Trump Tariffs and the Upcoming CPI Report: What Market Expectations Hold

As the economic impact of Donald Trump’s aggressive tariff policies begins to surface in U.S. summer data, July’s Consumer Price Index (CPI) was already poised to draw intense scrutiny. Now, with the report set to release—just 11 days after Trump ousted the Bureau of Labor Statistics commissioner—the stakes have risen further, injecting unprecedented intrigue into the closely watched inflation gauge.

A Controversial Prelude to the Data

The upcoming CPI release follows a turbulent two weeks for the BLS. On August 1, a surprisingly weak nonfarm payroll report—accompanied by significant downward revisions to prior months’ data—prompted Trump to accuse then-BLS Commissioner Erika McEntarfe of “tampering” with figures, leading to Beach’s immediate dismissal. The allegation was swiftly rebuked by former BLS commissioners from Trump’s own administration, as well as prominent economists and statisticians.

Trump announced via social media on Monday his intent to nominate E.J. Antoni, chief economist at The Heritage Foundation, as Beach’s successor. Notably, Antoni has a long history of criticizing the BLS, adding another layer of scrutiny to how the agency’s data will be interpreted moving forward.

Against this backdrop, a central question looms: Will the July CPI figures align with the Trump administration’s expectations?

Data Integrity Concerns Echo Beyond Employment

The same issues plaguing recent job reports—namely, sampling inadequacies—also plague CPI calculations, raising risks of larger future revisions to this investor-critical inflation metric. As part of sweeping budget cuts by the Office of Management and Budget, the BLS has scaled back data collection for key price indices.

Since April, the agency has halted in-person inflation data gathering in three major metropolitan areas: Buffalo, New York; Lincoln, Nebraska; and Provo, Utah. Instead, it has increasingly relied on “imputation”—estimating prices through regional or national comparisons rather than direct local observation.

“The margin of error will widen, and we should expect rolling revisions to CPI data, similar to what we’ve seen with employment and durable goods figures,” noted Joe Brusuelas, chief economist at RSM US.

CPI’s Stakes: More Than Headlines, a Fed Deciding Factor

Beyond the BLS drama, the July CPI carries critical implications for Federal Reserve policy, particularly whether the central bank can proceed with a September rate cut.

Jim Reid of Deutsche BankDB-- called the report “one of the summer’s defining market events,” emphasizing its role in gauging whether tariffs are finally passing through to consumer prices.

Economists have long warned of tariff-driven inflation, but tangible impacts have been elusive—until recently. Two weeks ago, the Fed’s preferred inflation gauge, the June Personal Consumption Expenditures (PCE) index, surged, hinting that “tariff inflation” may be materializing. July’s CPI could offer further confirmation.

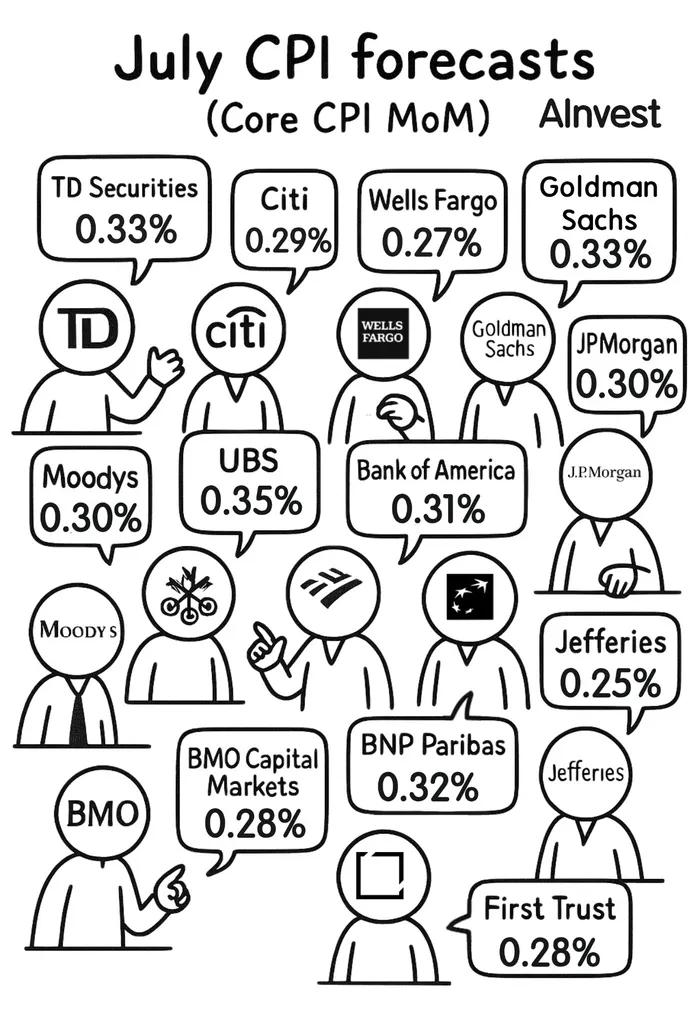

Median forecasts point to:

- A 2.8% year-over-year rise in headline CPI, up from 2.7% in June.

- A 0.2% monthly increase, slowing from June’s 0.3%.

- Core CPI (excluding food and energy) likely climbing to 3.0% year-over-year—its highest since February—from 2.9%, with a 0.3% monthly gain (up from 0.2%).

Most Wall Street banks peg core inflation between 2.9% and 3.1%, with more predicting 3.1% than 2.9%, signaling skew toward upward surprises.

Early signs of tariff pressures emerged in June: apparel prices rose 0.4%, footwear reversed months of declines with a 0.7% jump, and furniture/bedding prices climbed 0.4% after a 0.8% drop in May—suggesting cost pressures are reaching consumers.

What to Watch for in Market Reactions

For investors betting on a September Fed cut, inflation data now stands as the last major hurdle.

“The market is looking for confirmation that trade policy shifts are feeding into higher goods inflation,” said Gennadiy Goldberg, head of U.S. rates strategy at TD Securities. “All else equal, hotter inflation could make the Fed want to see more data before cutting.”

George Catrambone, head of Americas fixed income at DWS, noted that persistent inflation would amplify Fed Chair Jerome Powell’s concerns about conflicting dual mandates (stable prices vs. full employment). Policymakers will also weigh August’s CPI and Thursday’s Producer Price Index before the September decision.

Stuart Kaiser, an analyst at CitigroupC--, warned, “CPI could present the Fed with a dual-mandate dilemma,” highlighting core goods prices as a key focus. “Last month’s uptick in goods inflation may persist as tariffs take effect. With two FOMC members dissenting in favor of cuts in July, uncertainty lingers—especially if inflation rises—though the trend in policy rates remains downward.”

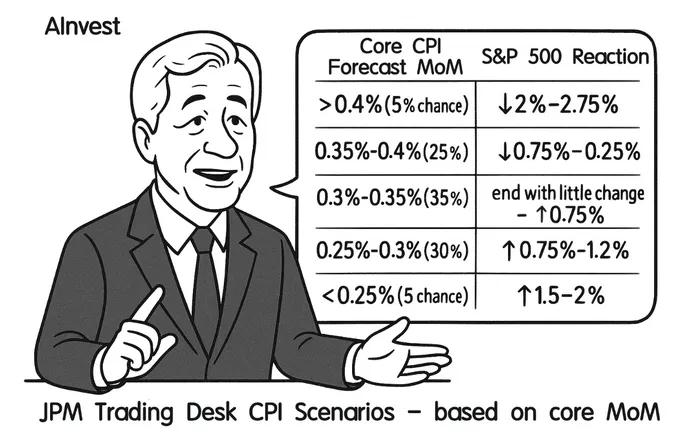

JPMorgan, in its pre-data analysis, outlined potential market scenarios:

Vickie Chang of Goldman SachsGS-- Global Macro Research noted that recent labor market weakness has already priced in “a dovish policy surprise,” buoying bonds and equities. A soft CPI could even spark bets on a 50-basis-point September cut, she said, while a hot reading (e.g., 0.4%+ core monthly gain) might delay easing expectations and weigh on risk assets—though any selloff could be short-lived, given upcoming Jackson Hole and jobs data.

As markets brace for the release, the July CPI report has transcended its usual role as an inflation gauge, becoming a focal point for debates over data integrity, policy influence, and the economic toll of tariffs. Its impact will resonate far beyond tonight’s trading floors.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet