Tomato Tariffs: A Spicy New Era for U.S. Agriculture and Supply Chains

The U.S. Commerce Department's imposition of a 17% tariff on Mexican tomato imports, effective July 14, 2025, marks a seismic shift in North American agricultural trade. The abrupt withdrawal from the 29-year Tomato Suspension Agreement—a pact designed to prevent “dumping” by Mexican growers—has ignited a chain reaction of price volatility, supply chain reconfigurations, and political brinkmanship. For investors, this is a moment to scrutinize the interplay of trade policy, commodity markets, and corporate resilience.

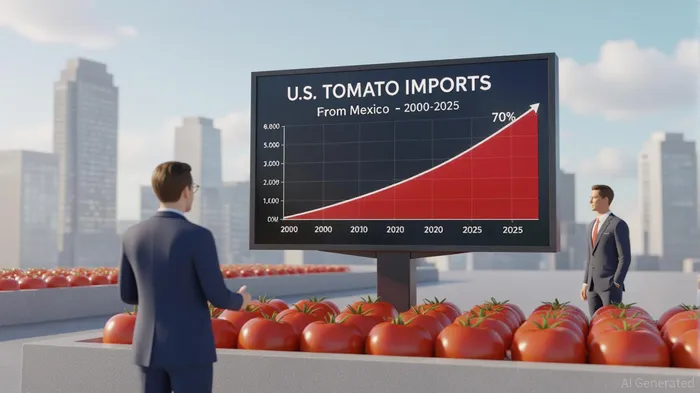

The Immediate Market Tremors

Mexican tomatoes account for 70% of the U.S. market, valued at $3 billion annually. With the tariff in place, economists project an 8.5%–10% rise in U.S. retail tomato prices by year-end, particularly during off-peak seasons (October–February) when domestic production wanes. . This surge could hit grocers and restaurants hard: small businesses like Appollonia's Pizzeria in Los Angeles face margin squeezes, while chains like KrogerKR-- and WalmartWMT-- may see consumer backlash over sticker shock.

.

.

Winners and Losers in the Supply Chain

Domestic Growers: The Silver Lining for Florida and California

Florida's tomato industry, which has seen its market share shrink from 70% to 30% since the 1990s, now stands to benefit. The Florida Tomato Exchange estimates that U.S. production could rise 5%–7% in 2026 as growers ramp up operations. Investors might look to land trusts or agribusiness firms with exposure to domestic tomato farming.

Mexican Exporters: Diversifying or Doubling Down?

Mexican producers, facing a 5% drop in U.S. exports, may pivot to markets like Canada, Europe, or Asia. However, logistical hurdles and trade agreements (e.g., USMCA) could limit their flexibility. .

Retailers and Restaurants: A Balancing Act

Grocery chains may stockpile tomatoes during peak U.S. harvests (April–June) or source alternatives like greenhouse-grown varieties. Restaurants could substitute cheaper produce or absorb costs temporarily, but prolonged price spikes might force menu price hikes—a risky move in a cost-sensitive market.

Historical Precedent: Tariffs as a Catalyst for Volatility

The 1996 Tomato Agreement, which set minimum prices for Mexican imports, initially stabilized prices but eroded U.S. competitiveness over time. The 2008–2009 recession saw tomato prices spike 15% due to similar trade disputes, offering a cautionary template. Investors who shorted agricultural ETFs (e.g., TECS) during that period profited, while long positions in logistics firms (e.g., JBHT, XPO) thrived as supply chains reorganized.

Contingency Strategies for Investors

Short-Term Plays in Commodity Futures

The CME's tomato futures contracts (if available) or broader agri-commodity ETFs (e.g., MOO) could capture volatility. A tactical short position in Mexican peso-denominated bonds (EWW) might also hedge against retaliatory tariffs.Logistics and Storage Stocks

Companies like Americold (ACOLD) or LineageLINE-- Logistics (private equity-backed) could benefit from increased cold-storage demand as U.S. growers seek to manage seasonal surpluses.Diversification in Agribusiness Tech

Firms developing vertical farming or AI-driven yield optimization (e.g., AeroFarms, Plenty) may attract capital as growers seek efficiency gains amid higher costs.

Risks and Considerations

- Political Volatility: Mexico could retaliate with tariffs on U.S. goods like beef or machinery, further straining bilateral relations.

- Weather and Climate: A poor U.S. harvest (e.g., due to drought) could amplify price spikes, while a bumper crop in Mexico might undercut the tariff's intended impact.

- Consumer Sentiment: Rising food costs could trigger inflation fears, pressuring the Federal Reserve to delay rate cuts—a double-edged sword for equity markets.

Conclusion: A Volatile Opportunity

The tomato tariff is a microcosm of broader trade tensions reshaping global supply chains. For investors, the key is to treat this as a short-term trading opportunity rather than a long-term bet. Focus on liquidity, hedging tools, and companies with adaptive supply chain strategies. As one grower put it: “Tomatoes rot fast—so do investment decisions.”

.

The path forward is clear: monitor trade negotiations closely, price in volatility, and bet on agility in a spicier agricultural landscape.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet