Stagflation Risk Back? Oil Spike Puts Fed in a Bind

Amid escalating tensions in the Middle East and persistently elevated oil prices, the Federal Reserve is about to release its latest rate decision and dot plot.

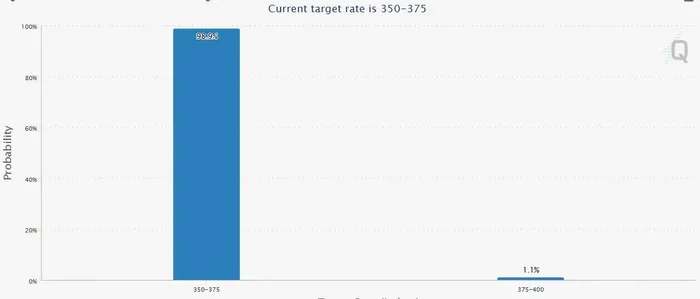

According to FedWatch, there is virtually no uncertainty around the rate decision itself: markets assign a 99% probability to no rate cut and only a 1% chance of a hike. As a result, investor attention is fully focused on the dot plot and Chair Jerome Powell’s remarks.

With no clear timeline for the reopening of the Strait of Hormuz and crude oil prices remaining elevated, the dot plot will provide critical insight into policymakers’ rate outlook: Will the Fed still deliver two cuts this year, one cut, or none at all?

On the macro side, the Fed may revise 2026 unemployment forecasts higher, along with core PCE inflation projections.

Following the dot plot, markets will closely parse Powell’s press conference for guidance. The U.S. labor market is already showing signs of softening, which would typically justify rate cuts. However, surging oil prices are reintroducing inflation risks.

The key concern for markets is clear: is stagflation making a comeback? How Powell balances inflation and employment will be the central focus for investors.

How Will the Fed Respond to the Oil Shock?

The Federal Reserve is currently facing a classic stagflation dilemma: rising inflation alongside growing downside risks to economic growth.

In theory, the Fed should look through one-off energy shocks and focus on core inflation, which excludes volatile food and energy components. During the March 2022 Russia–Ukraine conflict, Powell emphasized that while energy prices would rise, the broader inflation impact would be limited, and the Fed should focus on inflation expectations.

Subsequent Fed research largely validated this view. The oil price surge triggered by the conflict increased U.S. headline inflation by roughly 1 percentage point in Q1 2022, contributing about 0.5 percentage points to full-year inflation.

However, after stripping out volatile energy components, core PCE rose only 0.17%, while U.S. GDP growth declined by just 0.13%.

Further estimates suggest that a 10% increase in oil prices would:

Raise headline PCE by 0.2%

Raise core PCE by 0.04%

Reduce GDP growth by 0.1 percentage point

These effects are generally considered manageable. If oil prices subsequently normalize, the impact could be reduced by roughly half.

Why This Time May Be Different

However, historical comparisons may be misleading, as today’s macro backdrop differs significantly from 2022.

First, the starting point for inflation is much higher. In early 2022, core PCE had only just exceeded the Fed’s 2% target, and markets were only beginning to closely monitor inflation dynamics.

Today, inflation has remained above 2% for five consecutive years, and the Fed’s earlier “transitory inflation” narrative has significantly damaged its credibility.

According to University of Michigan surveys, long-term inflation expectations have stayed above 3% for two consecutive years.

In this context, any premature signal of policy easing risks unanchoring inflation expectations. With Powell approaching the end of his term, he is likely to adopt a more cautious stance and avoid repeating past policy missteps.

Tariffs and Oil: A Compounding Inflation Shock

This latest oil price surge coincides with the implementation of reciprocal tariffs, further complicating the inflation outlook.

February CPI data shows that 13 out of 21 tariff-sensitive categories recorded price increases, with particularly strong gains in categories such as apparel and household goods.

Importantly, February CPI did not yet reflect the latest spike in oil prices. Until the transmission mechanism from energy prices to broader inflation becomes clearer, the Fed’s optimal strategy is likely to remain wait-and-see.

What Are Investment Banks Saying?

There is broad consensus across major investment banks that the Fed will hold rates steady at this meeting.

The recent surge in energy prices has introduced significant uncertainty into the inflation outlook, prompting a shift in policy focus toward “wait and see.”

In addition, the Fed’s Summary of Economic Projections (SEP) is expected to exhibit stagflationary characteristics, with:

Higher inflation forecasts

Slightly lower growth projections

The key divergence lies in the timing of the next rate cut.

Bullish camp (ANZ, Wells Fargo): Oil shocks are temporary, and a weaker-than-expected labor market will lead to two rate cuts this year

Bearish camp (Crédit Agricole): Rate cuts may be delayed for the entire year

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet