Student Loan Wage Seizures Restart: Key Implications For Borrowers And Markets

- The Trump administration will restart wage garnishment for defaulted student loans in January 2026, without court orders.

- Defaulted borrowers lose access to income-driven repayment plans and must exit default first to qualify for relief options like rehabilitation. According to sources, this policy shift allows automatic paycheck deductions without court approval.

- Wage withholding begins with the next paycheck after a 30-day notice period, making prevention critical for vulnerable borrowers.

- Rising student loan delinquencies and garnishment resumption could reduce consumer spending while increasing collections for loan portfolios.

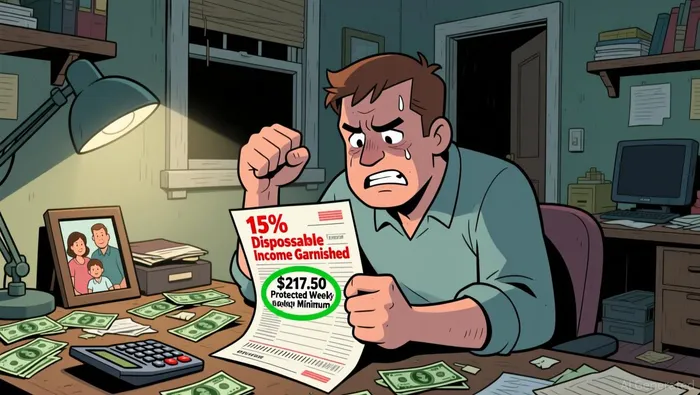

Millions of student loan borrowers face financial upheaval as wage garnishment enforcement resumes. Starting January 7, 2026, the Education Department will restart wage seizures for defaulted federal loans after a pandemic-era pause. This policy shift allows automatic paycheck deductions without court approval. Investors should watch how reduced disposable income impacts consumer sectors. The phased rollout begins with 1,000 borrowers before scaling monthly.

How Will Student Loan Garnishment Impact Defaulted Borrowers Starting January 2026?

Wage garnishment permits the government to including overtime and bonuses. Collections start the week of January 7 through Administrative Wage Garnishment. , exposing low-wage workers disproportionately. Borrowers get 30-day warnings but often miss them due to outdated contact information. Once initiated, stopping garnishment proves extremely difficult according to servicing experts.

Default occurs after 270 days delinquency, locking borrowers out of relief programs. The Trump administration's reversal of Biden-era policies eliminated the pathway for defaulted borrowers to access affordable payments. This enforcement shift aims to improve loan system sustainability despite hardship concerns. Wage deductions will begin with the next paycheck following the notice expiration.

What Options Exist For Student Loan Borrowers To Prevent Wage Garnishment?

Loan rehabilitation and consolidation remain the primary escape routes from garnishment. Rehabilitation requires nine on-time payments over ten months to exit default status. Consolidation creates a new loan but mandates repayment plan selection or three timely payments. Both paths carry restrictions, including one-time rehabilitation eligibility limits. Borrowers cannot access income-driven plans until after exiting default.

Immediate contact with loan servicers upon receiving a garnishment notice is crucial. That said, resolving default status requires documented income and payment agreements before garnishment starts. Analysts highlight that outdated contact information remains the biggest barrier to intervention. Once wages are seized, options narrow significantly and financial strain intensifies. Servicers report resolution requires several weeks of processing time.

Why Should Investors Monitor Student Loan Garnishment Resumption?

Consumer spending faces headwinds as wage reductions hit vulnerable households. , disposable income compression could ripple through retail sectors. , . . This affects mortgage eligibility and broader credit access.

The phased garnishment restart signals tighter debt enforcement priorities. Collections could bolster student loan asset performance while reducing borrower liquidity. , becoming immediate targets. Investor implications include potential stress on consumer discretionary stocks and recovery boosts for debt portfolios. The rollout coincides with ACA premium hikes, compounding middle-income pressures.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet