U.S. Treasury Borrowing Plans and Debt Strategy: Navigating Fiscal Caution in a Divided Market

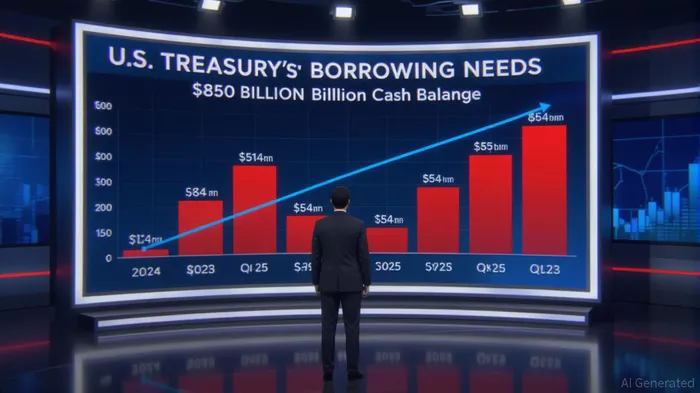

The U.S. Treasury's 2025 borrowing strategy reveals a delicate balancing act between fiscal caution and the risks of prolonged low-yield borrowing. For the April–June and July–September quarters, the Treasury aims to issue $514 billion and $554 billion in privately-held net marketable debt, respectively, assuming stable cash balances of $850 billion. These figures, while reflecting a conservative approach to debt management, underscore the growing challenge of financing a government with a fiscal deficit of 6.4% of GDP—the highest since 1947. The strategy hinges on maintaining auction sizes for nominal coupon securities and incremental increases in Treasury Inflation-Protected Securities (TIPS) to stabilize investor expectations. Yet, the market's divided outlook on fiscal sustainability and economic growth suggests that this path is far from certain.

Fiscal Caution: A Double-Edged Sword

The Treasury's emphasis on consistency in debt issuance—such as maintaining $125 billion in May 2025 to refund maturing debt—signals a desire to avoid abrupt market shocks. By sticking to regular auction sizes and avoiding large-scale refinancings, the Treasury aims to reduce volatility in yields and ensure steady access to capital. This approach is further reinforced by its commitment to enhancing buyback programs, which could stabilize liquidity and lower borrowing costs over time. However, critics argue that this cautious strategy risks entrenching long-term fiscal imbalances. With interest rates at 4.23% for the 10-year Treasury (as of June 2025), the government is locking in low-cost debt at a time when inflation and geopolitical uncertainties could force future rate hikes.

The Treasury's reliance on low-yield borrowing also masks a deeper structural issue: the rising share of federal spending allocated to net interest. In 2024, interest payments surpassed defense spending, signaling a shift in fiscal priorities that could erode long-term economic resilience. While the current strategy avoids immediate market panic, it fails to address the elephant in the room—how to reduce a debt-to-GDP ratio that has climbed to 128% (as of Q1 2025). Without meaningful reforms, the Treasury's “steady-as-she-goes” approach may prove insufficient to restore fiscal credibility.

A Divided Wall Street: Recession Fears vs. Resilience

Market analysts remain split on the implications of the Treasury's borrowing plans. On one side, optimists point to the U.S. economy's resilience. Despite a slowdown in Q1 2025 (0.4% GDP growth at an annual rate), labor markets held firm, with unemployment averaging 4.1% and job openings stabilizing at 7.7 million. Inflation, too, has moderated, with the 12-month CPI dropping to 2.4% by March 2025. These trends suggest that the economy can withstand the Treasury's borrowing surge without triggering a liquidity crisis.

On the other hand, skeptics warn of a perfect storm. The Wall Street Journal's April 2025 survey noted a 45% probability of a recession within 12 months, driven by concerns over trade policy, fiscal drag, and household fragility. For instance, credit card debt among lower-income households has surged to $1.2 trillion, with delinquency rates hitting a 13-year high. A prolonged economic downturn could force the Treasury to borrow even more aggressively, exacerbating fiscal imbalances. Meanwhile, the expiration of key provisions in the 2017 Tax Cuts and Jobs Act in 2026 looms as a potential drag on growth, further complicating the borrowing outlook.

Investment Opportunities in a High-Yield Environment

For investors, the Treasury's strategy presents both risks and opportunities. The steepening yield curve—driven by rising long-term rates and stable short-term rates—has created a favorable environment for long-duration bonds. Historically, investors who hold long-term Treasuries during periods of yield convergence have reaped significant returns. For example, the 30-year Treasury yield climbed to 4.77% by mid-2025, offering a compelling entry point for those anticipating future rate cuts.

TIPS, which adjust for inflation, have also gained traction. The Treasury's incremental increases in TIPS auction sizes (e.g., $21 billion for the July 2025 new issue) signal a recognition of inflation risks. Investors seeking to hedge against a potential resurgence in prices might find TIPS particularly attractive, especially as core CPI remains at 3.0%. Additionally, high-yield corporate bonds have outperformed Treasuries in Q2 2025, with the Bloomberg U.S. High Yield Composite returning 3.5% for the quarter. This outperformance reflects strong corporate earnings and a flight to risk in a low-recession environment.

However, caution is warranted. A sharp rise in inflation or a breakdown in trade negotiations could force the Federal Reserve to delay rate cuts, pushing long-term yields higher and eroding bond prices. Diversification across asset classes—including equities, alternatives, and international bonds—remains critical. For instance, the MSCIMSCI-- All Country World Index ex-US has outperformed U.S. equities in 2025, offering a counterbalance to domestic fiscal risks.

Conclusion: Strategic Positioning in Uncertain Times

The U.S. Treasury's 2025 borrowing strategy reflects a pragmatic but short-term view of fiscal sustainability. While its conservative approach to debt issuance has minimized immediate market jitters, it fails to address the long-term risks of rising interest payments and a bloated debt burden. For investors, the key lies in strategic positioning: capitalizing on the current high-yield environment while hedging against potential shocks. A diversified portfolio that includes long-term Treasuries, TIPS, and international assets can navigate the divided market outlook. As the Treasury prepares to unveil its next quarterly refunding plan on July 30, 2025, investors must remain vigilant—balancing optimism about the economy's resilience with caution about the fragility of its fiscal foundations.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet