U.S. Treasury Yields Drop Ahead of Jobs Report: What Traders Are Watching

The U.S. Treasury market has entered a period of recalibration, with the 10-year yield drifting lower as investors price in a dovish Federal Reserve and a labor market showing early signs of strain. By the end of August 2025, the benchmark yield had settled at 4.25%, down from 4.4% in June, reflecting a shift in expectations that has reshaped fixed-income strategies across the globe. This decline is not merely a technical adjustment but a signal of deeper macroeconomic forces at play: a cooling labor market, a central bank poised to cut rates, and a global bond market grappling with fiscal fragility.

Labor Market Signals: A Tipping Point?

The ADP private-sector jobs report for August added just 54,000 positions, far below the 68,000 forecast, while initial jobless claims rose to 237,000—the highest level since early 2024. These numbers, coupled with a job openings-to-unemployment ratio approaching parity, have stoked fears of a labor market teetering toward oversupply.

Investors are now pricing in a near-certain 25-basis-point rate cut at the September Fed meeting, with two additional cuts expected by year-end. The Fed's pivot, signaled at Jackson Hole, has shifted the narrative from inflation obsession to labor market stabilization. “The Fed is no longer fighting the last war,” one strategist noted. “They're now focused on preventing the next one.”

Central Bank Policy: Dovish Pivots and Fiscal Uncertainty

The Federal Reserve's pivot has been mirrored by a global reevaluation of monetary policy. In Europe, German and French 30-year yields have surged to multi-decade highs, driven by political instability and fiscal concerns. Meanwhile, the U.S. faces its own fiscal headwinds: a federal appeals court's ruling against President Trump's tariffs threatens to erase $172.1 billion in projected revenue, potentially forcing increased Treasury issuance.

This confluence of domestic and international pressures has created a paradox: while the Fed's rate cuts are expected to drive Treasury yields lower, the risk of fiscal-driven supply shocks could push them higher. Traders are hedging this duality by shortening duration and favoring the “belly” of the yield curve (3- to 7-year maturities), where yield differentials and rolldown benefits offer a more attractive risk-reward profile.

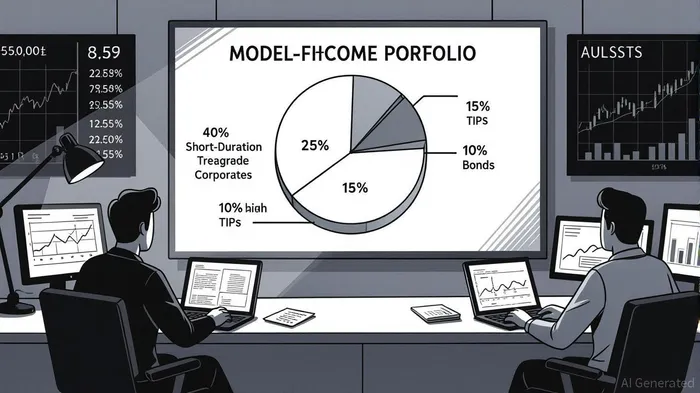

Tactical Fixed-Income Allocations: Navigating the New Normal

The shift in bond market strategy is evident in the flow of capital. Over $69 billion has poured into short-term Treasury ETFs since November 2024, while long-term ETFs have seen outflows exceeding $5 billion. Investors are also rotating into inflation-linked Treasuries (TIPS) and high-quality corporate bonds, particularly BBB-rated paper, which balances yield with credit safety.

The traditional 60/40 portfolio's diversification benefits have weakened in a dovish regime, prompting a surge in allocations to commodities and digital assets. However, fixed-income remains a cornerstone for capital preservation, with active yield curve positioning—particularly in the belly—offering a hedge against both rate cuts and inflation surprises.

Investment Advice: Balancing Income and Risk

For investors, the current environment demands a nuanced approach:

1. Shorten Duration: Prioritize 3- to 7-year Treasuries and corporate bonds to mitigate inflation risks while capturing rolldown gains.

2. Embrace TIPS: With inflation still above 2.9%, inflation-linked bonds provide a critical hedge against price pressures.

3. Diversify Geographically: Currency-hedged local-currency bonds from Germany, France, and Italy offer competitive yields amid global volatility.

4. Hedge Fiscal Risks: Consider Treasury futures or inflation swaps to protect against potential supply shocks from increased issuance.

Conclusion: A Market in Transition

The U.S. Treasury market is at a crossroads, with yields reflecting a delicate balance between Fed easing and fiscal uncertainty. As the August nonfarm payrolls report looms—expected to show 75,000 jobs added—traders will be watching for confirmation of a labor market slowdown and the Fed's response. For now, the bond market's message is clear: investors are betting on a softer landing, but they're not taking any chances.

In this environment, tactical allocations that prioritize flexibility, income, and risk mitigation will be key. The yield curve may be flattening, but the opportunities for those who navigate it wisely are growing.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet