Top Rated Stock: Defensive Winners Immune to High Oil Prices

High oil prices are creating widespread turbulence, yet these defensive stocks are largely insulated thanks to robust hedging programs, pricing power, and stable demand. Discover the trio best positioned to weather the storm.

HERE ARE OUR PICKS FOR THIS WEEK!

----------------------------------------------------------

Linde plc (LIN): Industrial Gas Leader with Clean Energy and Efficiency Tailwinds

Linde plc reported solid full-year and Q4 2025 results. Q4 revenue was $8.76 billion (up 6.3% YoY), beating estimates, while adjusted EPS came in at $4.20, slightly ahead of consensus.

Full-year sales reached $34.0 billion (up 3% YoY), with operating profit of $10.1 billion (up 4%) and adjusted EPS of $16.46 (up 6%). Operating cash flow for the year rose 10% to $10.4 billion, even as capital expenditure increased 17% to $5.3 billion to support long-term growth projects.

Linde continues to benefit from its diversified industrial gas portfolio and strong positioning in high-growth areas. Recently, NH3 Clean Energy appointed LindeLIN-- Engineering to deliver Front End Engineering and Design (FEED) for the WAH2 clean ammonia project in Western Australia.

Additionally, Bisedge was appointed as the exclusive dealer for Linde Material Handling products in South Africa effective April 1, 2026, expanding Linde’s footprint in sustainable logistics across the region.

The cryogenic vaporizer market is projected to grow from $0.52 billion in 2026 to $0.72 billion by 2031 at a 6.5% CAGR, supporting Linde’s industrial and energy transition exposure.

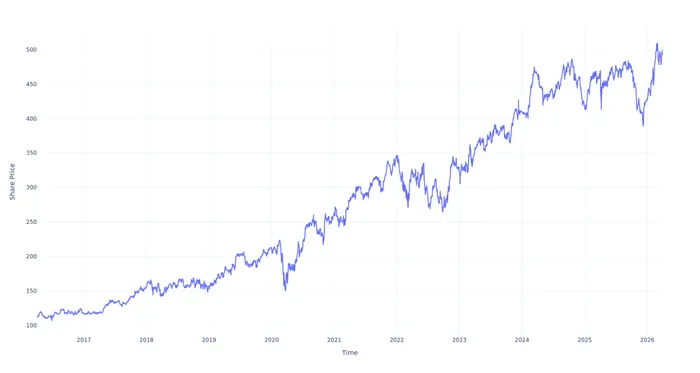

Over the past 10 years, Linde has outperformed the broader market by 3.53% annually, delivering an average return of 15.89%, a trend supported by its resilient business model, pricing power, and focus on high-return projects.

Linde's Performance Over Last 10 Years

Outlook:

Linde’s focus on clean energy (hydrogen, ammonia), efficiency gains, and geographic expansion should drive mid-single-digit revenue growth and continued margin expansion through 2027–2028. In a market full of uncertainty, LINLIN-- stands out as a high-quality defensive compounder with defensive qualities and long-term growth levers.

McDonald's Corporation (MCD): Value Leadership in a Cost-Conscious Environment

McDonald’s reported strong Q4 2025 results. Global comparable sales rose 5.7% (beating estimates), with U.S. comps up a robust 6.8% — the strongest pace in two years — driven by positive traffic and check growth. Revenue increased 10% to $7.01 billion, while adjusted EPS reached $3.12, exceeding consensus of $3.05. Full-year performance reflected successful recovery in guest counts, particularly among lower-income consumers.

Starting April 21, 2026, McDonald’s will expand its value offerings with a new Under $3 Menu (replacing the previous buy-one-add-one deal) and a $4 Breakfast Meal Deal, alongside existing lunch and dinner value options.

This “McValue 2.0” strategy aims to further strengthen affordability perception and recapture price-sensitive diners. The company’s robust commodity hedging program has effectively shielded margins from short-term volatility caused by elevated oil prices amid Middle East tensions.

Management noted no material impact from GLP-1 drugs so far, as users continue to prioritize protein-rich options already prominent on the menu. CEO Chris Kempczinski emphasized that value promotions are tactical rather than permanent subsidies, helping preserve long-term profitability.

Outlook:

Continued value menu momentum, international growth, and operational efficiencies should support mid-single-digit comparable sales growth and stable-to-expanding margins in 2026. MCD remains a defensive consumer staple with proven ability to adapt to economic pressures while delivering consistent shareholder returns.

Under Armour (UAA): Insider Buying and Pricing Power in a Challenging Retail Landscape

Under Armour reported Q3 fiscal 2026 results (ended December 31, 2025) on February 6, 2026, with revenue of $1.33 billion (down 5% YoY but beating estimates). Adjusted EPS turned positive at $0.09, significantly ahead of the consensus loss estimate. Gross margin improved thanks to supply chain efficiencies and reduced promotional activity, though North America sales remained under pressure.

A standout development has been substantial insider and institutional buying, signaling confidence in the ongoing turnaround. Major shareholder V. Prem Watsa (Fairfax) purchased millions of shares in recent months, with insiders collectively acquiring over 42 million shares valued at approximately $219 million in the last three months. Insider ownership stands at 15.60%, while institutional and hedge fund ownership (including Vanguard and Marshall Wace) has risen to 34.58%.

With potential cost pressures from Middle East conflicts possibly pushing apparel prices up 1% in the near term and 4–10% later in the year (as noted by industry peers like Next and H&M), Under Armour has room to implement selective price increases to protect and expand margins as the brand reset progresses.

Outlook:

Cost discipline, reduced discounting, international stabilization, and potential pricing power should drive margin expansion and sales inflection in fiscal 2027. UAA represents a classic mispriced recovery story with meaningful upside for patient investors.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO