Trade Idea: Overweight Energy🛢️ Stocks? Think Twice⚠️

Due to the closure of the Strait of Hormuz, oil supply is indeed being severely disrupted, pushing prices sharply higher and keeping them elevated around the $100 level. Energy stocks are significantly outperforming, while most other equities are under pressure. The question is: should investors overweight energy stocks?

Lance Roberts points out that oil price spikes driven by supply shortages are likely temporary. Moreover, the United States is no longer dependent on foreign oil, and the economy’s reliance on energy is far lower than it was in the 1970s.

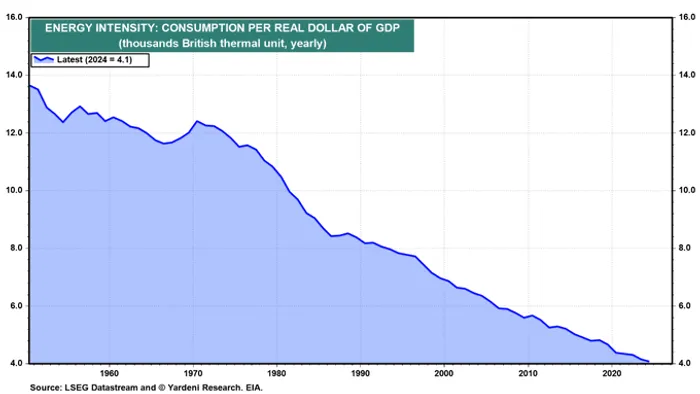

Data presented by Ed Yardeni shows that the U.S. economy now requires significantly less energy per unit of GDP than in previous decades. This reflects both efficiency gains and a structural shift away from manufacturing toward services. As a result, oil price spikes are less inflationary and cause less damage to real economic activity than in the past, when energy intensity was much higher.

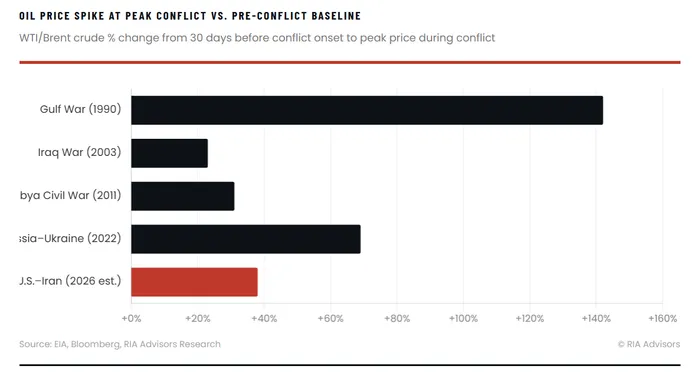

Oil’s reaction to military conflict follows a highly consistent pattern—so consistent that it can almost be used as a timing tool. Whenever conflict emerges near major oil transport routes, crude prices rise, sometimes sharply. Since late February, escalating tensions between the U.S. and Iran have already been reflected in a risk premium in WTIWTI-- prices. However, history suggests that investors should not focus on the spike itself, but rather on what comes next—the decline.

Looking back over the past 40 years, every major conflict affecting Middle Eastern or Russian oil supply has triggered an initial surge in crude prices. During the 1990 Gulf War, WTI rose from around $17 to over $40 in less than three months, but by early 1991, after coalition forces completed their mission, prices had fallen back below $20.

The 2011 Libya conflict followed the same pattern: Brent crude rose by 31%, only to fully retrace its gains within six months after a ceasefire. The clearest example is the February 2022 Russia–Ukraine war: WTI peaked at $130 in March and then trended lower over the next 18 months as markets gradually absorbed the supply disruption premium.

A similar pattern is likely today. As the saying goes, “This too shall pass.” Markets tend to price in worst-case supply disruptions at the onset of conflict, but such disruptions rarely prove as persistent as initially feared. The U.S. and Iran are engaging in negotiations, the Strait of Hormuz is gradually reopening to non-belligerent nations, and countries are tapping strategic petroleum reserves. Oil prices are therefore expected to decline over the coming months.

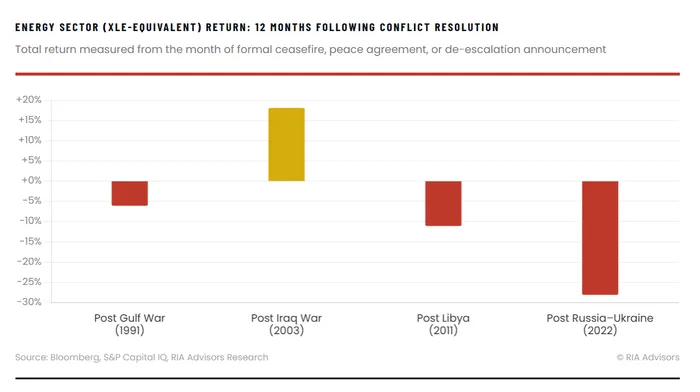

Turning to energy equities, funds tracking oil companies—such as XLE—have attracted significant inflows, based on the logic that higher oil prices directly boost earnings. This is true in the short term. However, what investors often overlook is that energy companies rarely retain these windfall profits for long. Governments do not tolerate prolonged high oil prices; political pressure inevitably leads to increased production mandates or windfall taxes. Moreover, once the crisis subsides and oil prices fall, energy stock valuations tend to revert quickly.

The Iraq War in 2003 was a rare exception, where energy stocks continued rising until 2007. At the time, shale oil had not yet emerged, markets feared a structural peak in oil supply, and the global economy was booming—fueled in part by China’s rapid growth. However, as with all commodities, high prices eventually lead to innovation and increased supply. In oil’s case, the shale revolution significantly expanded supply, and combined with the 2008 financial crisis, oil prices collapsed.

Lance Roberts summarizes: “The trade that looks obvious at the start of a conflict—long energy—is almost never the trade that works through its resolution.” When the supply crisis eases, it becomes a signal to sell energy stocks, not to continue holding them.

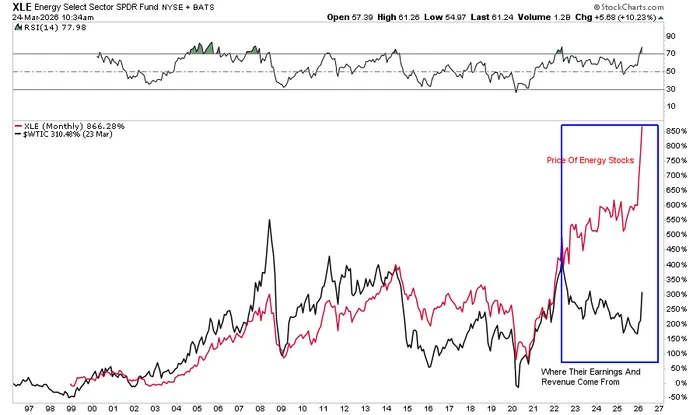

Looking at today’s market, if and when the Iran situation moves toward de-escalation, the playbook suggests trimming energy exposure into current strength. This is especially relevant given that energy stocks have deviated significantly from long-term historical norms in terms of earnings and revenue composition. The current level of speculation is likely to reverse more sharply than in past cycles.

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet