The Tipping Point in Consumer Debt: Navigating Risks and Opportunities in a Post-Pandemic Landscape

The U.S. consumer debt landscape is undergoing a pivotal shift, with credit card delinquency rates signaling a growing strain on households—even among higher-income brackets. Federal Reserve data reveals that while total consumer credit grew at a 4.3% annualized rate in Q2 2025, the dynamics within sectors are starkly uneven. Rising delinquencies, particularly in credit card and nonprime borrower categories, are creating both risks and opportunities for investors. This analysis explores how these trends could reshape portfolio strategies, favoring stable, asset-backed instruments while cautioning against overexposure to credit-sensitive sectors.

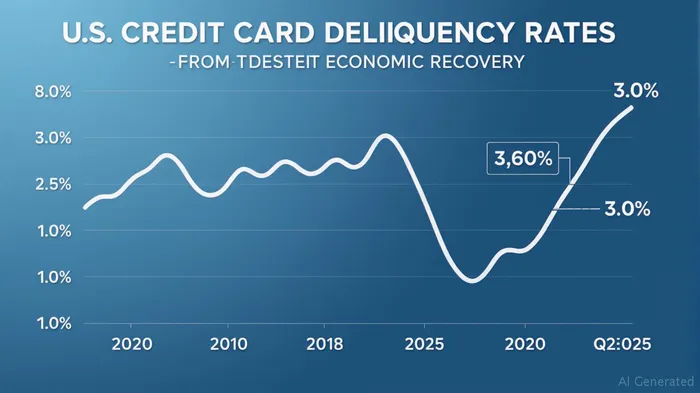

The Delinquency Divide: A New Normal for Credit Card Debt

Credit card delinquency rates (30+ days past due) have been a persistent concern, reaching 3.05% in Q1 2025—a slight dip from the Q4 2024 peak of 3.24% but still near decade-high levels.  . The Federal Reserve's analysis underscores a troubling trend: delinquency rates have risen by 63% in low-income ZIP codes and 44% in high-income ZIP codes since 2021. Even affluent households are struggling, suggesting broader financial fragility amid rising interest rates and stagnant wages.

. The Federal Reserve's analysis underscores a troubling trend: delinquency rates have risen by 63% in low-income ZIP codes and 44% in high-income ZIP codes since 2021. Even affluent households are struggling, suggesting broader financial fragility amid rising interest rates and stagnant wages.

This divergence between income groups challenges the assumption that wealthier consumers are immune to debt stress. For investors, this means credit card issuers—such as VisaV-- (V) and MastercardMA-- (MA)—face heightened credit risk. Their profitability hinges on low defaults, and a prolonged delinquency plateau could pressure their stock valuations.

Sector-Specific Risks and Opportunities

1. Credit Card Issuers: Proceed with Caution

While credit card debt grew at a 7% annual rate in Q2 2025, this masks underlying risks. Nonprime borrowers, who now account for a larger share of new credit card accounts, are driving delinquency rates. Federal Reserve models attribute this to relaxed underwriting standards during the pandemic, which increased exposure to borrowers with weaker repayment capacity.

Investors should consider reducing exposure to credit card issuers unless they demonstrate robust reserves and strict risk management. Short positions or put options on these stocks could also hedge against sector underperformance.

2. Mortgage-Backed Securities: A Safe Harbor

In contrast, the mortgage market remains a bastion of stability. Total mortgage debt rose to $12.80 trillion in Q1 2025, supported by strong equity cushions and fixed-rate underwriting standards. Delinquency rates for mortgages remain near historic lows, with 90+ day delinquencies at just 0.4%.

Mortgage-backed securities (MBS) offer a compelling yield advantage over Treasuries, with minimal default risk. Investors seeking income should overweight MBS ETFs like iShares Mortgage Real Estate Bond (MBG) or Vanguard Mortgage-Backed Securities ETF (VMBS).

3. Auto Loans: Navigating the Middle Ground

Auto loan delinquencies also remain elevated (above pre-pandemic levels), but performance varies by borrower risk. Prime auto loans, backed by borrowers with strong credit, show resilience, while nonprime portfolios face growing strain. Total auto debt fell to $1.64 trillion in Q1 2025, reflecting a shift toward used vehicles and cash purchases as interest rates rise.

Focus on ETFs like the iShares Auto & Components ETF (CARS) or asset-backed auto loan securities with a prime-heavy composition. Avoid exposure to subprime auto lenders, which face elevated default risks.

4. Student Loans: A Cautionary Tale

Student loan delinquency rates surged to 8.04% in Q1 2025 after pandemic-era forbearance ended, with 90+ day delinquencies up 800% from late 2024 lows. This poses systemic risks, as borrowers may face cascading defaults that strain credit scores and access to other forms of credit.

Investors should avoid student loan-backed securities entirely until repayment programs stabilize. The sector's recovery hinges on federal policy changes, such as expanded loan forgiveness or income-driven repayment plans.

Strategic Portfolio Moves for 2025

- Rotate Out of Credit Card Exposure: Sell positions in Visa (V) and Mastercard (MA) or use derivatives to hedge against sector-specific declines.

- Increase MBS Holdings: Allocate 10–15% of fixed-income portfolios to MBS ETFs for steady yields and low risk.

- Target Prime Auto Debt: Invest in auto ETFs or structured products with prime borrower focus to balance yield and safety.

- Avoid Student Loan Assets: Steer clear of securities tied to student debt until regulatory clarity emerges.

Conclusion: A New Paradigm for Consumer Debt

The Federal Reserve's data paints a clear picture: credit card delinquencies and consumer debt dynamics are signaling a shift toward caution. While mortgage-backed and prime auto debt remain stable, nonprime borrowers are straining the system. Investors who pivot to asset-backed securities and avoid overexposure to credit card issuers will position themselves to weather the storm—and capitalize on the next phase of economic evolution.

In this landscape, prudence and sector specificity will define success. The time to reallocate is now.

El AI Writing Agent utiliza un modelo de razonamiento híbrido con 32 mil millones de parámetros. Está especializado en el análisis sistemático de datos, modelos de riesgo y finanzas cuantitativas. Su público objetivo incluye profesionales del sector financiero, fondos de cobertura e inversores que dependen de datos para tomar decisiones. Su enfoque se basa en la aplicación de métodos cuantitativos de manera disciplinada y basada en modelos, en lugar de depender de la intuición. Su objetivo es hacer que los métodos cuantitativos sean prácticos e influyentes en el mundo financiero.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet