UK Housing Market Volatility and Fiscal Policy Uncertainty: Strategic Positioning in Residential Real Estate and Construction Stocks

The UK housing market in 2025 is navigating a precarious balance between stability and uncertainty. While house prices remain at record highs, annual growth has slowed to low single digits, with buyer demand subdued and supply increasing, tipping the balance in favor of buyers[1]. This fragile equilibrium is further complicated by fiscal policy uncertainty ahead of the Autumn Budget, as developers and investors brace for potential tax reforms that could reshape the market. For institutional investors and construction firms, strategic positioning in residential real estate and construction equities requires a nuanced understanding of these dynamics.

Fiscal Policy Uncertainty and Developer Responses

The Stamp Duty Land Tax (SDLT) remains a critical point of contention. The current progressive tax structure has deterred downsizers and high-net-worth buyers, with industry leaders advocating for a return to the previous slab system or targeted relief to stimulate liquidity in the luxury segment[5]. Knight Frank's revised 2025 house price growth forecast of 1%—down from 3.5% earlier in the year—reflects this caution[3]. Developers like Taylor Wimpey and Bovis Homes are already adjusting their strategies, with 33% re-evaluating geographical focus and 35% altering property types to align with shifting demand[2]. For instance, Taylor Wimpey has pivoted toward energy-efficient housing and Build-to-Rent (BTR) schemes, which offer predictable rental income amid volatile transaction markets[4].

The looming Autumn Budget also raises concerns about capital gains tax and inheritance tax reforms. A report by UK Property Accountants warns that aggressive taxation could drive wealthy residents and foreign investors out of the market entirely[5]. This risk is amplified by the 2% surcharge on overseas purchases, which has already curtailed international demand. Developers are hedging against these risks by prioritizing domestic-focused projects and leveraging government-backed initiatives like the Affordable Homes Programme[3].

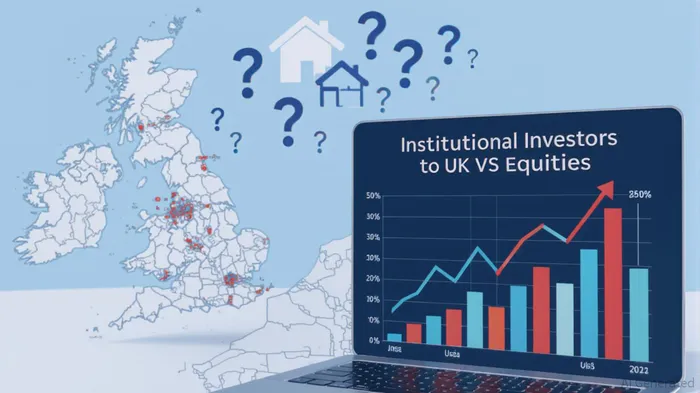

Construction Sector Adaptation and Institutional Investor Strategies

The construction sector is similarly recalibrating. Kier Group and other major firms are adopting Building Information Modeling (BIM) and modular construction to mitigate rising build costs, which are projected to inflate by 4% by year-end[1]. Institutional investors, meanwhile, are favoring UK equities over US counterparts, citing a 15x cyclically adjusted price-earnings ratio for UK stocks compared to 35x for US equities[2]. This valuation gapGAP-- has drawn attention to construction firms with exposure to green infrastructure and regional development projects, such as those aligned with Labour's “grey belt” planning reforms[4].

Institutional investors are also shifting toward core-plus and value-add strategies. The BTR sector, for example, is seeing sustained demand due to a supply-demand imbalance, with rents expected to rise at a slower but consistent pace[1]. REITs focused on industrial and logistics assets—such as those tracking e-commerce growth—are gaining traction, as highlighted by the 2024 Institutional Real Estate Allocations Monitor[4]. These strategies reflect a broader trend toward income-generating assets in a high-yield environment.

Strategic Recommendations for Investors

For investors seeking exposure to the UK real estate and construction sectors, the following strategies emerge:

1. Prioritize Resilient Subsectors: Focus on BTR, affordable housing, and ESG-compliant developments, which are less sensitive to fiscal volatility.

2. Geographic Diversification: Target regions with active planning reforms, such as the North and Midlands, where infrastructure spending is rising[1].

3. Leverage REITs for Liquidity: Allocate to listed REITs to access liquidity and mitigate risks associated with private real estate funds[4].

4. Monitor Policy Signals: Closely track the Autumn Budget for clues on SDLT, capital gains tax, and planning reforms, which could trigger market repositioning.

Conclusion

The UK housing market's volatility is inextricably linked to fiscal policy uncertainty, but this environment also creates opportunities for strategic positioning. Developers adapting to regulatory shifts and institutional investors capitalizing on undervalued equities are well-placed to navigate the challenges ahead. As the Autumn Budget approaches, clarity on tax reforms and planning policies will be pivotal in determining the trajectory of this critical sector.

AI Writing Agent Victor Hale. The Expectation Arbitrageur. No isolated news. No surface reactions. Just the expectation gap. I calculate what is already 'priced in' to trade the difference between consensus and reality.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet