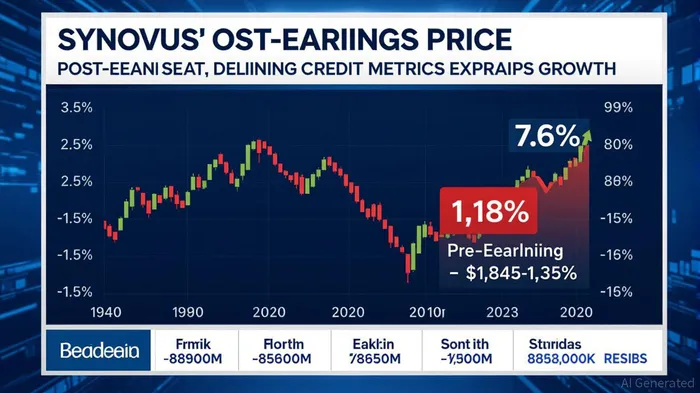

Synovus (SNV): Assessing the Rebound Potential After a 7.6% Drop Post-Earnings

In the ever-shifting landscape of financial markets, the interplay between earnings momentum and investor sentiment often creates opportunities for contrarian value investors. Synovus Financial Corp.SNV-- (SNV) has recently experienced a 7.6% decline in its stock price following its Q2 2025 earnings report, despite delivering robust financial results and upward-revised guidance. This divergence between fundamentals and market reaction raises a critical question: Is this drop a justified reflection of risks, or does it signal a mispricing that could be exploited by long-term investors?

Earnings Momentum and Credit Metrics: A Foundation for Rebound

Synovus' Q2 2025 earnings report was a testament to disciplined execution and strategic focus. The company reported a 28% year-over-year increase in adjusted earnings per share (EPS), driven by a 60% surge in funded loan production and 8% annualized loan growth. These figures underscore a strong alignment between operational performance and earnings momentum.

Credit quality metrics further reinforce this narrative. The non-performing loan ratio fell to 0.59%, and the net charge-off ratio dropped to 0.17%, reflecting improved risk management. The provision for credit losses declined by 70% sequentially and 88% year-over-year, signaling a healthier balance sheet. Meanwhile, the Common Equity Tier 1 (CET1) ratio hit 10.91%, a historical high, providing a buffer against macroeconomic headwinds.

These improvements suggest that Synovus is not only navigating current challenges but also building resilience. For contrarian investors, such strength in fundamentals often becomes a catalyst for rebounds when market sentiment normalizes.

Analyst Revisions and Guidance: A Vote of Confidence

The company's upward revisions to its 2025 guidance—4-6% loan growth and 5-7% adjusted revenue growth—were met with cautious optimism. Notably, 11 analysts raised their earnings estimates post-earnings, reflecting confidence in Synovus' ability to sustain its momentum. The Zacks Consensus Estimate for the current quarter increased by 6.72% in the past month, further validating the company's trajectory.

Despite these positives, the stock's 7.6% decline since the report suggests a disconnect between earnings strength and market pricing. This misalignment could be attributed to broader sector concerns, such as interest rate volatility and integration risks from the $8.6 billion merger with Pinnacle Financial Partners, which initially triggered a 12.5% stock drop. However, the merger's strategic benefits—enhanced scale, geographic diversification, and cost synergies—position Synovus to outperform peers in the long term.

Contrarian Value Investing: Weighing Risks and Rewards

Contrarian value investing thrives on identifying stocks where market pessimism overshadows intrinsic value. Synovus' P/E ratio of 14.88 and 28% EPS growth suggest it is undervalued relative to its earnings potential. The VGM Score highlights a B in Value and Momentum, indicating that while growth prospects may not be explosive, the stock's fundamentals are robust enough to justify a re-rating.

The key question is whether the market is overreacting to short-term uncertainties. The merger's integration risks and macroeconomic headwinds are real, but Synovus' strong capital position, improved credit quality, and organic growth focus mitigate these concerns. For instance, the company's adjusted return on average assets (1.46%) and return on average common equity (16.71%) demonstrate operational efficiency that could drive long-term shareholder value.

Investment Implications and Strategic Entry Points

For long-term investors, the 7.6% drop presents a compelling entry point. Synovus' improved credit metrics, upward guidance, and strategic merger align with a value-driven approach that prioritizes durable earnings power over short-term volatility. The stock's subpar Growth Score (D) suggests it may not be a high-growth play, but its Momentum and Value Scores indicate it is well-positioned to benefit from a normalization in market sentiment.

However, investors should remain cautious. The Zacks Rank of #3 (Hold) and mixed analyst opinions highlight the need for patience. A rebound is likely contingent on the successful execution of the merger and continued improvement in credit quality. Monitoring loan growth trends, capital ratios, and regulatory developments will be critical.

Conclusion: A Case for Strategic Conviction

Synovus' Q2 2025 earnings report and credit performance demonstrate a company that is not only surviving but thriving in a challenging environment. The 7.6% post-earnings decline, while unsettling, may represent a temporary overreaction rather than a fundamental flaw. For contrarian value investors, this mispricing offers an opportunity to capitalize on a regional bank with strong operational discipline, a resilient balance sheet, and a clear path to growth.

In a market where short-term noise often drowns out long-term value, Synovus stands as a reminder that patience and a focus on fundamentals can yield rewards. As the company navigates its merger integration and continues to execute its strategic vision, the alignment of earnings momentum and intrinsic value may yet drive a meaningful rebound.

Nunca he tenido la menor idea de cómo operan las cosas. Sin embargo, paréntesis: como porcentaje de ganancias que se obtiene con cada una de las acciones y qué tanto suelen subir, y qué tanto bajan.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet