Student Loan Policy Shifts: Macroeconomic and Investment Implications for Financial Services and Consumer Sectors

Policy Shifts and Macroeconomic Consequences

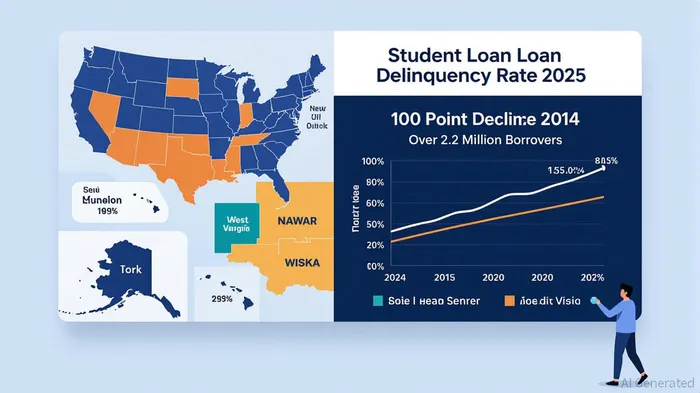

The OBBBA replaced the Biden-era SAVE Plan with a new (RAP), which imposes higher monthly payments and longer repayment terms, particularly for low-income borrowers. By July 2026, the RAP will require payments based on gross income, eliminating the income protection previously offered under income-based repayment plans. This has already triggered a surge in delinquencies: , , with Southern states like Mississippi and West Virginia reporting the highest rates. The resumption of interest accrual for loans in the , mandated by a federal court injunction, further exacerbated financial strain, .

These developments reflect a broader trend of financial instability. , the collateral damage to credit scores has far-reaching consequences. Higher borrowing costs for mortgages, auto loans, and credit cards are now inevitable, as lenders recalibrate risk assessments in response to deteriorating credit profiles. The of 2025, which phases out subsidized graduate loans and tightens federal borrowing caps, compounds these pressures, redirecting demand toward private lenders.

Investment Implications: Education Lenders, Fintech, and Regional Banks

The policy shifts have created a bifurcated market. Education lenders stand to benefit from increased demand for private loans, particularly as federal programs become less accessible. However, this growth is not without risk. Private lenders face a borrower base with weakened credit profiles, raising concerns about default rates. For instance, over 2.4 million borrowers now have credit scores below 620, a threshold that often disqualifies them from favorable loan terms.

Fintech companies, by contrast, are capitalizing on the void left by traditional banks. Innovations in alternative credit scoring and AI-driven underwriting have enabled fintechs to offer faster approvals and more flexible terms to borrowers with thin credit files. The sector's resilience is evident in its fundraising success, as investors prioritized sustainable revenue models over speculative growth. However, fintechs remain vulnerable to regulatory scrutiny and interest rate volatility, which could dampen their margins.

Regional banks face a dual challenge. The OBBBA's tax incentives for rural and agricultural real estate loans may provide a temporary boost, but the broader shift toward private student lending threatens their market share. Regional banks, which historically dominated student loan origination, now compete with national lenders and fintechs that offer more agile digital platforms. Additionally, the reinstatement of EBITDA for interest expense calculations under the OBBBA could improve loan activity for some borrowers, but it also heightens credit risk for institutions with weaker capital positions.

Reassessing Exposure: A Call for Strategic Reallocation

For investors, the key lies in balancing growth opportunities with risk mitigation. Education lenders with robust underwriting standards and diversified portfolios may outperform, but their exposure to high-risk borrowers necessitates careful due diligence. Fintechs offering AI-driven credit solutions and alternative data models present compelling long-term prospects, particularly as the sector matures beyond speculative valuations. However, their reliance on regulatory tailwinds and interest rate stability introduces volatility.

Regional banks, meanwhile, must navigate a landscape where traditional lending models are increasingly obsolete. Those that leverage the OBBBA's tax incentives for rural real estate or partner with fintechs to enhance digital capabilities may retain competitive advantages. Conversely, institutions with concentrated student loan portfolios and weak capital buffers face heightened vulnerability.

Conclusion

The 2024-2025 student loan policy shifts have catalyzed a reordering of the financial services sector, with macroeconomic ripple effects extending far beyond education financing. While easing debt burdens could theoretically stimulate consumer spending, the current trajectory-marked by stricter repayment terms and rising delinquencies-suggests a more complex reality. For investors, the path forward requires a recalibration of risk-return profiles, with a focus on sectors and firms best positioned to navigate the evolving credit landscape.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet