Tariff-Induced Inflation and the Fed's Rate Cut Crossroads: Navigating Opportunities in a Low-Rate Landscape

The June 2025 Consumer Price Index (CPI) report revealed a critical turning point: U.S. inflation remains stubbornly stable at 2.7% annually, with core inflation (excluding food and energy) inching toward 3%. While this stability might suggest relief for policymakers, the data masks a deeper truth—tariff-driven supply chain disruptions are already nudging prices upward, and the Federal Reserve may be forced to delay rate cuts longer than markets expect. For investors, this creates a strategic opportunity to position in rate-sensitive sectors like real estate and utilities, which thrive in low-rate environments.

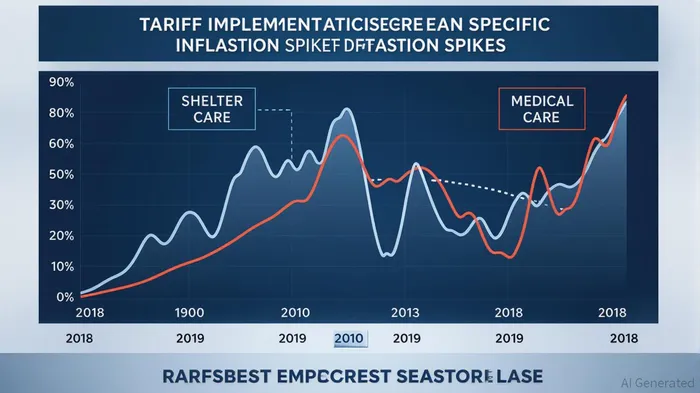

The Tariff Inflation Nexus: CPI Data and Supply Chain Pressures

The June CPI report highlights how tariffs are embedding themselves into consumer prices. Key sectors like shelter (up 3.8% annually), medical care (up 2.8%), and household furnishings (up 3.3%) saw significant price increases. Even as energy costs dipped 8.3% year-over-year, tariff-affected goods—such as furniture, appliances, and apparel—showed rising prices as businesses exhausted pre-tariff inventory buffers.

Economists like Mark Zandi of Moody'sMCO-- warn that inflation is “kicking into a higher gear,” with core goods prices set to rise further as 30% tariffs on EU imports take effect in August. The Fed, already wary of overshooting its 2% target, faces a dilemma: easing monetary policy too soon could amplify inflationary pressures, while waiting risks a slowdown in economic growth.

Why Markets Overestimate Near-Term Rate Cuts

Investors are pricing in a 50% chance of a Fed rate cut by year-end, assuming inflation will ease quickly. But the June CPI data—and the broader tariff narrative—undermine this optimism.

First, the Fed's dual mandate (price stability and full employment) prioritizes inflation control. With core CPI at 2.9% and shelter costs rising, policymakers are unlikely to risk rate cuts that could fuel overshooting. Second, tariff impacts are asymmetric: while energy and used cars may decline temporarily, shelter and services costs—representing 60% of CPI—are structural and sticky.

Historically, the Fed has been slow to cut rates during periods of tariff-driven inflation. For example, in 2018–2019, the central bank hiked rates despite trade wars, only reversing course after a sharp economic slowdown. Today's resilient labor market (unemployment at 3.5%) gives the Fed less urgency to act preemptively.

Rate-Sensitive Sectors: The Safe Harbor in a Low-Rate World

If the Fed delays cuts, investors should focus on sectors that benefit from prolonged low rates:

- Real Estate:

Low rates keep borrowing costs down for developers and make dividend-paying REITs attractive. The shelter component's 3.8% annual inflation also signals strong demand for housing, supporting property prices.

Utilities:

Regulated utilities are less sensitive to economic cycles and often outperform when rates stabilize. Their steady dividends and defensive nature align with a prolonged low-rate environment.

Dividend Stocks:

- Companies with stable cash flows and high yields, such as consumer staples giants (e.g., Procter & Gamble), will remain sought after as bond alternatives.

Risks and the Path Forward

The primary risk is an inflation surprise to the upside, which could force the Fed to tighten instead of cut. However, with energy prices volatile and global demand softening, the more likely scenario is a prolonged “wait-and-see” stance.

Investors should also monitor specific tariff-sensitive sectors for bargains. For instance, apparel stocks may bottom as retailers exhaust discounted pre-tariff inventories, while tech hardware firms reliant on imported components could see near-term volatility but long-term pricing power.

Conclusion: Position for a Fed Hold

The June CPI data underscores that tariffs are a slow-burn inflationary force, and the Fed is unlikely to ease aggressively until they subside. Markets may overestimate the timing of rate cuts, creating a mispricing opportunity. By focusing on rate-sensitive sectors like real estate and utilities, investors can capitalize on the extended low-rate environment while hedging against inflation's persistent grip.

The Fed's crossroads is an investor's crossroads too—choose wisely.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet