Tech Stocks Sink at the Open as Oracle’s AI Spending Jitters Hit Nasdaq

Women, Divorce & Money: What Most Don’t Know Until It’s Too Late 👇

U.S. stocks opened mixed on Thursday as investors weighed a renewed selloff in major technology names against steadier trading elsewhere in the market. The Dow Jones Industrial Average rose 123.77 points, or 0.26%, to 48,181.5, while the Nasdaq Composite slid 172.39 points, or 0.73%, to 23,481.8 as Oracle’s cloud disappointment continued to reverberate through the broader AI complex. The S&P 500 fell 28.84 points, or 0.42%, to 6,857.84, extending early pressure in large-cap tech, while the Russell 2000 was nearly flat, up just 0.03 points, or 0.01%, at 254.84, signaling a cautious but more stable tone across smaller domestic companies.

Bitcoin slipped to $90,097.71, down 2.05%, extending a weeklong retreat that has coincided with softer risk appetite. Crude oil futures fell 1.47% to $57.60, continuing a downward trend driven by easing supply concerns and the Fed’s indication that liquidity conditions should improve into year-end. Gold, meanwhile, gained 0.55% to $4,248.10, reflecting demand for defensive hedges as investors parse crosscurrents in macro policy and corporate guidance. The CBOE Volatility Index edged up 0.95% to 15.92, suggesting a modest pickup in expected near-term equity swings.

The most forceful narrative shaping the morning came from Oracle’s latest results and the divergent interpretations surrounding them. While the company delivered a blockbuster $523 billion in Remaining Performance Obligations—well above the Street’s $500 billion expectation—its free cash flow swung deeply negative due to an aggressive $12 billion capex figure for the quarter. According to the AInvest analysis, free cash flow reached –$10 billion, and projected fiscal 2026 capex of roughly $50 billion, or 75% of anticipated revenue, has amplified investor concerns about leverage and funding transparency.

Wedbush, however, urged clients not to misread the quarter. In the firm’s words, “this is the number we are most focused on around the future and health of Oracle's AI buildout and strategy looking ahead.” Analysts highlighted Oracle’s sequential $69 billion RPO addition and reiterated long-term revenue growth expectations of 17% in FY26, 35% in FY27, and 47% in FY28 as the AI backlog converts. The note frames OracleORCL-- not as a point of weakness but as a “bedrock for the AI Revolution,” grouping it with Palantir, Microsoft, and Nvidia as core industry beneficiaries.

Still, the AInvest overview noted that markets reacted sharply, sending Oracle shares down 11–12% and pressuring AI-linked peers. The tension between long-term AI infrastructure demand and near-term capital intensity remains a source of volatility.

Wall Street wakes up with a post Fed hangover. Following the FOMC’s 25-basis-point cut to a 3.5%–3.75% federal-funds range, the Fed’s new dot plot was “in line with the September release,” according to Jay Hatfield of Infrastructure Capital Advisors. He added that the Fed’s move to issue $40 billion of short-term Treasurys “was viewed as bullish by some market participants but are simply a technical adjustment to accommodate year end liquidity demand.” Hatfield expects inflation to fall toward 2% by 2026, forecasts three cuts next year, and sees the 10-year Treasury drifting to 3.75%. He maintains S&P 500 targets of 7,000 for 2025 and 8,000 for 2026, citing AI-driven productivity gains.

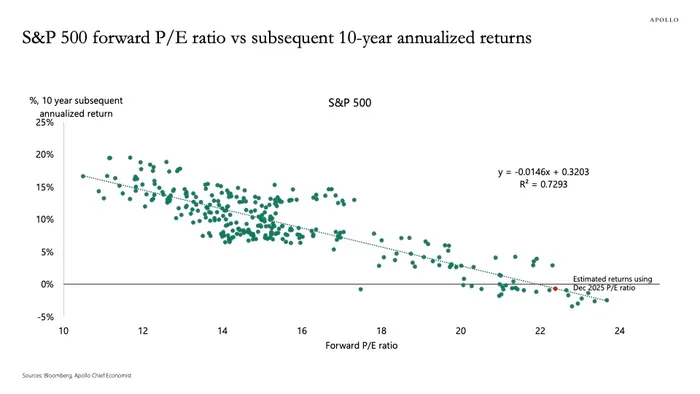

Yet the outlook for long-dated equity returns remains a subject of debate. Apollo Global Management Chief Economist Torsten Slok highlighted that the historical relationship between the S&P 500 forward price/earnings ratio and subsequent 10-year returns now points toward near-zero real equity gains over the decade ahead. His chart illustrates a tight negative correlation: valuations at current levels have historically delivered muted long-term returns.

That juxtaposition of rising AI-related capital cycles, a Fed that may continue easing, and research suggesting compressed long-horizon returns, has left investors awaiting clearer direction from corporate earnings and forthcoming macro data in the new year.

Adam Shapiro is a three-time Emmy Award–winning content creator, former network news correspondent, and founder of the multimedia production company TALKENOMICS. At AInvest, he created and launched Capital & Power, a video podcast series designed to drive engagement and establish thought leadership, while also producing original live streams, financial articles, and investor-focused video content. Previously, as a correspondent at FOX Business, Shapiro established the network’s Washington, D.C. bureau, reported from the White House, Capitol Hill, and the Federal Reserve, and secured exclusive bipartisan interviews with influential leaders. His reporting helped solidify FOX Business as the most-watched business channel on television. At the same time, his original Talkenomics series drew tens of thousands of viewers per episode through insightful conversations with policymakers, economists, and thought leaders. At Yahoo Finance, he played a critical leadership role in expanding digital programming to eight hours of live, bell-to-bell financial news coverage, dramatically increasing traffic from 68M to 104M unique monthly visitors and growing ad revenue from zero to over $50 million annually. Yahoo Finance continues to benefit from the credibility of Shapiro’s exclusive interviews with former President Donald Trump and numerous Fortune 500 CEOs.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet