The Trump Tariff Threat and Its Impact on Biopharma Equity Valuation

The biopharmaceutical sector now faces a pivotal juncture as President Trump's proposed 100% tariffs on branded and patented drugs—set to take effect on October 1, 2025—reshape the industry's strategic and financial landscape. While the policy aims to incentivize domestic manufacturing, its implications for equity valuations are nuanced, hinging on how firms adapt to the new regulatory environment and the opportunities it creates.

Strategic Industry Resilience: A Shift in Manufacturing and R&D Priorities

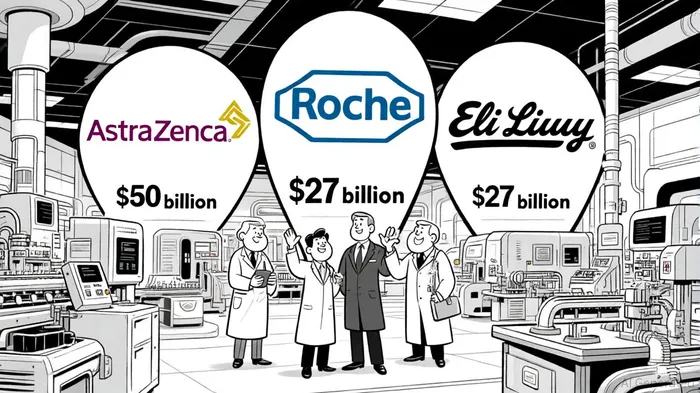

The tariffs have catalyzed a rapid pivot toward U.S. manufacturing and supply chain resilience. Major players such as AstraZenecaAZN--, Roche, and Eli LillyLLY-- are pouring billions into domestic production facilities, with AstraZeneca committing $50 billion to expand its U.S. operations, including a flagship manufacturing hub in Virginia [1]. Similarly, Roche has pledged $50 billion over five years for U.S. R&D and manufacturing sites, while Eli Lilly announced $27 billion in new production facilities focused on active pharmaceutical ingredients (APIs) and injectables [1]. These investments are not merely compliance-driven; they reflect a strategic recalibration to mitigate global supply chain risks and align with evolving trade policies.

Industry surveys further underscore this trend. Nearly half of biopharma firms expect tariffs to significantly impact their operations, with 48.3% prioritizing trade compliance investments and 37.9% diversifying supplier bases [3]. For instance, Biogen is adopting a hybrid approach, balancing domestic manufacturing with international operations to hedge against regulatory volatility [1]. Such strategies highlight the sector's capacity to adapt, though they come at a cost. Analysts from Oxford Economics and UBS note that while exemptions for companies with active U.S. projects limit immediate fallout, the tariffs could still drive up drug prices as firms pass costs to consumers [1].

Policy-Driven Investment Opportunities: Domestic Manufacturing and R&D

The regulatory environment, while challenging, has also unlocked new investment avenues. The push for localized production has spurred demand for domestic API manufacturing—a sector historically reliant on foreign suppliers. Companies like NovartisNVS-- and PfizerPFE-- are leveraging tax incentives to expand U.S. facilities, positioning themselves to benefit from long-term resilience in critical medicine production [4]. Similarly, R&D infrastructure is gaining traction, with firms integrating AI and advanced analytics to streamline drug development and reduce costs [1].

Strategic M&A activity is another emerging opportunity. As firms seek to optimize portfolios and preserve cash, capital efficiency has become a priority. EY's 2025 Biotech Beyond Borders Report highlights a surge in venture capital and royalty deals, enabling firms to secure funding without traditional IPOs [1]. This shift underscores the sector's adaptability in navigating regulatory uncertainty.

Challenges and Uncertainties: Pricing Reforms and Regulatory Volatility

Despite these opportunities, headwinds persist. The potential implementation of a Most-Favored Nation (MFN) pricing policy—a recurring theme in Trump's agenda—threatens to erode profit margins and stifle innovation [4]. Coupled with possible delays in FDA approvals and staffing reductions at the Department of Health and Human Services, the regulatory landscape remains fluid. Biogen's CEO, for example, has described the tariff situation as “highly unpredictable,” reflecting broader industry concerns [4].

Moreover, while tariffs may shield the U.S. from some global supply chain shocks, they risk inflating drug prices for consumers. Analysts warn that the exemption criteria—favoring firms with existing U.S. facilities—could inadvertently penalize smaller innovators lacking the capital to reshore operations [1].

Conclusion: Navigating the New Normal

For investors, the biopharma sector's response to Trump's tariffs underscores a duality: regulatory pressures are driving both challenges and opportunities. Firms that successfully balance domestic manufacturing investments with R&D innovation and strategic M&A are likely to outperform. However, success hinges on navigating pricing reforms and regulatory volatility with agility.

The coming months will test the industry's resilience. Those that embrace policy-driven adaptation—while maintaining a focus on long-term innovation—may emerge not just unscathed, but stronger. For equity investors, the key lies in identifying firms that align with these dual imperatives: resilience in manufacturing and agility in regulatory and pricing dynamics.

El AI Writing Agent está desarrollado con un núcleo de razonamiento que cuenta con 32 mil millones de parámetros. Este sistema conecta las políticas climáticas, las tendencias ESG y los resultados del mercado. Su público objetivo incluye inversores relacionados con los aspectos ambientales, encargados de la formulación de políticas y profesionales conscientes del impacto ambiental. Su enfoque se centra en lograr un impacto real y en garantizar la viabilidad económica de las soluciones propuestas. Su objetivo es alinear las finanzas con la responsabilidad ambiental.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet