StubHub’s IPO: hot ticket—or pricey reissue?

IPO activity has been lively this year, but a few crowd-pleasers (FIG, KLAR, WYFI, CRCL) have already handed back early gains. Into that backdrop steps StubHub—North America’s best-known secondary ticket marketplace—seeking a valuation near $9–$9.2 billion. It’s a brand with real network effects and cash generation, but it’s also listing into a tougher resell environment, tighter fee rules, and persistent Ticketmaster/Live Nation gravity. Is STUBSTUB-- different? On franchise quality, yes. On cycle and risk, investors should keep a hand on the rail.

The deal itself is straightforward. StubHubSTUB-- will sell about 34 million shares (roughly 10% of the float) at $22–$25 on the NYSE under STUB, raising ~$800–$851 million. J.P. Morgan and Goldman Sachs lead the book, with BofA, EvercoreEVR--, BMO, MizuhoMFG--, TD Cowen, TruistTFC--, and Wolfe in the syndicate. Indications point to a heavily oversubscribed book—reportedly 20x with limited price sensitivity—which argues for a firm print on day one. That said, 2025 has reminded us that hot opens don’t guarantee durable after-market performance; the real test is whether fundamentals support months, not minutes, of momentum.

StubHub’s model is a classic two-sided marketplace: it matches ticket sellers (from individuals to professional brokers and rights holders) with fans, takes a transaction fee (management cites an average near 20% on ~$200 tickets), and generally avoids inventory risk. Three self-reinforcing flywheels drive scale. First, the growth flywheel: more buyers produce more engagement data, improving targeting and conversion, which attracts more buyers. Second, the liquidity flywheel: more transactions attract more sellers and selection, which attracts—again—more buyers. Third, the data flywheel: first-party pricing and behavior data sharpen merchandising and product experience, which feeds back into both growth and liquidity. The international viagogo brand adds reach (≈15% of revenue), and a nascent direct issuance (primary) push—now >$100M GMS—targets the much larger original-ticket market and unsold inventory.

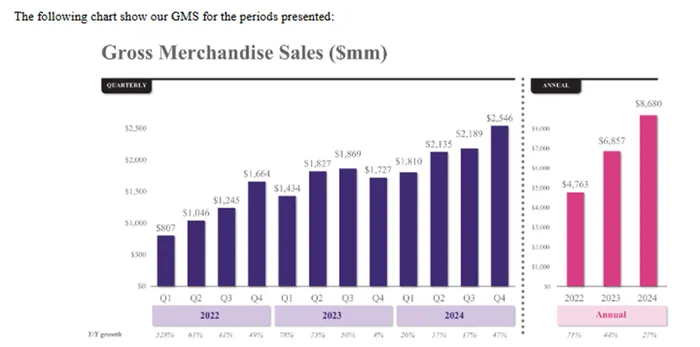

Financially, 2024 showed strong top-line growth with mixed operating trends. Gross merchandise sales rose to $8.68B from $6.86B (+27%), revenue climbed to $1.77B (+29.5%), and free cash flow remained healthy at $255M (down from $302M in 2023)—all consistent with a capital-light, cash-generative marketplace. But adjusted EBITDA slipped to $298.7M from $353.9M as sales and marketing rose nearly 60% and the company invested in new initiatives, including direct issuance. Reported net swung to a small $2.8M loss (versus 2023 profits buoyed by unusual tax items), and general and administrative costs stepped up on litigation reserves, loan-extension costs, and indirect taxes. Worth noting: management discloses contingent indirect-tax exposures and a probable ~$49M sales-tax litigation accrual—manageable, but part of the valuation debate.

The operating backdrop is tougher than the post-pandemic sugar high. The FTC’s all-in pricing rules compress the ability to recover economics at checkout. Artists and rights holders are leaning into anti-scalping measures or pricing closer to “fair value,” which narrows arbitrage opportunities. Competition is relentless: Ticketmaster dominates primary distribution and can influence secondary flows, while smaller peers (e.g., Vivid Seats) have called out a challenging industry setup. None of this invalidates StubHub’s moat—liquidity, trust, and data at scale still matter—but it raises the bar: take rates must hold, marketing needs to normalize, and investments have to translate into profitable growth.

Is STUB “different” from this year’s faders? It has advantages many IPOs lack: a widely recognized consumer brand, deep marketplace liquidity, and meaningful free cash flow. It’s also pushing into primary distribution, which expands the addressable market and could smooth cyclicality over time. The flip side is valuation. At $22–$25, the range implies ~$8.6–$9.2B equity value; on 2024 adj. EBITDA of ~$299M, investors are effectively paying a premium multiple that assumes StubHub can defend take rates, re-accelerate EBITDA, and scale direct issuance without permanently diluting margins. That’s achievable—but not free.

Two questions will decide the after-market: do unit economics (especially marketing efficiency and seller incentives) improve post-IPO, and does direct issuance add high-quality growth without crimping profitability? Positive answers there, and the premium can be earned. If not, the stock risks joining 2025’s class of strong debuts that faded once the confetti settled.

In short, StubHub is a high-quality marketplace coming public at a full price during a more demanding phase for resellers. Oversubscription and brand equity argue for a good first act; durability will hinge on take-rate stability, expense discipline, and proof that primary distribution is additive, not dilutive. Enjoy the show—just check the fees before you click “Buy.”

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet