Student Loan Policy Shifts: Navigating Credit Risk and Market Volatility in a New Era of Borrowing

The U.S. student loan landscape is undergoing a seismic shift, driven by the Trump administration's “Big, Beautiful Bill” enacted in July 2025. This sweeping overhaul, which imposes strict borrowing limits, eliminates key repayment protections, and redirects borrowers toward private loans, is reshaping credit risk profiles and market volatility across the financial ecosystem. For investors, understanding these dynamics is critical to navigating the evolving risks and opportunities in student loan-backed securities (ABS) and related markets.

The Borrower's Dilemma: Tightened Limits and Heightened Default Risks

The new policy caps federal borrowing at $20,500 annually for graduate students ($100,000 lifetime) and $50,000 for professional degrees ($200,000 lifetime). Parent PLUS loans are restricted to $20,000 per year and $65,000 lifetime. These limits have forced many borrowers into private loans, which now account for 8.63% of originations in the 2024–2025 academic year—a 8.63% year-over-year increase.

Private loans, however, come with higher interest rates (averaging 8–12% versus federal averages of 3.5–6.5%) and fewer borrower protections. With 23.7% of borrowers now delinquent in Q1 2025 (per the New York Fed), the risk of default is rising. The average federal loan balance of $38,375, combined with reduced access to income-driven repayment (IDR) plans, has created a perfect storm for borrowers. Default rates for federal loans stand at 4.86%, while private loans report 1.61%, but the latter's higher interest rates amplify their systemic risk.

Lenders: A Shift to Private Loans and Credit Risk Exposure

Private lenders are seeing a surge in demand, but this growth comes with caveats. Unlike federal loans, private lending relies heavily on credit scores, excluding many low-income borrowers. This has led to a 2.2 million borrower population with credit score drops exceeding 100 points, limiting their access to new credit. For lenders, the risk of non-performing loans is rising, particularly as borrowers face wage garnishments and tax offsets under the resumption of collections in May 2025.

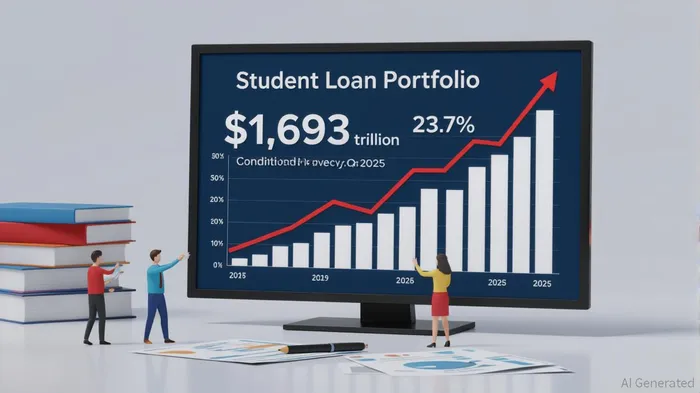

Asset-Backed Securities: A Double-Edged Sword

Student loan ABS, particularly those backed by private debt, are experiencing heightened scrutiny. Morningstar DBRS notes that the delinquency surge has led to lower credit ratings for private loan-backed ABS, as their risk profiles diverge from the historically stable federal loan portfolios. Federal student loans, now the largest consumer debt category after mortgages, remain a cornerstone of the ABS market, but the shift to private loans introduces fragility.

The $1.693 trillion federal loan portfolio is expected to shrink as borrowing limits curb access, while private ABS volumes grow. However, the higher interest rates and delinquency risks in private loans could lead to tighter spreads and reduced liquidity. Investors must weigh the potential for higher yields against the elevated default risk, particularly in regions with high delinquency rates (e.g., Southern states like Mississippi and Alabama, where delinquency rates exceed 30%).

Investment Implications and Strategic Recommendations

- Diversification is Key: Investors should avoid overexposure to private student loan ABS. Instead, consider a mix of federal-backed and private-backed securities, hedging against regional and demographic risks.

- Monitor Policy Developments: The Biden administration's ongoing legal battles over IDR programs and the Trump administration's enforcement of collection practices will shape the market. Track legislative updates and regulatory actions.

- Focus on Prime Borrowers: Given the rise in near-prime and subprime delinquencies, prioritize ABS backed by prime borrowers (credit scores ≥720), who are better positioned to navigate repayment challenges.

- Leverage Derivatives for Hedging: Use credit default swaps (CDS) to mitigate potential losses in private loan portfolios. The market's growing volatility makes hedging an attractive strategy.

Conclusion

The post-2025 student loan policy shifts have created a complex interplay of credit risk, market volatility, and borrower behavior. While federal loan portfolios remain relatively stable, the growing reliance on private loans introduces new challenges for investors. By adopting a cautious, diversified approach and staying attuned to regulatory and economic trends, investors can navigate this evolving landscape while mitigating downside risks. The key lies in balancing yield-seeking with risk-aware strategies in a market where policy changes can reverberate far beyond the classroom.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet