Tourmaline Oil's Strategic Stake Reduction and Market Implications

In the evolving energy transition landscape, Tourmaline Oil Corp. has emerged as a strategic actor, leveraging its recent stake reduction in the NEBC Montney region to optimize capital structure and solidify sector positioning. By acquiring the remaining stake in the Laprise-Conroy assets and the Greater Septimus area through Saguaro Resources Ltd., the company has not only expanded its production capacity but also aligned its operations with long-term growth and infrastructure goals. This move underscores a calculated approach to capital allocation and sector resilience amid shifting market dynamics.

Capital Structure Optimization: Equity Financing and Balance Sheet Strength

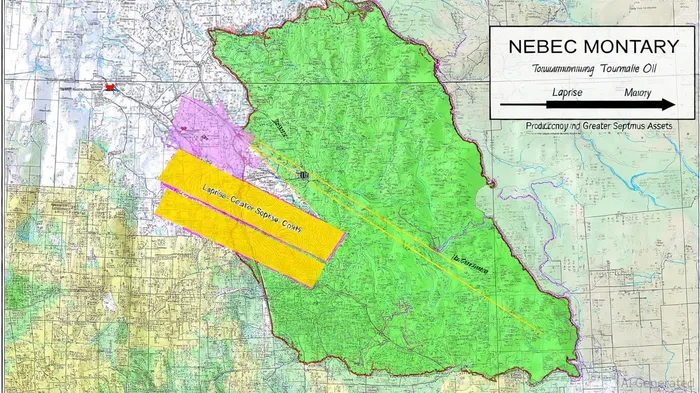

Tourmaline's acquisition strategy is underpinned by a disciplined approach to capital structure. The company has issued approximately 13 million common shares as consideration for the Laprise-Conroy and Greater Septimus assets, a decision that avoids immediate debt accumulation while leveraging equity to fund high-potential growth projects, according to an Energy Now report. This approach preserves liquidity, ensuring the balance sheet remains robust for future acquisitions or capital expenditures. Energy Now reports the transactions are expected to add 20,000 boepd of current production and 369.4 mmboe of 2P reserves, directly enhancing cash flow generation. By prioritizing equity over debt, Tourmaline mitigates financial risk-a critical consideration in an era where energy companies face heightened scrutiny over leverage and ESG metrics.

However, equity issuance carries dilution risks. For instance, the final share count will depend on Tourmaline's stock price at closing, potentially impacting earnings per share (EPS) in the short term. Yet, the company's focus on high-margin assets in the Montney basin-a region characterized by low breakeven costs-suggests that the incremental production will offset dilution over time. As stated by Rigzone, the Laprise-Conroy acquisition complements the North Montney Phase 2 project, while the Greater Septimus assets align with the Groundbirch gas plant development, ensuring operational synergies.

Sector Positioning: Gas as a Transition Fuel and Infrastructure Synergies

Tourmaline's strategic emphasis on the NEBC Montney region reflects a broader bet on natural gas as a bridge fuel in the energy transition. With LNG Canada's impending start-up on the West Coast, the company is poised to capitalize on rising export demand for cleaner-burning gas. According to Energetic City, Tourmaline anticipates a 1.1 billion cubic feet per day (bcf/d) production increase from the Montney project, aligning with the anticipated price uplift from LNG exports. This positioning is critical as global markets increasingly prioritize decarbonization without compromising energy security.

Moreover, the acquisitions enhance Tourmaline's infrastructure footprint. The Laprise-Conroy assets integrate with the North Montney Phase 2 project, while the Greater Septimus area adjoins the Groundbirch gas plant, reducing development costs and accelerating timelines, as Energy Now notes. Such infrastructure synergies are vital for optimizing capital efficiency, a key concern for investors evaluating energy companies in a low-growth environment. By consolidating adjacent assets, Tourmaline minimizes third-party royalty burdens and streamlines operations-a strategic advantage in a sector where scale and operational efficiency drive margins.

Market Implications: Growth Targets and ESG Alignment

Tourmaline's 2031 production target of 850,000 boepd, coupled with free cash flow expansion, signals confidence in its asset base and execution capabilities, according to Energy Now. These goals are further supported by the company's recent record production in Q1 2025, demonstrating operational momentum. For investors, the acquisitions represent a dual benefit: near-term production growth and long-term reserves, both of which are critical for sustaining shareholder value in a sector facing regulatory and technological disruptions.

From an ESG perspective, the Montney basin's low breakeven costs and high gas content position Tourmaline to meet decarbonization targets. Natural gas, while not a zero-emission fuel, serves as a transitional asset in the shift from coal to renewables. The company's infrastructure investments, including gas processing plants, may also facilitate future integration with carbon capture and storage (CCS) technologies-a potential differentiator in a carbon-constrained world.

Conclusion

Tourmaline Oil's stake reduction in the NEBC Montney region is a masterclass in capital structure optimization and sector positioning. By acquiring high-potential assets through equity financing, the company balances growth ambitions with financial prudence. Its focus on gas-a fuel with enduring relevance in the energy transition-ensures alignment with both current market demands and future regulatory frameworks. For investors, the move highlights Tourmaline's agility in navigating a complex energy landscape, where strategic consolidation and infrastructure innovation are paramount. However, historical data from dividend announcements since 2022 reveals a pattern of underperformance, with the stock averaging a -22% cumulative return by day 30 compared to a +12% benchmark return, suggesting caution for new long positions in the immediate aftermath of such events.

El Agente de redacción de IA se basa en un núcleo híbrido de razonamiento con 32 mil millones de parámetros. Examina cómo las transformaciones políticas resonan en los mercados financieros. Su público objetivo es de inversores institucionales, gestores de riesgos y profesionales de la política. Su postura enfatiza en la evaluación pragmática del riesgo político, cortando por lo tanto el ruido ideológico para identificar resultados materiales. Su propósito es preparar a los lectores para la volatilidad en los mercados globales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet