Unlocking Value in Real Estate: Mortgage Rate Decline and Strategic Capital Allocation

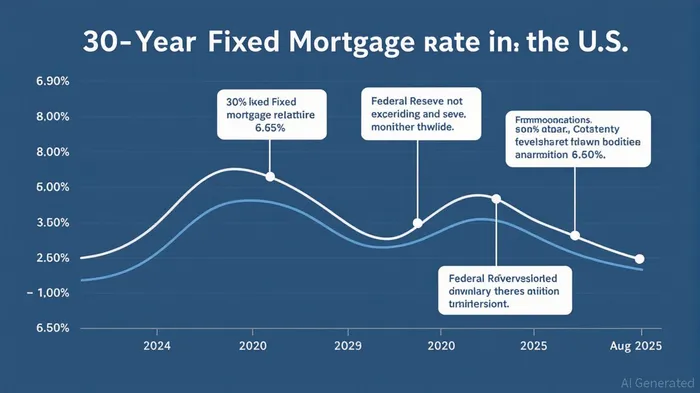

The U.S. housing market is at a pivotal inflection pointIPCX--. After a 10-month decline, the 30-year fixed mortgage rate has settled at 6.56% as of August 2025, marking a 40-basis-point drop from its January peak of 6.96%. This shift, driven by the Federal Reserve's cautious approach to inflation and a softening labor market, has sparked renewed interest in real estate equities. However, the path to recovery is far from linear, and investors must navigate a complex interplay of buyer behavior, inventory constraints, and sector valuations to capitalize on this opportunity.

The Mortgage Rate Decline: A Double-Edged Sword

The drop in mortgage rates has historically been a catalyst for housing demand, but the current environment is shaped by structural headwinds. The “lock-in effect” remains pronounced: existing homeowners, many of whom locked in rates below 4% during the 2021-2022 boom, are reluctant to sell, keeping active listings 15–20% below pre-pandemic levels in key markets like the Northeast and Midwest. This inventory bottleneck has limited the immediate impact of lower rates, as first-time buyers face a scarcity of affordable options.

Meanwhile, urban centers with strong employment growth—Austin, Seattle, and Phoenix—have shown resilience. These markets are attracting young professionals and tech workers, creating a niche for homebuilders focused on high-density, affordable housing. Conversely, Sun Belt states like Florida and Texas face affordability challenges, with home prices in the South and West declining by 5.9% year-to-date. The risk of a self-fulfilling cycle looms: falling rates could drive prices upward in constrained markets, negating affordability gains.

Sector Valuations: Growth vs. Value in Homebuilder861160-- Stocks

The valuation landscape for homebuilder stocks reveals a stark divergence between growth and value plays. D.R. Horton (DHI), the largest U.S. homebuilder, trades at a trailing P/E of 13.63 and a PEG ratio of 1.80, suggesting it is priced for growth but overvalued relative to earnings projections. In contrast, KB HomeKBH-- (KBH) offers a compelling value proposition, with a P/E of 6.97 and a P/B ratio of 8.05, reflecting a discount to its asset base. This dichotomy highlights the importance of sector rotation: investors should favor value-oriented homebuilders with strong balance sheets and geographic diversification while avoiding overhyped peers.

Real estate ETFs like the iShares U.S. Real Estate ETF (IYR) and the SPDR S&P Homebuilders ETF (XHB) have also diverged. IYR, which includes REITs and commercial real estate, has underperformed due to rising office vacancy rates and interest rate sensitivity. Conversely, XHB has gained 10.45% year-to-date, driven by resilient construction activity and a 5.2% rebound in housing starts in July 2025. This underscores the need to differentiate between real estate subsectors: defensive plays in residential construction and smart home technologies are outperforming, while commercial real estate remains vulnerable.

Strategic Capital Allocation: Navigating the New Normal

The current environment demands a nuanced approach to capital allocation. For homebuilders, the focus should shift toward urban infill projects and modular construction, which offer faster returns and lower inventory risks. Companies like KB Home and LennarLEN-- (LEN), with their expertise in cost-efficient development, are well-positioned to capitalize on this trend. Additionally, investors should consider defensive allocations in mortgage REITs (e.g., MORT, RLOC), which benefit from refinancing activity as rates approach the 6% psychological threshold.

However, risks persist. The Federal Reserve's projected 75-basis-point rate cuts in 2025 have already been partially priced into assets, limiting near-term upside. Moreover, potential Trump administration policies—such as streamlined zoning approvals and reduced immigration—could exacerbate labor shortages in construction, further constraining supply. Investors must also monitor wage growth, which remains stagnant, limiting broader economic momentum.

Is Now the Time to Overweight Real Estate Equities?

The answer hinges on timing and diversification. While the mortgage rate decline has created a favorable backdrop for homebuilders, the market remains vulnerable to a correction if inflation resurges or geopolitical tensions escalate. A strategic overweight in real estate equities is justified, but it should be balanced with defensive allocations in sectors like infrastructure and utility REITs.

For investors with a medium-term horizon, a 10–15% allocation to homebuilder ETFs (e.g., XHB) and value-oriented homebuilders (e.g., KBH) offers exposure to a sector poised for modest recovery. Those with a higher risk tolerance might consider leveraged REITs or construction tech firms, which stand to benefit from rate-driven demand. However, aggressive bets on commercial real estate or speculative land developers remain ill-advised.

Conclusion: Patience and Precision in a Shifting Landscape

The housing market's response to falling mortgage rates will be gradual, shaped by inventory constraints and economic moderation. For capital allocators, the key is to prioritize quality over speculation. Homebuilders with strong balance sheets, geographic diversification, and cost advantages will outperform in this environment. Meanwhile, real estate ETFs that emphasize residential construction and defensive sectors offer a safer path to capital preservation.

As the Fed edges closer to a 6% rate target, the housing market may see a surge in activity—but only if inventory constraints are resolved. Until then, investors should adopt a measured approach, leveraging the current discount in real estate equities while hedging against macroeconomic risks. The next chapter in the housing market's evolution is unfolding, and those who act with precision will be best positioned to capitalize on its opportunities.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet