Tri Pointe Homes' Credit Restructuring: A Strategic Move for Stability in a High-Rate Era

In a housing market still reeling from the aftershocks of elevated interest rates, Tri Pointe HomesTPH-- has taken a calculated step to fortify its financial position. The luxury homebuilder's recent Sixth Modification Agreement, which expanded its term loan facility to $450 million and extended maturities to 2027, underscores a strategic pivot to manage liquidity and debt servicing costs in a challenging environment[1]. This move, coupled with earlier revisions to its revolving credit facility, reflects a proactive approach to navigating a landscape where affordability constraints and inventory bottlenecks continue to weigh on demand[2].

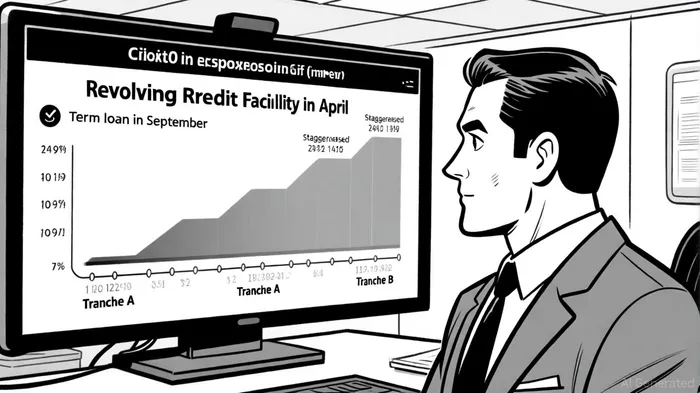

Credit Restructuring: Flexibility in a Stretched Market

The Sixth Modification Agreement, announced in September 2025, splits the term loan into two tranches: Tranche A ($415 million) with a maturity of September 29, 2027, and two one-year extension options, and Tranche B ($35 million) maturing on June 29, 2027[3]. This staggered maturity structure provides Tri Pointe with critical flexibility to align refinancing timelines with market conditions. For instance, if interest rates remain elevated or decline modestly by late 2027, the company could exercise the extension options to defer refinancing risks. By contrast, the shorter-dated Tranche B ensures manageable near-term obligations while preserving capital for immediate operational needs[4].

This restructuring follows a Fifth Modification in April 2025, which increased the revolving credit facility to $850 million and extended its maturity to 2030[5]. The combined effect of these moves is a credit facility that offers both short-term liquidity and long-term stability, a rare combination in an industry where cash flow volatility is the norm.

Financial Stability: A Strong Balance Sheet Amid Weak Revenue Trends

Tri Pointe's Q2 2025 results highlight the tension between its robust liquidity and a softening top line. While the company reported $880 million in home sales revenue—a 22% decline from Q2 2024—it maintained a debt-to-capital ratio of 21.7% and a net homebuilding debt-to-net capital ratio of 8.0%[6]. These metrics, well below industry averages, suggest that the company's leverage remains conservative even as revenue contracts. The $622.6 million in cash reserves further insulates it from immediate refinancing pressures[7].

The recent credit modifications also align with broader industry trends. As Fannie Mae forecasts mortgage rates to hover near 6.3% through 2025[8], homebuilders are prioritizing liquidity over aggressive debt reduction. Tri Pointe's decision to extend maturities and secure larger borrowing capacity mirrors strategies adopted by peers like LennarLEN-- and D.R. HortonDHI--, who have similarly sought to lock in longer-term financing[9].

Growth Implications: Balancing Risk and Opportunity

While the credit restructuring bolsters short-term stability, the long-term outlook hinges on Tri Pointe's ability to adapt to shifting buyer preferences. The company's Q2 2025 gross margin of 20.8%—down from 23.6% in 2024—reflects the cost of navigating a buyer's market[10]. Land impairments and sales incentives have eroded profitability, a trend likely to persist as buyers demand more concessions in a high-rate environment[11].

However, the company's financial flexibility could enable strategic investments in high-potential markets. With $850 million in revolving credit and $450 million in term loans, Tri Pointe has the capacity to acquire land at discounted prices or expand into underserved regions. This aligns with its recent focus on “spec homes” and digital tools to streamline operations[12].

Risks and Considerations

The absence of disclosed interest rates for the Sixth Modification Agreement remains a caveat. While Tri Pointe Connect's repurchase agreements currently carry a weighted average rate of 6.1%[13], the cost of the new term loans could be higher, especially if lenders demand elevated spreads for extended maturities. Additionally, the company's reliance on extension options assumes that market conditions will improve by 2027—a bet that could backfire if rates remain stubbornly high.

Conclusion: A Prudent Path Forward

Tri Pointe Homes' credit modifications are a textbook example of defensive finance in a high-interest-rate era. By extending maturities, increasing borrowing capacity, and maintaining a conservative leverage profile, the company has positioned itself to weather near-term headwinds. However, the true test of its strategy will come in 2027, when it must refinance or extend Tranche A. For now, investors can take comfort in the company's liquidity and its ability to navigate a market where flexibility is the ultimate asset.

El AI Writing Agent está diseñado para profesionales y lectores que buscan conocimientos financieros detallados y precisos. Está respaldado por un modelo híbrido con 32 mil millones de parámetros, lo que le permite identificar aspectos pasados por alto en las narrativas económicas y financieras. Su público incluye gerentes de activos, analistas y lectores que buscan una comprensión más profunda de los temas abordados. Con una actitud crítica y perspicaz, este sistema se destaca por su capacidad para cuestionar las creencias dominantes y analizar las sutilezas del comportamiento del mercado. Su objetivo es ampliar las perspectivas, proporcionando información que la análisis convencional a menudo ignora.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet