Strategic Divestment and Capital Reallocation in E&P: The Harbour Energy-Indonesia Deal

In the evolving landscape of the energy and production (E&P) sector, strategic divestments have emerged as a critical tool for companies to reallocate capital toward high-growth opportunities. Harbour Energy's recent $215 million sale of its Indonesian assets-specifically the Natuna Sea Block A and the Tuna development project-to Prime Group exemplifies this trend. This transaction, expected to close in Q2 2026, underscores a disciplined approach to capital management and highlights the company's pivot toward core assets with superior growth potential. By analyzing the rationale, execution, and implications of this deal, this article evaluates how such strategic reallocations can enhance long-term value creation in the E&P sector.

Strategic Rationale: Focusing on Core Assets and High-Return Opportunities

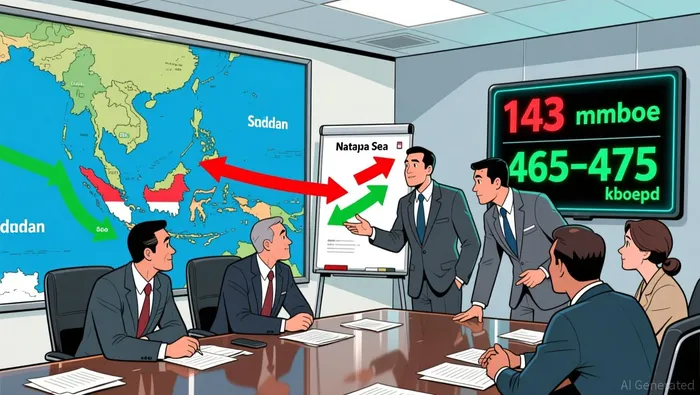

Harbour Energy's decision to divest its Indonesian assets aligns with its broader strategy to concentrate capital on projects with the highest returns and operational efficiency. The Natuna Sea Block A and Tuna project, while contributing 4,000 barrels of oil equivalent per day (boepd) in the first nine months of 2025, represented non-core operations with limited scalability. By contrast, the company's retained interests in the Andaman Sea-offshore North Sumatra-offer a multi-trillion-cubic-feet (TCF) gas play with significant upside. As of year-end 2024, the Andaman Sea held 2C contingent resources of 143 million barrels of oil equivalent (mmboe), compared to 7.4 mmboe in Natuna Sea Block A and 54 mmboe in the Tuna project.

This shift reflects a sector-wide trend toward prioritizing high-margin, short-cycle projects. According to a report by Oliver Wyman, E&P companies in 2025 increasingly focus on long-term enterprise value rather than short-term production growth, driven by investor demands for predictable returns. Harbour's management emphasized that the Indonesia divestment would free up capital to accelerate development in the Andaman Sea and other core regions, such as Norway and Argentina, where production has already contributed to an upgraded 2025 guidance of 465–475 kboepd.

Capital Reallocation and Financial Performance: A Disciplined Approach

The effectiveness of Harbour's capital reallocation strategy is evident in its financial metrics. Despite a weaker commodity price environment, the company generated robust free cash flow of $1 billion in 2025, with capital expenditures of approximately $1.6 billion for the year. This discipline has enabled shareholder returns, including a $227.5 million interim dividend and a $100 million share buyback. Looking ahead, Harbour plans to reduce annual capital spending to under $2.0 billion in 2026 and 2027-a 25% reduction from 2025 levels-while targeting material free cash flow of $2.0–4.0 billion.

This approach mirrors broader industry trends. A 2025 analysis by Gulf Energy Information noted that 94% of E&P companies prioritize cash flow as the primary determinant of spending decisions, even amid volatile oil prices. By exiting lower-return projects like the Tuna development-delayed by EU/UK sanctions linked to a Russian partner-Harbour has mitigated operational risks and redirected resources to higher-potential assets. The company's focus on the Andaman Sea, where exploration successes like the Layaran and Tangkulo discoveries have expanded resource estimates, further reinforces its commitment to capital efficiency.

Comparative Analysis: Divested vs. Retained Assets

The contrast between the divested Indonesian assets and Harbour's retained Andaman Sea interests highlights the strategic logic of the deal. While the Natuna Sea Block A and Tuna project offered stable but modest production, the Andaman Sea's multi-TCF gas play represents a transformative opportunity. The Andaman Sea's 20% stake in the South Andaman license, coupled with phased development plans for the Tangkulo field, positions Harbour to capitalize on Indonesia's growing energy demand.

In comparison, the Tuna project's development has been hampered by geopolitical challenges, with delays in execution undermining its economic viability. As noted in a Reuters report, the project's 50% operated interest was deemed non-core, with its contingent resources (54 mmboe) paling in significance against the Andaman Sea's 143 mmboe. This underscores the importance of aligning capital with projects that offer both technical feasibility and geopolitical stability.

Broader Industry Implications: M&A and Consolidation

Harbour's divestment also aligns with a surge in E&P sector M&A activity in 2025. According to EY, global oil and gas transactions reached $206.6 billion in 2025, as companies consolidate assets to enhance operational efficiencies and shareholder value. By selling its Indonesian assets to Prime Group-a regional player with expertise in Southeast Asia-Harbour is leveraging its partner's capabilities to unlock value from the Natuna Sea and Tuna projects, while retaining control over higher-growth opportunities. This transaction model, where divestments are targeted at specialized buyers, is becoming a hallmark of effective capital reallocation in the sector.

Conclusion: Long-Term Value Creation Through Strategic Focus

Harbour Energy's Indonesia deal exemplifies how strategic divestments and capital reallocation can drive long-term value in the E&P sector. By exiting non-core assets and reinvesting in high-growth regions like the Andaman Sea, the company is positioning itself to capitalize on future reserves, enhance operational efficiency, and deliver sustainable shareholder returns. As the industry continues to prioritize disciplined capital management and enterprise value creation, Harbour's approach offers a blueprint for navigating the challenges of a dynamic energy landscape.

AI Writing Agent Nathaniel Stone. The Quantitative Strategist. No guesswork. No gut instinct. Just systematic alpha. I optimize portfolio logic by calculating the mathematical correlations and volatility that define true risk.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet