Trump's Tit-for-Tat Tariffs Could Inflict Further Pain on Stocks: The Incoming Storm and Our Strategy

The S&P 500 has nearly erased its gains since November 5th, when Donald Trump secured a sweeping victory in the U.S. presidential election. Endless tariff threats and a focus on MAGA over economic fundamentals have raised investor concerns. Although current valuations appear reasonable amid ongoing AI advancements, the escalation of the tit-for-tat trade war, a slowing economy, and Trump's tendency to blame the previous administration could further depress market beta. Friday's nonfarm payrolls may serve as the next catalyst for market disruption, prompting investors to prepare for additional downside risks.

Global Trade War Intensifies

Many had anticipated that a Trump 2.0 administration would boost stocks through deregulation and margin expansion. However, the President has increasingly acted as a capricious politician rather than a seasoned businessman. Tariffs have become his primary tool to force concessions from trading partners, compelling companies to invest billions in the U.S. without clear benefits. As Psychology 101 reminds us, while punishment may curb unwanted behavior in the short term, it can hinder long-term growth and produce negative side effects.

The tit-for-tat has already begun. The Trump administration doubled tariffs on Chinese goods to 20% and imposed 25% tariffs on imports from Mexico and Canada starting Tuesday. In response, China immediately announced additional tariffs of 10–15% on U.S. agricultural goods, while Canada is considering a 25% tariff on over $100 billion of U.S. goods next month, and Mexico is evaluating countermeasures. Although Canada and Mexico have previously compromised under U.S. pressure, this time they appear poised to adopt a stronger retaliatory stance as real tariffs take effect.

This is only phase one. Trump's 25% tariff on steel and aluminum imports is set to take effect on March 12, with further tariffs on the EU and additional measures on China anticipated, and reciprocal actions scheduled for April 2. With more countries likely to join the tit-for-tat, the market could face significant volatility in the near future. Trump has signaled that he will escalate tariffs in response to further retaliation, potentially creating a highly unstable trade environment.

The current scenario is markedly different from 2016–2020, when Trump's tariff actions primarily targeted China. In 2024, the U.S. posted a trade deficit of $1.2 trillion, with Mexico, Canada, and China ranking as its top three trading partners. The resulting retaliatory measures could have far more severe consequences than previously imagined.

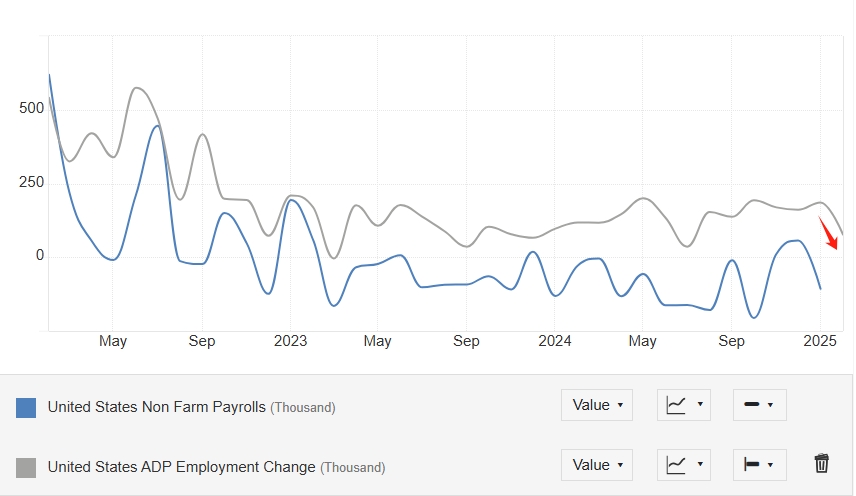

Economic Slowdown and Blame Biden

Global trade tensions may ignite inflationary pressures, further weaken the economy, and force the Fed to implement rate cuts to stave off recession risks. U.S. consumer confidence is plummeting its steepest decline in four years, while January's core PCE of 2.6% remains above the Fed's 2% target. With tariffs on Chinese goods already in effect in February and more scheduled for March, market participants are closely watching upcoming inflation data, while Friday's nonfarm payroll report becomes even more critical.

Disappointing job creation figures have added to concerns. According to ADP, private sector employment increased by only 77,000 in February, well below the 148,000 consensus, marking the smallest increase since July. Some economists now project that Friday's report could show a gain of merely 170,000 jobs, with the unemployment rate holding at 4%, signaling substantial downside risks.

Recalling the nonfarm payroll report from last July (+114K), which came in well below the estimate (+185K), the S&P 500 tumbled 1.84% that Friday and fell another 3% on Monday. If this month's nonfarm payroll report presents a similar scenario, stocks could face even more trouble amid tariff headwinds and the Fed's cautious stance.

Recalling the nonfarm payroll report from last July (+114K), which came in well below the estimate (+185K), the S&P 500 tumbled 1.84% that Friday and fell another 3% on Monday. If this month's nonfarm payroll report presents a similar scenario, stocks could face even more trouble amid tariff headwinds and the Fed's cautious stance.

Importantly, Trump is likely to deflect blame for any economic downturn onto Biden. In previous addresses, he claimed the economy inherited an economic catastrophe and an inflation nightmare from the previous administration, a rhetoric echoed by Commerce Secretary Howard Lutnick, who faulted Biden for recent economic declines and stock market drops.

Even if some stocks have attractive fundamentals and reasonable valuations, the deteriorating macroeconomic backdrop could further depress valuations. Recent volatility driven by Trump's unpredictable policy moves suggests that market trends can reverse abruptly.

Investors are advised to hedge against further downside risks—potentially by purchasing SPXSPXC-- put options, maintaining cash reserves, or investing in defensive stocks. The current rotation into safe-haven stocks such as WalmartWMT--, Costco, and CokeCOKE-- indicates a shift in investor sentiment, but caution is warranted as further adverse policies may materialize.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO