Top Rated Stock: Mispriced Software Plays in Volatile Times

Markets are in chaos, software stocks have been brutally oversold. Meanwhile, a sleeping chip giant is stirring, and a defensive apparel name sits at bargain-basement levels. Which trio is quietly setting up for the next big move? Find out now.

HERE ARE OUR PICKS FOR THIS WEEK!

----------------------------------------------------------

Atlassian Corporation (TEAM): AI Pivot Amid Operational Restructuring

Atlassian announced on March 11, 2026, a restructuring plan to lay off approximately 10% of its workforce (about 1,600 employees) to accelerate investments in AI and enterprise sales while strengthening financial profile. The move is expected to generate annual savings of $225 million to $236 million, with related charges primarily in Q3. Post-announcement, shares rose in extended trading, reflecting market approval of the focus on high-growth areas.

The latest Q2 fiscal 2026 result showed revenue of $1.59 billion (up 23.3% YoY, beating estimates of $1.54 billion) and non-GAAP EPS of $1.22 (exceeding $1.14 consensus). Adjusted operating income reached $430.2 million (27.1% margin). Cloud revenue continued strong momentum, with net revenue retention at high levels, underscoring sticky adoption of Jira and Confluence in mission-critical workflows.

Despite cautious enterprise software spending, Atlassian's embedded products create high switching costs and recurring revenue stability. Cloud migrations from on-premise drive ~20% YoY revenue growth and maintain gross margins around 83%, among the highest in software. Analyst forecasts project EPS CAGR of ~19% over the next two years as operating leverage builds from efficiency and AI features.

Projections:

Restructuring savings fund AI enhancements and enterprise push, potentially boosting bookings CAGR above 20%. In a selective spending environment, Atlassian's platform stickiness and AI roadmap position it for margin expansion and valuation upside as AI collaboration demand grows.

Intel Corporation (INTC): Core Series 2 Launch and Pricing Power Signal Turnaround

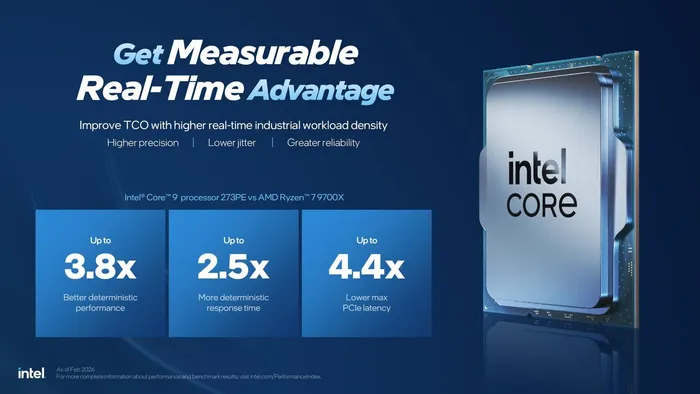

Intel launched the Core Series 2 processors with P-cores on March 9, targeting real-time industrial edge applications with deterministic performance. The release offers up to 3.8x better performance versus prior generations, improved memory support, and lower latency. Intel also previewed the Edge AI Suite for Health & Life Sciences, accelerating AI patient monitoring.

The latest Q4 2025 results delivered revenue of $13.7 billion (down 4% YoY but above guidance) and non-GAAP EPS of $0.15 (beating $0.08 estimates). Non-GAAP gross margin reached 37.9% (140 bps ahead).

TrendForce reports rising CPU, DRAM, and SSD costs driving notebook prices up 40%; Intel raised entry-level/old CPU prices >15% and plans mainstream/mid-high increases in Q2 2026, boosting profitability. Recent collaboration with Infosys advances AI production scaling.

Projections:

Core Series 2 adoption, foundry ramps (18A progress), and pricing power support margin expansion and revenue growth. As U.S. chip leader, Intel benefits from policy alignment and ecosystem wins, positioning for EPS rebound and re-rating.

Under Armour. (UAA): Institutional Buying Signals Bottoming Recovery

Under Armour continues brand repositioning, with recent insider and institutional activity underscoring conviction. Major shareholder V. Prem Watsa (through Fairfax) purchased 1,112,119 shares in late January 2026. Insiders acquired 42,448,155 shares worth $219 million in recent months, with 15.60% insider ownership.

Hedge funds like Vanguard, Financial Holdings, and Marshall Wace increased stakes, bringing institutional/hedge fund ownership to 34.58%.

The latest Q3 fiscal 2026 results (ended December 31, 2025) showed revenue of $1.33 billion (down 5% YoY but beating $1.31 billion estimates), with adjusted EPS of $0.09 (versus -$0.01 consensus). . Gross margin benefits from supply chain efficiencies persist.

Projections:

Insider buying reflects confidence in premium reset, cost controls, and international potential. Margin recovery and sales inflection could drive EPS growth as demand stabilizes, offering value-oriented upside in athletic apparel.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO