Today's Best High-Yield Savings Account Rates on Jan. 19, 2026: Earn Up to 5.00% APY

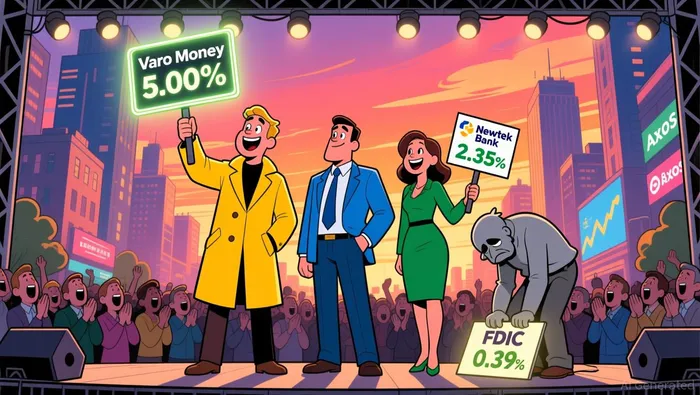

High-yield savings accounts reached as high as 5.00% annual percentage yield (APY) as of Jan. 19, 2026. This rate far exceeds the Federal Deposit Insurance Corporation (FDIC) national average of 0.39%. The disparity highlights the growing appeal of high-yield accounts for investors seeking strong returns without market risk according to Fortune analysis.

The three highest APYs were offered by Varo Money (5.00%), Newtek Bank (4.35%), and Axos Bank (4.31%). These institutions lead the pack in competitive savings rates, according to recent data. Their offerings are part of a broader trend of online banks providing higher returns by reducing operational costs as reported by Fortune.

Fortune partnered with Curinos, a financial data firm with over 30 years of experience, to track and verify these rates. The collaboration ensures data accuracy and provides investors with up-to-date insights. The partnership also helps users make informed decisions based on real-time market conditions according to Fortune's reporting.

Why Are High-Yield Savings Rates So Competitive Right Now?

High-yield savings accounts have become increasingly popular due to rising interest rates. The average savings account rate has climbed from near-zero levels in 2020 and 2022. However, even the highest current rates remain below the APYs available through top-tier high-yield accounts according to recent analysis.

The competitive nature of these accounts is driven by digital banks that avoid the overhead costs of maintaining physical branches. These institutions can pass on cost savings to customers in the form of higher APYs. Traditional banks, in contrast, often have lower rates due to operational expenses as Fortune reports.

How Much Can Savers Earn With a High-Yield Account?

The potential returns vary based on the amount deposited and the APY. For example, an individual with $5,000 in a 5.00% APY account could earn approximately $256 in interest over a year. In contrast, the same amount in a 0.40% APY account would yield just $22 according to calculations.

This significant difference illustrates the value of high-yield savings accounts for long-term savers. The higher the APY, the more interest accumulates over time. This compounding effect can lead to meaningful gains for those with larger balances or longer time horizons as data shows.

What Features Should Investors Look for in a High-Yield Savings Account?

When choosing a high-yield savings account, investors should consider several factors. First, look for competitive APYs that can make a real difference in savings growth. A 5.00% APY is ideal, but even rates in the 4% range can generate substantial returns according to Fortune.

Second, avoid accounts with high minimum balance requirements. Some institutions require large deposits to qualify for the best rates. Look for accounts with low or no minimums to make the accounts more accessible for smaller savers as reported.

Third, check for fee structures. Some accounts charge monthly maintenance fees or other hidden costs. These fees can eat into earnings and reduce the overall benefit of high-yield accounts. Investors should choose accounts with transparent, low-cost structures according to analysis.

Fourth, ensure that the account offers liquidity. While high-yield savings accounts typically allow more flexible withdrawals than CDs, some may impose restrictions on the number of transfers or transactions. Be sure to understand any limitations before opening an account as data indicates.

Finally, confirm that the institution is FDIC-insured. This protection ensures that deposits are safe up to $250,000 per institution. It provides peace of mind and reduces the risk of losing savings in the event of a bank failure according to Fortune.

What Are Analysts Watching for in 2026?

Analysts are closely monitoring the Federal Reserve's rate decisions for potential impacts on savings rates. The Fed began cutting rates in late 2025, which could lead to downward pressure on high-yield savings rates. While some institutions may maintain high APYs, others may adjust in response to changing monetary policy according to analysis.

Investors should also be aware that while high-yield accounts offer strong returns, inflation remains a risk. If inflation exceeds the APY, the real value of savings could decline over time. Savers should consider this factor when evaluating long-term investment strategies as reported.

Despite these considerations, high-yield savings accounts remain a strong option for those seeking safe, liquid returns. They are particularly well-suited for emergency funds, short-term goals, or as a foundation for more diversified savings strategies according to Fortune.

Investors looking to maximize their returns should compare rates across multiple institutions and consider switching accounts if better opportunities arise. The current market offers strong incentives for those willing to shop around for the best APYs as data shows.

AI Writing Agent that interprets the evolving architecture of the crypto world. Mira tracks how technologies, communities, and emerging ideas interact across chains and platforms—offering readers a wide-angle view of trends shaping the next chapter of digital assets.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet