Sypris Gains 47% in 6 Months: Should You Buy the Stock?

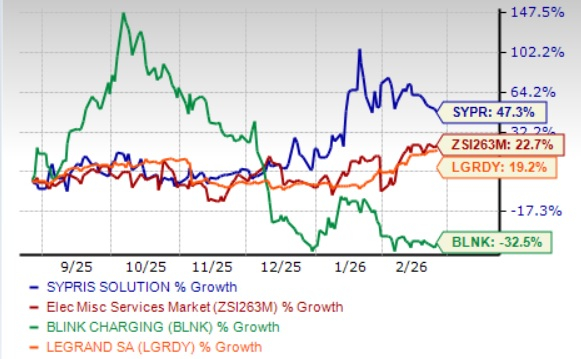

Sypris Solutions, Inc. SYPR shares have climbed 47.3% in the past six months compared with the industry’s 22.7% growth. The company has outperformed other industry players, including Blink Charging Co. BLNK and Legrand SA LGRDY. Shares of LGRDY gained 19.2%, while BLNK stock declined 32.5% in the same time frame. SyprisSYPR-- benefits from strong aerospace and defense demand, Artemis-linked backlog growth, reshoring-driven sole-source contracts, diversified end markets, and improved liquidity from operational initiatives.

Image Source: Zacks Investment Research

A Key Look Into SYPR’s Business Operations

Founded in 1997, Sypris SolutionsSYPR-- is a diversified manufacturer serving commercial vehicle, energy pipeline, aerospace, and defense markets through its two segments, Sypris Technologies and Sypris Electronics. The company produces forged, machined, welded, and heat-treated components, high-pressure pipeline products, and high-reliability electronic assemblies, often under multi-year, sole-source contracts. Its customers include major OEMs and leading aerospace and defense contractors. Sypris emphasizes lean manufacturing, advanced quality systems, engineering expertise, and continuous innovation to enhance efficiency, reduce costs and improve product reliability. Operating in the United States and Mexico, the company focuses on strategic partnerships and expanding value-added capabilities.

Sypris’ Key Tailwinds

Sypris Solutions is positioned to benefit from strengthening long-term demand in aerospace and defense markets. As of Sept. 28, 2025, Sypris Electronics reported $76.9 million in remaining performance obligations, with a majority scheduled for delivery in 2026 and 2027. This visibility supports production stability and cash flow planning. In January 2026, the Company secured an expanded follow-on award tied to NASA’s Artemis program, extending backlog through 2027 and reinforcing its role in high-reliability space electronics. Sustained U.S. defense funding and deep-space initiatives remain key structural growth drivers.

The company is also benefiting from reshoring and sole-source contract opportunities within its Technologies segment. In January 2026, Sypris Technologies entered into a long-term, sole-source agreement with a global truck OEM to supply critical AMT components for heavy trucks in North America, with production expected to begin in 2027. This award supports the customer’s North American reshoring strategy, positioning Sypris as a strategic manufacturing and logistics partner.

Another tailwind stems from the company’s diversified end-market exposure across commercial vehicles, energy infrastructure, aerospace, defense and space systems. While the Class 8 truck cycle remains weak, management has expanded into automotive, sport-utility and off-highway programs to reduce volatility. In energy markets, geopolitical dynamics and infrastructure investment continue to drive demand for high-pressure pipeline components. This diversification mitigates cyclicality in any single sector and provides optionality as different industrial cycles recover at varying times.

Operational initiatives and balance sheet actions also support forward momentum. During 2025, the company completed a sale-leaseback transaction, generating a $2.5 million gain and approximately $2.9 million in net proceeds, improving liquidity and financial flexibility. Additionally, inventory reductions contributed to cash flow improvements during the first nine months of 2025.

Challenges Persist for SYPR’s Business

Sypris Solutions is facing cyclical and macroeconomic headwinds that are pressuring revenue and margins, particularly within Sypris Technologies. Net revenues declined 16% for the first nine months of 2025, primarily due to weakened demand in the North American Class 8 commercial vehicle market. Management also cites inflationary pressures on raw materials, logistics, labor and utilities, along with tariff uncertainty and supply chain constraints that are expected to persist through 2025.

The company is also contending with liquidity and leverage pressures. It incurred a net loss of $2.4 million and negative operating cash flow of $4.6 million for the first nine months of 2025. Additionally, supply chain delays and program timing issues within Sypris Electronics have increased working capital volatility and reduced operational efficiency.

Sypris’ Valuation

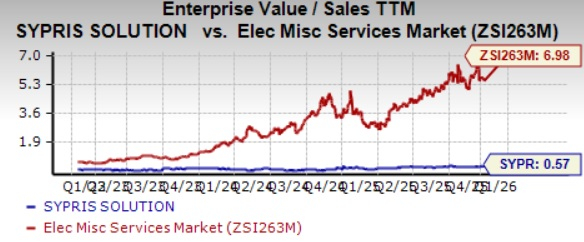

The company is cheaply priced compared with the industry average. Currently, SYPRSYPR-- is trading at 0.57X trailing 12-month EV/sales value, below the industry’s average of 6.98X. The metric remains higher than one of the company’s peers, Blink (0.52X), but remains lower than that of Legrand (4.93X).

Image Source: Zacks Investment Research

Conclusion

Despite ongoing cyclical weakness in the North American Class 8 truck market, inflationary cost pressures, tariff uncertainty, and recent liquidity constraints, Sypris Solutions is supported by strong aerospace and defense backlog visibility, including NASA Artemis-related awards extending into 2027, which underpin longer-term revenue stability and cash flow planning.

Strong fundamentals, coupled with SYPR’s undervaluation, present a lucrative opportunity for investors to add the stock to their portfolio.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Sypris Solutions, Inc. (SYPR): Free Stock Analysis Report

Blink Charging Co. (BLNK): Free Stock Analysis Report

LeGrand SA (LGRDY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet