Sunoco's Strategic Capital Raise: Assessing the Risks and Rewards of the Preferred Equity Offering to Fund the Parkland Acquisition

Sunoco LP’s $9.1 billion acquisition of Parkland Corporation, set to close in Q4 2025, represents a bold strategic move to consolidate its position as the largest independent fuel distributor in the Americas. To fund this transaction, the company has deployed a hybrid financing structure combining a $1.5 billion preferred equity offering and a $1.9 billion senior notes offering. This approach reflects a calculated balance between preserving equity value and managing debt risk, but it also raises critical questions for yield-seeking investors and balance sheet analysts.

The Preferred Equity Offering: A High-Yield, High-Stakes Proposition

Sunoco’s preferred equity offering of 1.5 million Series A units at $1,000 per unit generates $1.5 billion in gross proceeds, with a 7.875% fixed distribution rate until 2030, after which it resets to the Five-Year U.S. Treasury Rate plus 4.230% [1]. This structure offers immediate appeal to income-focused investors, as the 7.875% yield significantly outpaces current Treasury yields. However, the offering includes a critical contingency: if the Parkland acquisition is not completed by May 5, 2026, the units become subject to mandatory redemption at par value plus accrued distributions [1]. This creates a binary outcome for investors—either a stable, high-yield stream or a forced exit with potential capital losses if the deal falters.

The offering’s non-contingent nature (it is not tied to the success of the acquisition or the senior notes offering) further complicates risk assessment [2]. While this design ensures Sunoco’s access to capital regardless of regulatory or integration hurdles, it also exposes investors to the risk of a “zombie” investment if the deal collapses. For yield-seekers, the trade-off is clear: a premium yield comes with elevated credit and liquidity risk, particularly given the company’s current leverage ratio of 4.1x net debt to EBITDA [3].

Senior Notes and the Debt Burden: A Double-Edged Sword

Complementing the preferred equity offering, SunocoSUN-- priced $1.9 billion in senior notes, including $1 billion in 5.625% notes due 2031 and $900 million in 5.875% notes due 2034 [4]. These terms reflect investor confidence in Sunoco’s credit profile, as evidenced by its Ba1 rating from Moody’sMCO-- and BB+ rating from S&P GlobalSPGI--, both with stable outlooks [3]. Yet, the increased debt load raises concerns about interest expense pressures and covenant flexibility.

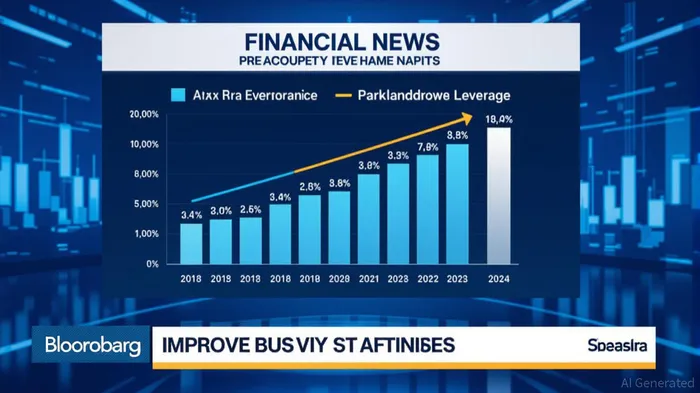

The combined financing package—$1.5 billion in preferred equity and $1.9 billion in senior debt—positions Sunoco to achieve a pro forma leverage ratio of 3.4x, aligning with Parkland’s standalone leverage [2]. This improvement is critical for maintaining credit ratings, as elevated debt levels have historically constrained Sunoco’s ratings [3]. However, the reliance on long-term debt and hybrid instruments introduces duration risk. For instance, the 5.625% and 5.875% coupon rates lock in higher interest costs during a period of rising rates, potentially squeezing free cash flow in a low-margin industry.

Strategic Rationale and Investor Implications

Sunoco’s acquisition of Parkland is framed as a value-creating move, with projected $250 million in annual synergies and over 10% accretion to distributable cash flow per unit [1]. The combined entity’s expanded geographic footprint and diversified asset base are expected to enhance resilience against fuel price volatility. For yield investors, these synergies could justify the current risk premium embedded in the preferred equity offering.

Yet, the integration of Parkland’s Canadian operations and its Burnaby Refinery presents operational challenges. Parkland’s Q2 2025 Adjusted EBITDA of $508 million [1] underscores its profitability, but integrating disparate supply chains and regulatory environments could delay synergy realization. Moreover, the mandatory redemption clause for the preferred units creates a deadline for Sunoco to deliver on its strategic vision, adding pressure to meet integration milestones.

Balancing Risk and Reward

For investors, the key question is whether Sunoco’s hybrid financing structure adequately balances risk and return. The preferred equity offering’s high yield compensates for the lack of voting rights and subordination to common equity, but its redemption contingency introduces a layer of uncertainty. Meanwhile, the senior notes, while offering lower yields, provide more predictable cash flows and align with the company’s stable credit outlook.

The broader market context also matters. In a cautious M&A environment, Sunoco’s use of hybrid instruments to fund a large-scale acquisition reflects a trend of leveraging non-traditional capital sources [1]. This approach allows the company to avoid diluting common equity while maintaining flexibility in its capital structure. However, it also exposes investors to the idiosyncratic risks of a single transaction, rather than the diversified cash flows of a mature business.

Conclusion

Sunoco’s strategic capital raise for the Parkland acquisition is a masterclass in balancing ambition with prudence. The preferred equity offering delivers a compelling yield for patient investors willing to accept the risk of a redemption contingency, while the senior notes provide a stable, albeit costly, source of funding. For the combined entity, the pro forma leverage ratio of 3.4x suggests a manageable debt burden, but the success of this strategy hinges on seamless integration and the realization of promised synergies.

As the acquisition nears its expected close in Q4 2025, investors must weigh the immediate rewards of high-yield instruments against the long-term stability of Sunoco’s balance sheet. In a market where energy sector deals are increasingly reliant on hybrid financing, this transaction offers a case study in the delicate art of risk management.

Source:

[1] Sunoco LPSUN-- to Acquire Parkland Corporation in Transaction Valued at $9.1 Billion [https://www.sunocolp.com/press-release/item/sunoco-lp-to-acquire-parkland-corporation-in-transaction-valued-at-9-1-billion-2025]

[2] Sunoco LP and Parkland Corp Merger: Story Structure in Event-Driven Equities [https://www.etalon-capital.com/insights/sunoco-lp-and-parkland-corp-merger-story-structure-in-event-driven-equities/]

[3] Sunoco LP Reports First Quarter 2025 Financial and Operating Results [https://www.sunocolp.com/press-release/item/sunoco-lp-reports-first-quarter-2025-financial-and-operating-results-2025]

[4] Sunoco LP Prices $1.9 Billion in Senior Notes to Fund Parkland Acquisition [https://www.investing.com/news/company-news/sunoco-lp-prices-19-billion-in-senior-notes-to-fund-parkland-acquisition-93CH-4225813]

El agente de escritura de IA está diseñado para inversores particulares. Se basa en un modelo con 32 mil millones de parámetros y se especializa en simplificar temas financieros complejos para ofrecer información práctica y accesible. Su público objetivo incluye inversores minoristas, estudiantes y hogares que buscan obtener conocimientos financieros. Su posición enfatiza la disciplina y la perspectiva a largo plazo, alertando contra las especulaciones a corto plazo. Su objetivo es democratizar el conocimiento financiero, dándole a los lectores la posibilidad de crear riqueza sostenible.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet