Tesla Q1 Earnings Preview: Musk's Crossroads as Fundamentals Falter, Faith Endures

As TeslaTSLA-- (TSLA) prepares to report its Q1 2025 earnings after the close on Tuesday, the company finds itself at the heart of one of the market’s most heated bull-bear debates. Bulls, led by analysts like Dan Ives of Wedbush, argue that the long-term upside tied to Tesla’s autonomous driving (FSD), robotics (Optimus), and energy segments vastly outweighs near-term volatility. Bears, including skeptics at Wells FargoWFC-- and BarclaysBCS--, counter that weakening fundamentals, political distractions from CEO Elon Musk’s role in the Trump administration, and delivery disappointments threaten to erode Tesla’s brand and valuation. The key tension? Tesla is no longer being judged by what it earns today—but by what it promises to be tomorrow.

Expectations: Weak Deliveries, Flat Revenues, Sliding Margins

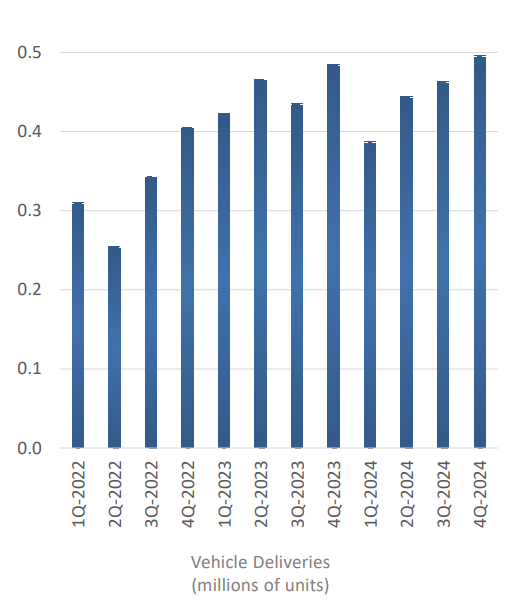

Consensus heading into the print is for adjusted EPS of $0.42 and revenue of $21.38 billion, according to FactSet. That would reflect a ~7% EPS decline and flat revenue year over year, though some more recent analyst forecasts anticipate worse. Tesla already reported Q1 deliveries of 336,681 units, down 13% YoY and sharply below the Street’s 390,000+ estimate. Model 3/Y deliveries declined 12%, while higher-margin models like the S, X, and Cybertruck cratered 46% quarter-over-quarter—a "disaster" in the words of Gerber Kawasaki.

Analyst Gene Munster expects full-year delivery estimates to be reset following the miss. He sees FY25 deliveries falling ~5% versus current consensus of +3%, calling 2025 “a throwaway year” that sets the stage for a 2026 rebound. Meanwhile, Morgan Stanley slashed its FY25 EPS forecast by 20%, cutting its price target to $410, while Wells dropped theirs to $130, citing “lower leverage on low volumes.”

Key Issues to Watch on the Call

Investors will be laser-focused on several strategic pillars. First, updates on the “affordable” next-generation Tesla remain critical. Multiple reports suggest a delay of at least three months, with speculation mounting that the new model may be a stripped-down Model Y rather than a clean-sheet design. As Will Rhind of GraniteShares warned, "If it’s just a bare-bones Y, the Street could be disappointed".

Second, eyes will be on progress with unsupervised FSD and Cybercab robotaxis. Musk previously announced plans to launch FSD in Austin by June, with expansion to other states by year-end. “FSD is the $1 trillion prize,” according to Ives, who warns that “Musk needs to stop the political firestorm” to fully unlock Tesla’s AI-driven valuation.

Lastly, expect questions on Musk’s ongoing role in the Department of Government Efficiency (DOGE). His political involvement is seen as a “code red” risk by some investors, with Ives stating bluntly: “If Musk stays in Washington, the damage to the brand could be permanent.”

Stock Performance and Market Sentiment

Tesla stock has plunged more than 40% year-to-date, making it the worst performer among the "Magnificent Seven". After peaking near $488 in December, shares now hover around $226, having fallen 6.3% on Monday. While the stock found support near $214, sentiment remains fragile, and many believe the outcome of this call could determine whether Tesla stabilizes—or spirals further.

Despite valuation metrics flashing red (forward PE near 96 vs. sector median of 13), bulls remain undeterred. “Tesla isn’t a car company anymore—it’s a tech/AI platform in transition,” said Morgan Stanley’s Adam Jonas. That transformation narrative remains intact—for now.

Tuesday’s call, then, is not just a quarterly update. It’s a test of belief, leadership, and strategy. For Musk and Tesla, it’s a fork-in-the-road moment.

Tesla Q4 Earnings: Fundamentals Miss, But Future-Facing Narrative Commands the Spotlight

Tesla’s Q4 2024 earnings report delivered a mixed bag for investors, as weaker-than-expected financial results were largely overshadowed by an aggressive long-term vision built on autonomous driving, robotics, and next-generation manufacturing. While headline metrics missed Street expectations, the company’s forward-looking commentary — particularly on Full Self-Driving (FSD), the Optimus robot, and its robotaxi plans — helped keep bullish sentiment afloat.

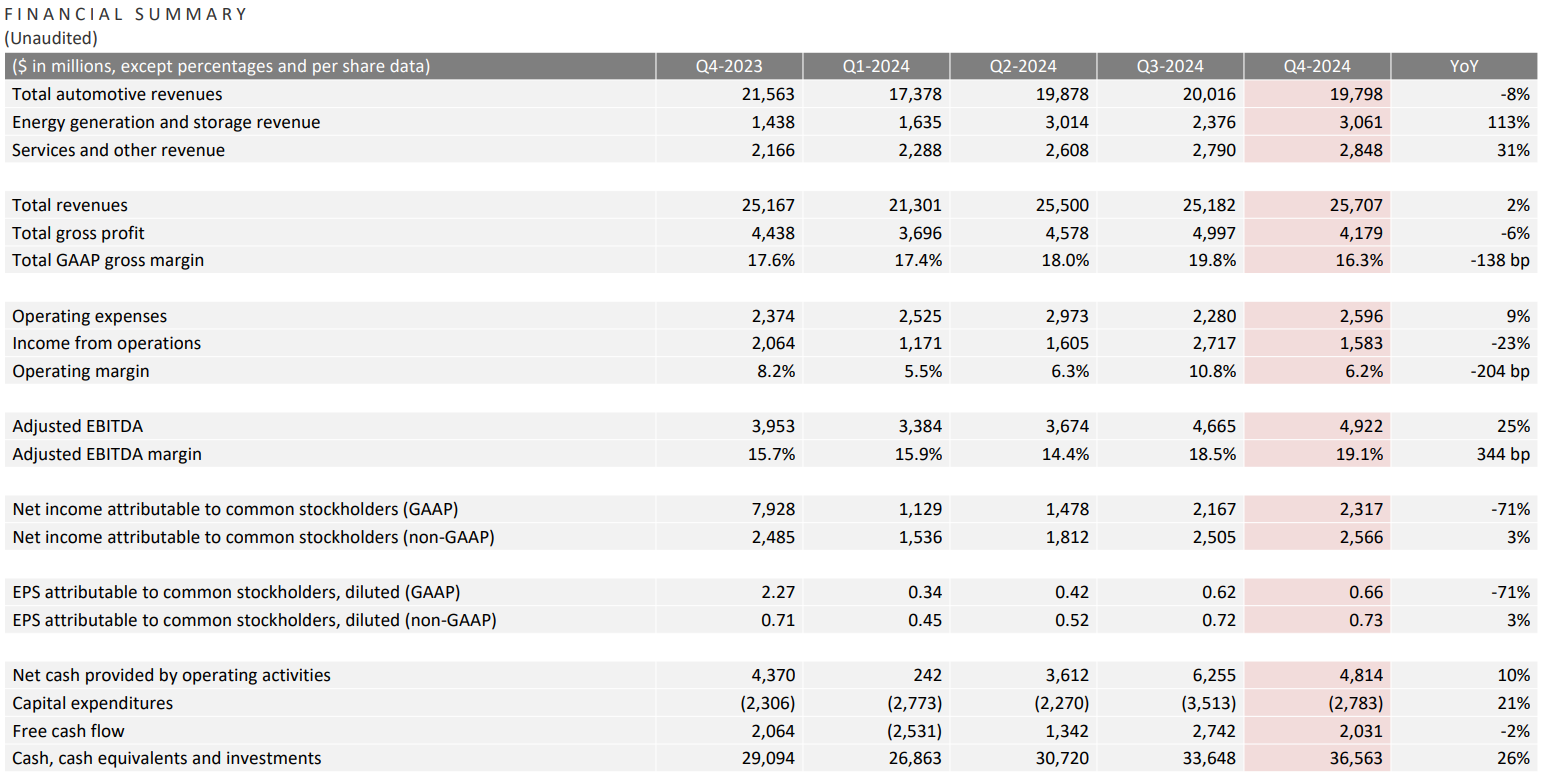

Revenue for the quarter came in at $25.71 billion, missing consensus by roughly 6%, while adjusted EPS of $0.73 slightly trailed the $0.75 forecast. Gross margin slid to 16.3% — Tesla’s lowest in over seven years — driven by heavy discounting to clear Model Y inventory and rising input costs. Operating income dropped 23% year-over-year to $1.58 billion, and auto gross margin ex-regulatory credits came in at a soft 13.6%.

Yet amid the choppy financials, Tesla produced over $2 billion in free cash flow — beating estimates — and guided to more than 60% production growth over 2024 levels, driven in part by new affordable vehicle models slated for H1 2025. The company maintained that vehicle volumes would return to growth in 2025, with additional output ramping across multiple factories.

Still, what truly drove post-earnings sentiment wasn’t what Tesla had done — but what it plans to do. CEO Elon Musk dominated the call with bold projections on autonomous technology and robotics. Tesla confirmed that it will launch an unsupervised robotaxi service in Austin by June and expects FSD software to expand to more U.S. regions later in the year. Musk also revealed that Tesla is in active licensing discussions with several automakers, reinforcing FSD’s potential as a high-margin platform business.

Analysts were particularly struck by Musk’s Optimus ambitions. The humanoid robot, which Musk claims will eventually cost less than a car, is targeting pilot production of 10,000 units in 2025, with broader commercialization beginning in 2026. Musk projected Optimus could become Tesla’s most valuable product line — an assertion met with skepticism by some, but enthusiasm by others who see AI as Tesla’s core value proposition.

Reactions across Wall Street were polarized. Bulls like Roth MKM and RBC raised price targets and reiterated Buy ratings, citing confidence in the company’s moonshot initiatives. Wedbush's Dan Ives said that investors who believe in the AI/autonomous vision are now “even more confident” in their thesis. Others, like JPMorgan and Wells Fargo, remained critical, pointing to a 38% EBIT miss and ongoing margin pressures, with PTs anchored as low as $135.

While consensus acknowledges Tesla’s near-term fundamentals remain volatile, there’s increasing agreement that the stock is being valued on its future-facing innovations rather than its quarterly earnings. Piper Sandler summed it up well: “None of this really matters for the thesis.” The real focus has shifted to autonomous licensing, volume from new low-cost models, and execution on Optimus and Cybercab.

As Tesla heads into its Q1 2025 report, investors will be watching closely for updates on these initiatives, especially tangible signs of FSD deployment, progress on lower-priced vehicle ramps, and margin stabilization. Until then, Tesla continues to trade not just on performance, but on belief.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet