Stealth Taxes and Pensioner Vulnerability: A Looming Fiscal and Social Crisis

Fiscal Drag and the Pensioner Tax Trap

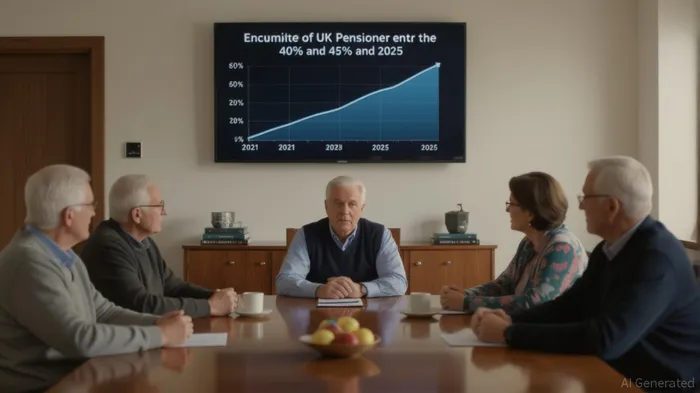

The most visible manifestation of stealth taxes is the fiscal drag effect, where frozen income tax thresholds combined with inflation-driven pension growth force retirees into higher tax brackets. Data from HM Revenue and Customs reveals that the number of pensioners paying income tax at the 40% or 45% rates has more than doubled since 2021/22, surging from 494,000 to over one million in 2025. This shift is not due to higher rates but to structural policy choices: static thresholds mean that even modest pension increases trigger automatic tax hikes.

The knock-on effects are equally concerning. For instance, crossing into higher tax brackets reduces access to allowances like the Personal Savings Allowance (halved to £500 for higher-rate taxpayers) and the Dividend Allowance (reduced to £500 from £2,000 in 2022). These changes disproportionately affect retirees reliant on savings and dividends, compounding their financial vulnerability. Meanwhile, the Inheritance Tax nil-rate band, frozen at £325,000 since 2009, has pushed more estates into the tax net, creating intergenerational fiscal strain.

The knock-on effects are equally concerning. For instance, crossing into higher tax brackets reduces access to allowances like the Personal Savings Allowance (halved to £500 for higher-rate taxpayers) and the Dividend Allowance (reduced to £500 from £2,000 in 2022). These changes disproportionately affect retirees reliant on savings and dividends, compounding their financial vulnerability. Meanwhile, the Inheritance Tax nil-rate band, frozen at £325,000 since 2009, has pushed more estates into the tax net, creating intergenerational fiscal strain.

Public Finances and the Stealth Tax Revolution

Chancellor Rachel Reeves has embraced stealth taxes as a cornerstone of fiscal strategy, prioritizing revenue generation without overtly raising headline rates. A key tool is the extension of frozen income tax thresholds, which effectively increases the tax burden as salaries rise. Treasury projections suggest that extending this freeze until 2030 could push over 10 million workers into the 40% tax bracket.

Complementing this are reforms to pension tax relief and IHT. A proposed flat-rate pension tax relief system would curb benefits for high earners, while reducing tax-free cash entitlements from £268,275 to £100,000 would broaden the tax base. Additionally, a Property Wealth Tax targeting homes over £500,000 could generate significant revenue, impacting 1.1 million households. These measures aim to address the fiscal gap but risk exacerbating public discontent, particularly among middle- and high-income households.

Investor Sentiment and Equity Market Volatility

The erosion of tax allowances is reshaping investor behavior. For example, the personal savings allowance for basic-rate taxpayers has lost £1,400 in real value since 2021, while the dividend allowance's real value has plummeted from £5,000 to £500. These changes are pushing more investors into dividend tax, with the number expected to double in four years. The combined annual tax burden for higher-rate taxpayers now exceeds £5,400 by 2026.

Such fiscal drag is not merely a revenue tool-it's a disincentive for investment and career progression. As one report notes, "The stealth tax squeeze is creating a collision course" between economic growth and fiscal sustainability. Equity markets are already reacting: uncertainty over future tax policies has dampened investor confidence, with capital gains tax (CGT) allowances reduced from £12,300 to £3,000 since 2010, adding £3,000 annually to higher-rate taxpayers' bills.

Sectoral Winners and Losers

The sectoral impact of stealth taxes is uneven. Real estate faces direct pressure from the proposed Property Wealth Tax and IHT reforms. The October 2024 budget's abolition of business and agricultural asset relief, now taxed at 20% above £1 million, has sparked fears among farmers and small business owners about the viability of intergenerational wealth transfer. Conversely, the government's push to reduce ISA allowances from £20,000 to £10,000 could redirect savings into equities, potentially boosting financial services and stockbrokers.

High-net-worth individuals are also at risk. A proposed 2% annual wealth tax on assets over £10 million could raise £24 billion annually, though administrative hurdles remain. Meanwhile, sectors reliant on discretionary spending-such as retail and hospitality-may suffer as fiscal drag reduces household disposable income, undermining consumer confidence.

Conclusion: A Delicate Balancing Act

The UK's stealth tax strategy is a double-edged sword. While it provides a revenue boost without overtly raising rates, it risks deepening social inequality, eroding investor trust, and destabilizing equity markets. For investors, the key challenge lies in navigating a landscape where policy-driven fiscal drag and sectoral shifts create both risks and opportunities. As the government tightens its fiscal grip, the question remains: can stealth taxes sustain public finances without triggering a broader economic and social crisis?

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet