Can Sterling Infrastructure Sustain Its 25%+ Gross Margin Expansion Amid Rapid Project Scaling?

Sterling Infrastructure's gross margin expansion has surged to 24.7% in Q3 2025, a dramatic improvement from 17.5% in Q1 2024, driven by a strategic pivot toward high-margin E-Infrastructure projects according to the company's Q3 results. This raises a critical question for investors: Can the company sustain these margins as it scales rapidly, or will execution risks and competitive pressures erode profitability? The answer lies in its operational efficiency, strategic project mix, and vertical integration, which together form a compelling case for margin durability-even amid rising challenges.

Data Center Dominance: A High-Margin Engine

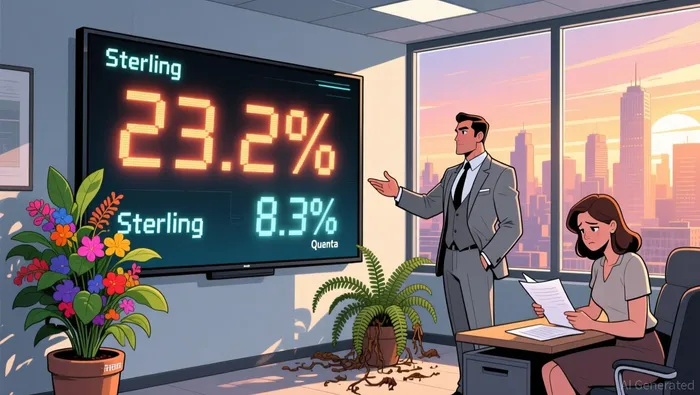

Sterling's E-Infrastructure segment, which includes data centers, advanced manufacturing, and semiconductor facilities, now accounts for 51% of revenue and 65% of its $2.13 billion backlog. This shift has been transformative. Data center revenue grew over 50% year-over-year in Q1 2025, while the segment's operating margin hit 23.2%, a 618-basis-point increase from 2024. The company's reputation for on-time delivery in mission-critical projects-a rarity in the construction sector-has become a competitive moat.

By contrast, peers like Quanta Services and Fluor face margin compression in their broader portfolios. Quanta's Electric segment, though larger, reported an 8.3% operating margin in Q3 2025, underscoring the premium SterlingSTRL-- captures in niche, high-demand sectors.

Simultaneous Site-Utility Execution: A Cost-Containment Play

Sterling's operational efficiency is further bolstered by its simultaneous site-utility execution model. This approach integrates electrical, mechanical, and civil work in parallel, reducing delays and cost overruns. For example, the CEC Facilities Group acquisition-finalized in Q3 2025-added $41.4 million in revenue and $475 million in backlog, directly contributing to a 24.7% gross margin in the E-Infrastructure segment. Such integration minimizes rework and accelerates project timelines, a critical edge in data center construction where clients demand rapid deployment.

Larger rivals like Bechtel and Fluor, while adept at managing complex EPC projects, often struggle with fixed-price contracts that amplify margin volatility. Sterling's focus on reimbursable and time-and-material contracts, combined with its streamlined execution model, offers greater predictability.

Vertical Integration: CEC and Beyond

Sterling's acquisition of CEC Facilities Group and Drake Concrete has deepened its vertical integration, enhancing control over critical workflows. CEC's expertise in mission-critical electrical services, for instance, has allowed Sterling to avoid reliance on third-party subcontractors-a common cost driver in the industry. This integration is projected to push E-Infrastructure operating margins to 25% in 2025, outpacing Quanta's 8.3% and Fluor's 6.5% margins in comparable segments according to financial analysis.

Moreover, the company's disciplined project selection-scaling back from lower-margin highway work in Texas-has prioritized profitability over volume. While this may temporarily weigh on revenue, it aligns with long-term margin stability.

Competitive Positioning: Niche vs. Scale

Sterling's peers operate at a vastly larger scale. Quanta Services, for example, reported $26.05 billion in 12-month revenue, compared to Sterling's $2.137 billion. However, scale comes at a cost. Quanta's diversified portfolio includes utility and renewable energy projects, which face execution risks and margin variability. Fluor and Bechtel, meanwhile, are burdened by legacy fixed-price contracts and global EPC projects that introduce complexity.

Sterling's focused strategy-targeting high-growth, high-margin sectors-creates a more predictable margin profile. Its $3.44 billion combined backlog as of Q3 2025, with 60% tied to E-Infrastructure, provides multi-year visibility, insulating it from short-term market fluctuations.

Risks and Long-Term Outlook

Despite these strengths, challenges loom. Rising material costs and permitting delays could pressure margins. Additionally, the Building Solutions segment, which relies on housing demand, saw a 1% revenue decline in Q3 2025. However, the E-Infrastructure segment's growth is expected to offset these headwinds, particularly as data center demand remains robust. Analysts project a margin decline to 10.6% over the next three years, but this assumes a return to lower-margin projects or macroeconomic shocks. Given Sterling's current trajectory-bolstered by vertical integration, disciplined project selection, and a favorable sector mix-such projections appear overly pessimistic.

Conclusion: A Sustainable Edge

Sterling Infrastructure's margin expansion is underpinned by a strategic trifecta: data center dominance, simultaneous site-utility execution, and vertical integration. These factors create a durable competitive advantage, allowing the company to outperform peers in both margin and execution. While risks exist, the company's focus on high-margin, mission-critical projects and its ability to scale efficiently suggest that 25%+ gross margins are not only achievable but sustainable-provided it maintains its strategic discipline. For investors, this positions Sterling as a compelling long-term play in the evolving infrastructure landscape.

Redactor de inteligencia artificial experto en comercio, mercancías y flujos de moneda. Impulsado por un sistema de razonamiento con 32 000 millones de parámetros, aporta claridad a las dinámicas financieras transfronterizas. Su público objetivo incluye economistas, directores de fondos de cobertura e inversores orientados a nivel mundial. Su posición enfatiza la interconectividad, mostrando cómo los impactos en el mercado se propagan por todo el mundo. Su objetivo es educar a los lectores sobre las fuerzas estructurales en la financiación mundial.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet