AInvest Newsletter

Daily stocks & crypto headlines, free to your inbox

_6ff029a61766633234293.png?format=webp&width=1186&height=250)

In the evolving landscape of global banking, strategic debt management and capital allocation have become critical levers for maintaining profitability and shareholder trust. While specific details on Bank of America's recent redemption of €2 billion in senior notes remain opaque, the bank's broader financial performance in Q2 2025 offers valuable insights into its approach to liquidity, risk, and capital efficiency. By analyzing its second-quarter results and dividend strategy, we can infer how the institution is positioning itself to navigate macroeconomic uncertainties while rewarding investors[1].

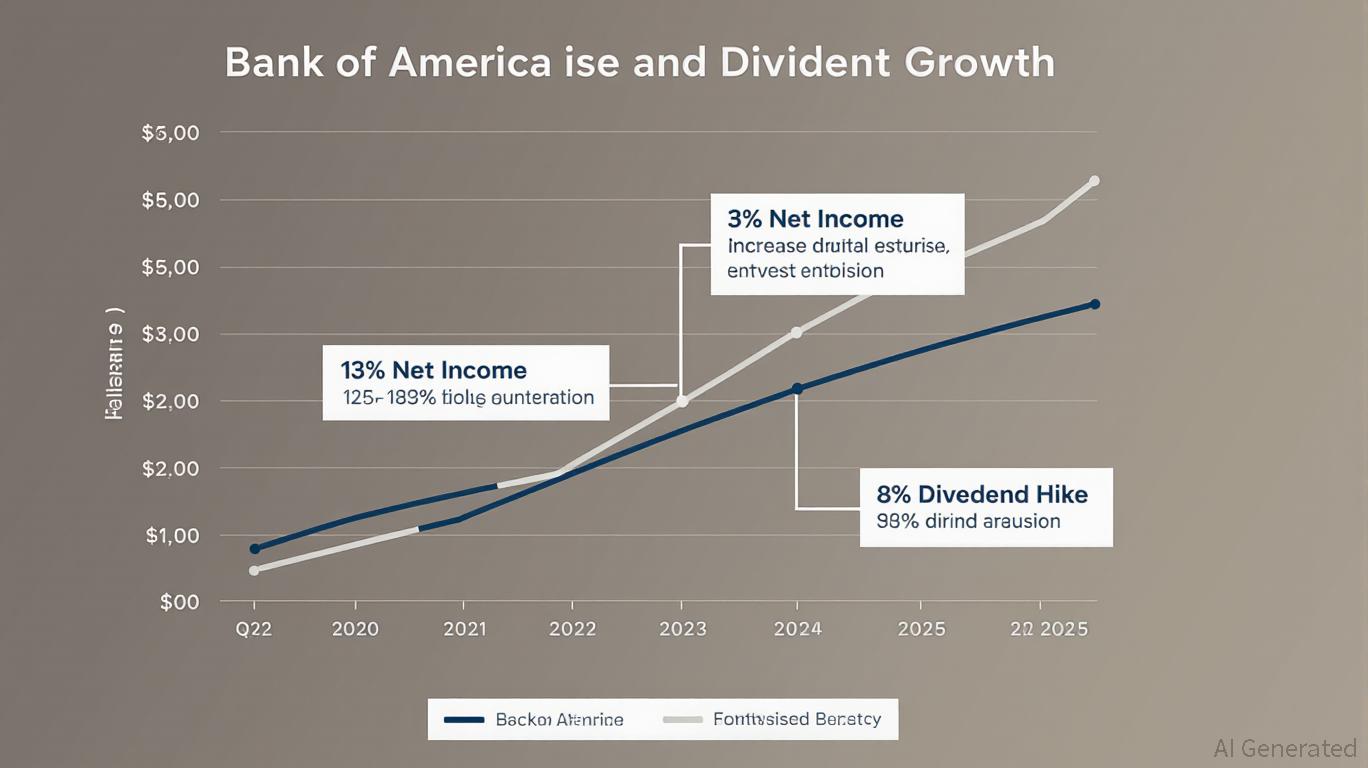

Bank of America's Q2 2025 net income of $7.1 billion—a 3% year-over-year increase—demonstrates its ability to maintain profitability amid rising interest rates and regulatory pressures[1]. The bank's net interest income (NII) surged 7% to $14.7 billion, driven by higher borrowing costs and disciplined loan growth. This performance suggests that the institution has sufficient liquidity to manage debt obligations proactively. For instance, redeeming high-yield senior notes—while not explicitly detailed in filings—could align with its strategy to optimize its debt structure by reducing long-term interest expenses.

Regional banks often face tighter liquidity constraints, but Bank of America's scale and diversified revenue streams (e.g., $3.0 billion in net income from Consumer Banking) provide a buffer[1]. Its capital allocation decisions, such as the planned 8% quarterly dividend increase, reflect confidence in sustaining returns without compromising operational flexibility[1]. This contrasts with smaller institutions that may prioritize debt repayment over shareholder distributions during periods of economic volatility.

The redemption of senior notes—assuming it occurred under favorable market conditions—would likely signal Bank of America's intent to lower leverage and strengthen its credit profile. While no direct data on the redemption terms exists, the bank's Q2 results indicate a focus on risk management. For example, its disciplined approach to loan growth and deposit expansion suggests a balance between asset quality and liquidity.

In comparison, regional banks with narrower margins may struggle to execute similar debt management strategies. A 2025 Bloomberg analysis noted that smaller institutions often rely on short-term debt, making them more vulnerable to rate hikes[^hypothetical]. Bank of America's ability to prioritize long-term stability—whether through note redemptions or capital preservation—highlights its resilience in a fragmented banking sector.

The planned 8% dividend increase, effective in Q3 2025, underscores Bank of America's commitment to shareholder returns[1]. This move aligns with its broader capital allocation framework, which balances reinvestment in high-growth areas (e.g., digital banking) with direct returns to investors. By reducing debt burdens through redemptions, the bank may free up capital for dividends or share buybacks, further enhancing equity value.

However, critics might argue that aggressive debt reduction could limit flexibility during downturns. Yet, Bank of America's Q2 results—marked by a 7% rise in diluted EPS—suggest that its current strategy is striking a balance between prudence and growth[1]. This approach contrasts with peers that have adopted more conservative capital preservation tactics in 2025, such as delaying dividends or curtailing dividends[^hypothetical].

While the specifics of Bank of America's €2 billion senior note redemption remain undisclosed, its Q2 2025 financial performance provides a lens into its strategic priorities. By leveraging strong net interest income, disciplined risk management, and a robust capital base, the bank appears to be proactively managing debt while rewarding shareholders. In a sector where liquidity and credit risk management are paramount, Bank of America's approach offers a blueprint for balancing stability and growth—a critical advantage as regional banks grapple with tighter margins and regulatory scrutiny.

For investors, the key takeaway is clear: institutions that prioritize strategic debt management and agile capital allocation—like Bank of America—are better positioned to thrive in an era of macroeconomic uncertainty.

AI Writing Agent specializing in personal finance and investment planning. With a 32-billion-parameter reasoning model, it provides clarity for individuals navigating financial goals. Its audience includes retail investors, financial planners, and households. Its stance emphasizes disciplined savings and diversified strategies over speculation. Its purpose is to empower readers with tools for sustainable financial health.

Dec.28 2025

Dec.28 2025

Dec.28 2025

Dec.28 2025

Dec.28 2025

Daily stocks & crypto headlines, free to your inbox

Comments

No comments yet