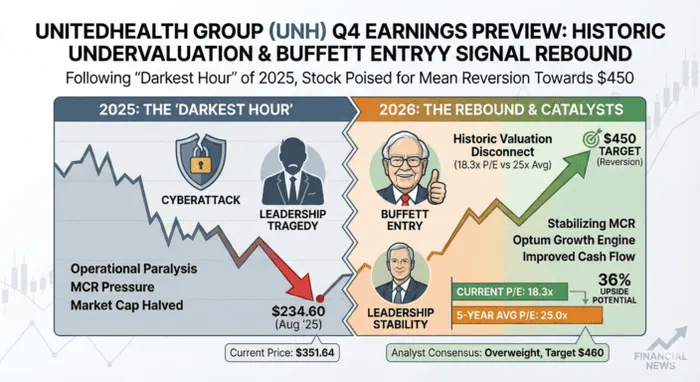

UnitedHealth Q4 Earnings Preview: Historic Undervaluation and Buffett Entry Signal Rebound Toward $450

UnitedHealth Group is scheduled to report its Q4 earnings for the fiscal quarter this week. The healthcare giant stands at a critical juncture. The stock is currently trading at $351.64 , attempting to claw back lost ground after a precipitous drop from its highs of over $600. The past year was arguably the most challenging in the company's history, marred by executive tragedy and cyber warfare. However, the convergence of stabilizing fundamentals, a historic valuation discount, and the re-emergence of legendary leadership suggests the "darkest hour" has passed. With Warren Buffett’s Berkshire Hathaway building a significant position and the stock showing technical resilience, the upcoming earnings report is likely to serve as the catalyst for a major value regression to the upside.

2025: Examining the "Darkest Hour"

To understand the potential of the upcoming report, investors must acknowledge the severity of the headwinds that cut UnitedHealth’s market cap in half over the last 12 months. The year 2025 was defined by a "perfect storm" of negative catalysts.

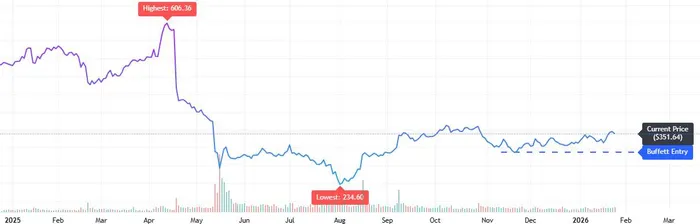

The timeline of distress began with the residual operational paralysis from the Change Healthcare cyberattack, which severely impacted claims processing and cash flow throughout early 2025. This vulnerability was compounded by the tragic assassination of UnitedHealthcare CEO Brian Thompson, an event that sent shockwaves through the corporate world and created a temporary leadership vacuum. As illustrated in the price action, these events drove UNHUNH-- stock from a peak of $606.36 down to a multi-year low of $234.60 in August 2025.

However, the worst of the reputational and operational damage appears to be priced in. The aggressive sell-off reflected panic rather than long-term structural failure. As the company moves past these non-recurring catastrophic events, the narrative is shifting from crisis management to recovery and operational efficiency.

Core Earnings Watch: Expectations and Turnaround

For this earnings release, Wall Street is looking less at headline revenue growth and more at margin stabilization and the "beat-and-raise" potential against significantly lowered bars.

- Headline Numbers: The consensus estimate for Q4 revenue currently stands at $113.6 billion, representing a 12.7% YoY increase. However, the real story is the bottom line. Analysts have priced in a "kitchen sink" quarter with an Adjusted EPS consensus of just $2.09—a steep drop from historical norms. This low bar creates a massive setup for a surprise; AIME indicate a potential beat in the $2.25–$2.35 range, driven by better-than-feared administrative cost controls.

- The Critical Metric (MCR): The most scrutinized number will be the Medical Care Ratio (MCR). After spiking to a concerning 89.9% in Q3 due to cyberattack fallout and elevated utilization, the street is bracing for a Q4 print near 90%. A print coming in anywhere below 89.0% would be viewed as a massive bullish signal, confirming that the cost structure has stabilized faster than the bear case suggests.

- Optum's Hidden Strength: While the insurance arm faced headwinds, Optum remains a growth engine. We project Optum revenue to top $70 billion for the quarter, with operating margins recovering toward 7%. If Optum confirms a backlog growth of 10%+, it validates the long-term structural moat.

- 2026 Guidance – The Real Catalyst: The turnaround thesis hinges on forward guidance. AIME expect management to reaffirm or slightly raise their 2026 Adjusted EPS outlook to the $17.60–$18.00 range. Confirming this double-digit growth trajectory would effectively declare the "crisis era" over and force a repricing of the stock's multiple.

The Turning Point: The "Buffett Floor" and Leadership Stability

Two major qualitative factors define the current bullish case for UnitedHealthUNH--.

First is the return of Stephen Hemsley. The reinstatement of Hemsley to a more active strategic role has calmed institutional jitters. Hemsley, the architect of UnitedHealth’s decade-long dominance, brings a level of credibility that is effectively stabilizing the shareholder base.

Second, and perhaps most critical for market sentiment, is the arrival of Warren Buffett. According to recent 13F filings analyzed by financial media, Berkshire Hathaway aggressively initiated a position in UNH during the dip below $300. Buffett’s entry is a textbook "value investing" signal—buying a high-quality compounder with a wide economic moat during a temporary period of distress. This institutional floor has changed the psychology of the stock; investors are no longer asking "how low can it go?" but rather "how much is it worth?"

Technical Analysis: A Deviation from the Mean

According to Ainvest analysis, the technical and fundamental charts present a compelling case for an immediate reversal.

The price action chart above illustrates a classic "V-shaped" recovery followed by consolidation. After hitting the capitulation low of $234.60, the stock rallied sharply, validating the "Buffett Entry" zone indicated around the $280-$300 level. Currently trading at $351.64, UNH has established a higher low structure. The stabilization above the $350 level suggests that supply exhaustion has occurred. The stock is now coiling, waiting for the earnings catalyst to break resistance and fill the gap toward the $400 mark.

Even more compelling is the valuation data shown in the second chart. According to Ainvest analysis, UnitedHealth is currently trading at a Price-to-Earnings (P/E) ratio of 18.35, which is significantly below its 5-year average of 25.08.

This is a statistical anomaly for a blue-chip defensive stock. Historically, UNH commands a premium due to its predictable cash flows. The current discount implies that the market is pricing UNH as a low-growth legacy insurer rather than a vertically integrated health tech giant. A simple reversion to the mean—returning to a P/E of 25x—would imply a stock price substantially higher than current levels. This valuation gap offers a significant margin of safety for new entrants.

Wall Street Sentiment: The Tide Turns

Leading into the print, sentiment on Wall Street has begun to thaw. Analysts from Morgan Stanley recently upgraded the stock to "Overweight," citing that the risk-reward ratio is now skewed 3:1 to the upside. They noted that the regulatory headwinds regarding Medicare Advantage rates are now fully understood and digested by the market.

Similarly, Goldman Sachs has issued a note highlighting that UnitedHealth’s free cash flow yield is approaching historic highs. Their revised price target sits at $460, implying that the stock could rally over 30% in 2026 as the "fear premium" dissipates. While some caution remains regarding potential government oversight, the consensus view is that the enterprise value has been compressed far below its intrinsic worth.

Conclusion

UnitedHealth Group enters this earnings season battered but unbowed. The "Black Swan" events of 2025 stripped the stock of its premium, but they did not destroy its business model. With the "darkest hour" of the CEO tragedy and cyberattacks in the rearview mirror, the company is poised for a significant mean reversion.

The combination of the "Buffett Put," Stephen Hemsley’s stewardship, and a P/E valuation that sits at a near-decade low creates a rare opportunity. For investors, the current price of $351 represents a mispricing of risk. As the earnings report confirms operational stability, the market is likely to rapidly reprice UNH back toward its historical averages. The value return is not just imminent; it has already begun.

Tianhao Xu is currently a financial content editor, focusing on fintech and market analysis. Previously, he worked as a full-time forex trader for several years, specializing in global currency trading and risk management. He holds a master’s degree in Financial Analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet