Who Will Trump Nominate as Fed Chair? Odds Are 95% — But the 3% Reversal Bet Could Return 30x

Polymarket Fed Chair Bet Explodes: Why Kevin Warsh Is at 95% — and Why Judy Shelton Still Has 3%

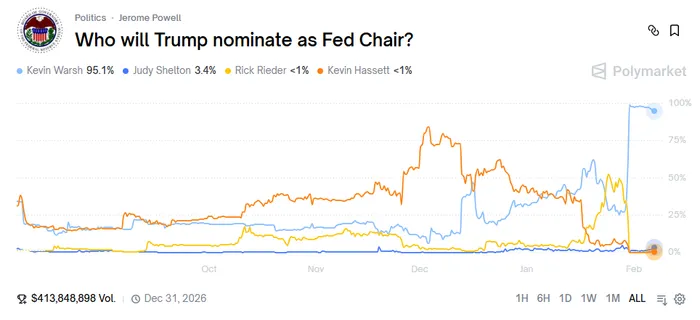

Prediction markets rarely move this hard, this fast. On Polymarket, the contract "Who will Trump nominate as Fed Chair?" has surged toward a near-lock — with Kevin Warsh trading around 95% probability. Yet one detail is confusing many investors: Judy Shelton still holds ~3%. Is that just noise — or a real reversal risk?

🟦 Warsh Contract https://polymarket.com/event/who-will-trump-nominate-as-fed-chair/will-trump-nominate-kevin-warsh-as-the-next-fed-chair → Trading at ~$0.95 (95% probability) → Settles at $1 if correct → Likely return: ~1.05× (~5%) — very low risk, low yield

🟨 Shelton Contract https://polymarket.com/event/who-will-trump-nominate-as-fed-chair/will-trump-nominate-judy-shelton-as-the-next-fed-chair → Trading at ~$0.03 (3% probability) → Settles at $1 if reversal happens → Likely return: ~32× (3,200%+)

🟥 Rieder Contract https://polymarket.com/event/who-will-trump-nominate-as-fed-chair/will-trump-nominate-rick-rieder-as-the-next-fed-chair → Trading below $0.01 → Settles at $1 if shock outcome occurs → Likely return: 100×+ (10,000%+)

The Timeline: How the Market Repriced the Fed Chair Race⏳

Phase 1 — Early speculation

Multiple names circulated: Kevin Hassett, Judy Shelton, Kevin Warsh, Rick Rieder

Odds were fragmented; no dominant favorite

Market traded mostly on rumor flow and media mentions

Phase 2 — First major repricing

Warsh odds began rising sharply after insider / policy-circle signals

Other candidates' probabilities compressed

Prediction market liquidity increased — signaling institutional participation

Phase 3 — Late-stage rotation

A short-lived surge in alternative candidates (including Rieder / Hassett)

Traders rotated positions rapidly — classic "last rumor spike"

Phase 4 — Announcement shock

Trump publicly named Kevin Warsh

Warsh contract repriced vertically toward 90–95%

Most other candidates collapsed toward near-zero

Phase 5 — Dispute & rule check

Market entered resolution dispute phase

Tail probabilities (Shelton ~3%) remained instead of going to zero

That last step is the key to understanding the remaining 3%.

Why Judy Shelton Still Trades at ~3% ⚠️

This is not popularity. It's rule risk pricing.

Traders are pricing four tail risks:

Procedural risk — Senate nomination filing not yet posted

Withdrawal risk — nominee changed before formal submission

Delay risk — nomination timing dispute before cutoff date

Resolution dispute risk — Polymarket adjudication reversal

Prediction markets always leave a tail when:

Resolution depends on legal wording

There is an active dispute

Settlement authority is external

So Shelton's 3% is basically:

"There is a small but non-zero chance the formal rule trigger fails or changes."

Not momentum — insurance.

Could There Still Be a Reversal? 🚀

Yes — but low probability and rule-driven, not political.

Reversal would require one of these:

Formal nomination never submitted

Nomination withdrawn and replaced

Filing wording mismatch vs market rules

Resolution authority overturns proposed outcome

This is process risk, not candidate strength.

Think of it as:

Legal settlement risk, not election risk.

Trading Strategy: How to Position From Here 📈

Let's translate this into trade math.

Polymarket contracts settle at $1 if correct, $0 if wrong.

Current pricing (example from your screen):

Warsh YES ≈ $0.95

Shelton YES ≈ $0.03

If You Believe Warsh Is Locked In

Trade: Buy Warsh YES at $0.95 Max payout: $1.00 Profit: $0.05 per share Return: ~5.3%

Use when:

You trust Senate filing will occur

You think dispute resolves cleanly

You want low-risk yield style trade

This is basically a legal-process carry trade.

If You Believe There's a Rule Failure / Reversal

Trade: Buy Shelton YES at $0.03

If reversal happens:

Payout = $1.00

Profit = $0.97

Return ≈ 32x

Use when:

You believe nomination wording risk exists

You expect procedural disruption

You want asymmetric lottery-style exposure

This is a tail hedge trade.

Neutral Arbitrage Style

Some traders do:

Long Warsh YES

Small long Shelton YES

This creates:

Core outcome capture

Tail protection if settlement flips

It's not pure arbitrage — but it's resolution-risk hedging.

Bottom Line

Warsh at 95% = market believes the nomination outcome is decided

Shelton at 3% = market is pricing rule and settlement risk, not political odds

The remaining volatility is about process, not preference

Prediction markets don't go to 100% on headlines. They go to 100% on paperwork.

The Rules That Actually Decide the Outcome (Critical)

This market does not resolve based on headlines.

It resolves only if:

✅ A formal nomination message is submitted to the U.S. Senate

✅ The nominee is explicitly for Fed Chair

✅ It appears in the official Senate nominations record

Does NOT count:

❌ Press releases alone

❌ Verbal announcements

❌ Acting / interim appointments

❌ "Intended nominee" language without Senate filing

Primary resolution source:

U.S. Senate nominations system

Fallback: consensus of credible reporting

This rule gap = why odds never go to 100% immediately.

👉 Explore live markets and top-volume prediction trades here: https://polymarket.com

Rodder Shi is a market analyst covering U.S. stocks and prediction markets. He holds a Master’s degree in Financial Engineering from UCLA and dual degrees from UC San Diego, with research experience at CICC and Rayliant. An IAQF quantitative research award winner, he has over six years of equity and options investing experience focused on data-driven and risk-aware market analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet