TSMC Earnings Beat Estimates Again as AI Supercycle Continues, Guiding to an Even More Explosive Year Ahead

- Q4 results beat across the board, with revenue and profit exceeding expectations and gross margin surging to an exceptional 62.3%, underscoring TSMC's growing pricing power in advanced nodes.

- Advanced-node demand remains red-hot, as 3nm, 5nm, and 7nm processes accounted for a record 77% of revenue, driven by sustained AI chip demand led by NvidiaNVDA-- and resilient consumer electronics.

- Forward guidance shocked the market, with management projecting nearly 30% revenue growth this year, record-high margins, and aggressive capex plans, reinforcing the view that the AI supercycle is far from over.

AI still shows no signs of slowing. TSMC's latest fourth-quarter earnings once again beat expectations, while management guided that 2026 will be an even bigger harvest year. This earnings report effectively silences the skeptics who have been calling for the end of the AI boom.

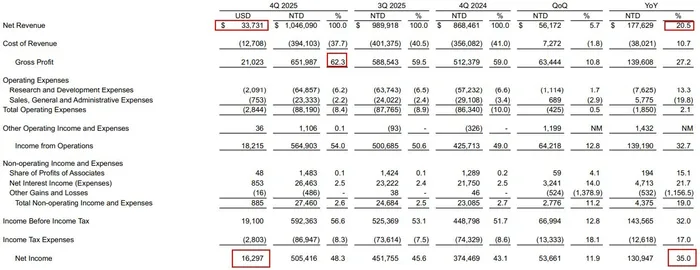

Looking at the numbers , TSMCTSM-- reported revenue of $33.7 billion, up 25% year over year and 2% quarter over quarter, exceeding the top end of its prior guidance of $33.4 billion. Net income came in at $16.3 billion, up 41% year over year.

The most striking figure was gross margin, which surged to 62.3%, up another 3.3 percentage points from the previous quarter. With a near-monopoly over advanced chip manufacturing for AI and high-end consumer electronics, TSMC now enjoys pricing power comparable to that of chip designers themselves.

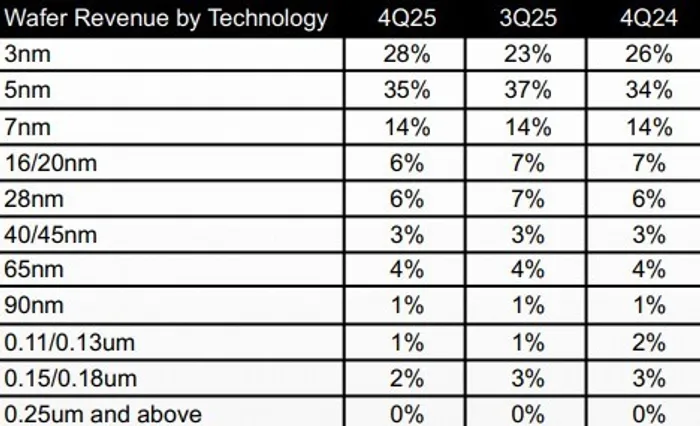

3nm + 5nm + 7nm revenue nears 80%: Nvidia driving the surge?

The earnings report shows that 3nm chips accounted for 28% of total revenue this quarter, up 5 percentage points sequentially and 2 points year over year. Part of this can certainly be attributed to strong holiday-season sales of the iPhone 17 series. However, a five-point sequential jump suggests Nvidia may also be playing a role. Nvidia's next-generation AI architecture after Blackwell, Rubin, entered production in the fourth quarter, and Jensen Huang previously requested TSMC expand 3nm capacity by 50%. Amid the AI frenzy, demand for advanced process nodes continues to surge, driving both volume and pricing higher.

Meanwhile, 5nm contributed 37% of revenue, down 2 percentage points quarter over quarter, indicating that more demand is shifting toward the cutting-edge 3nm process. Revenue contribution from 7nm was flat sequentially at 14%.

Overall, 3nm, 5nm, and 7nm combined accounted for 77% of total revenue, a new record high. With consumer electronics and AI acting as twin growth engines, TSMC's moat remains rock-solid.

By platform, revenue from high-performance computing (HPC) declined slightly to 55%, down 2 percentage points sequentially. Smartphone-related chips rose 2 points to 32%, reflecting stronger demand during the holiday shopping season. That said, AI-related products continue to show resilience regardless of the cycle.

Revenue contribution from IoT chips (wearables, smart home devices) and automotive chips remained steady at 5%.

AI demand still exploding; revenue expected to grow nearly 30% this year

Despite recurring doubts about an impending end to the AI cycle, TSMC's guidance suggests this is not even on the radar. The company expects first-quarter revenue of $34.6–35.8 billion, another record high, implying about 38% year-over-year growth at the midpoint. For the full year, revenue is projected to grow close to 30% in U.S. dollar terms. First-quarter gross margin is expected to reach 63%–65%. For context, Nvidia—a chip designer—posts gross margins around 75%, underscoring TSMC's extraordinary pricing power in advanced manufacturing.

TSMC is also aggressively ramping capital expenditures to expand capacity and narrow the supply-demand gap. It expects capex of $52–56 billion this year, up 31% year over year, a notably aggressive plan, and noted that capital spending will rise significantly over the next three years. On the technology front, mass production of 2nm chips began in the fourth quarter. In terms of fabs, construction of the Germany plant is progressing; Japan's second fab has broken ground; and construction of the Arizona P2 fab in the U.S. has been completed, with production tools expected to be installed in 2026. The AI boom is far from over.

Overall, TSMC's latest earnings modestly beat expectations, and its gross margin was staggering. But it is the guidance for this year and beyond that truly shocked the market. Even after two years of explosive growth, the company can still deliver high-speed expansion, reinforcing the view that the AI wave will persist well into the foreseeable future and solidifying its long-term investment narrative. This also signals that global tech giants will continue to ramp up AI spending, setting the stage for more strong earnings across the technology sector.

Crypto market researcher and content strategist with 3 years of experience in digital asset analysis and market commentary. Skilled at transforming complex blockchain data and trading signals into clear, actionable insights for investors. Experienced in covering Bitcoin, Ethereum, and emerging ecosystems including DeFi, Layer2, and AI-related projects. Passionate about bridging professional market research with accessible storytelling to empower readers and investors in the fast-evolving crypto landscape.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet