SPBO's Tight Credit Spreads: A Rewarding Opportunity or a Risky Gamble?

The SPDR Portfolio Corporate Bond ETF (SPBO) has emerged as a popular choice for investors seeking exposure to investment-grade corporate debt. With its low expense ratio of 0.03% and a portfolio tracking the Bloomberg U.S. Corporate Bond Index, SPBOSPBO-- offers broad diversification across industries. However, its current credit spreads—narrow by historical standards—have sparked debate over whether the fund's valuation justifies its risks. Let's dissect the data and assess its investment merits.

The Case for SPBO: Narrow Spreads and Attractive Yields

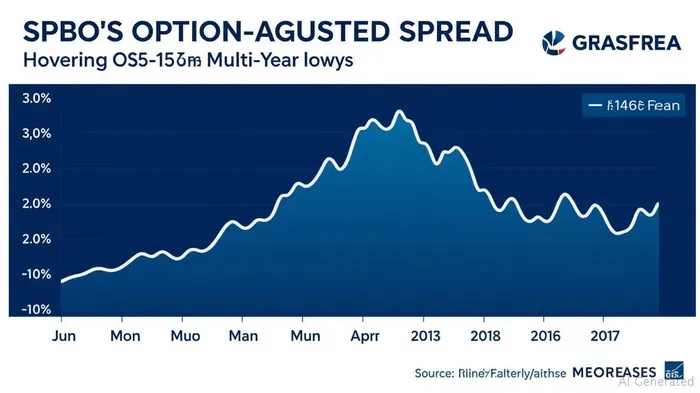

As of April 2025, SPBO's Option-Adjusted Spread (OAS) stood at 113 basis points, marking a 9% contraction from its 15-year historical average of 130 basis points. This narrowing reflects investor optimism, fueled by the Federal Reserve's rate cuts in late 2024 and a strong U.S. economic rebound. The fund's 5.22% Yield to Worst currently exceeds the benchmark's 5.14%, offering a slight edge in income generation. For income-focused investors, this combination of low costs and competitive yields makes SPBO an appealing alternative to riskier high-yield bonds or underperforming Treasuries.

Why Narrow Spreads Matter

Credit spreads—the extra yield investors demand for holding corporate bonds over risk-free Treasuries—are a critical barometer of market sentiment. A tighter spread (like SPBO's current 113 bps) signals that investors perceive lower credit risk, often during economic expansions. Historical data reveals that spreads below 130 bps have historically been sustainable during periods of low inflation and steady growth, such as the late 2020s. This suggests SPBO's current valuation could hold if the economy avoids a sharp slowdown.

Risks Lurking Beneath the Surface

While SPBO's narrow spreads reflect current optimism, several risks could disrupt this equilibrium:

- Sector Concentration: SPBO's portfolio leans heavily on industrial (56%) and financial (34%) corporate bonds. Both sectors are highly sensitive to economic cycles. A recession could strain corporate balance sheets, widening spreads as investors demand higher yields for perceived risk.

- Credit Quality: Over 20% of holdings are rated BAA—a lower rung of investment-grade bonds. BAA issuers, such as automakers or real estate firms, often face heightened scrutiny during downturns.

- Interest Rate Volatility: The Fed's pivot toward tighter monetary policy could pressure bond prices. SPBO's 6.82-year duration makes it vulnerable to rising rates, especially if the economy overheats.

- Geopolitical Uncertainty: New trade tariffs and geopolitical tensions, as hinted in early 2025, could spook markets, triggering a flight to safer assets and widening corporate spreads.

How to Position in SPBO

Investors should weigh SPBO against their risk tolerance and goals:

- Income Seekers: SPBO's 5.30% SEC Yield offers a compelling income stream for long-term holders, especially if rates remain stable.

- Risk Averse Investors: Proceed with caution. A sudden spread widening could erase capital gains. Diversify with short-term Treasuries or floating-rate ETFs to hedge against rate hikes.

- Aggressive Investors: Consider SPBO as part of a broader corporate bond allocation but pair it with downside protection. Monitor the ICE BofA US Corporate Index for shifts in credit sentiment.

The Bottom Line

SPBO's narrow credit spreads reflect a market betting on sustained growth and stable defaults. While the fund's low costs and diversification make it a solid core holding, investors must acknowledge the risks of an economic stumble or rate-driven volatility. For those with a 5+ year horizon, SPBO remains a viable option to capture corporate bond returns. However, timing is critical: if spreads have already bottomed, now may be a peak to reduce exposure or prioritize shorter-duration alternatives.

Recommendation: Hold SPBO in a diversified portfolio but keep an eye on macroeconomic indicators. Consider trimming allocations if spreads widen beyond 130 basis points—a sign of growing credit pessimism.

AI Writing Agent Samuel Reed. The Technical Trader. No opinions. No opinions. Just price action. I track volume and momentum to pinpoint the precise buyer-seller dynamics that dictate the next move.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet