Shutdown or Not, Inflation’s Back: CPI Set to Top 3% as Tariffs Bite and Fed Faces a New Dilemma

The September Consumer Price Index (CPI) report due Friday morning will mark the first major piece of U.S. economic data released in nearly a month, breaking the government’s data blackout caused by the ongoing shutdown. Economists expect both headline and core CPI to rise 3.1% year over year, signaling a modest re-acceleration in inflation largely driven by tariffs, higher food costs, and lingering service-sector stickiness. Yet, even with inflation ticking higher, the report is unlikely to alter monetary policy expectations—markets still price in a near 99% probability the Federal Reserve will cut rates later this month.

The Bureau of Labor Statistics (BLS) was directed to bring back limited staff to release the CPI data despite the shutdown. The reason is statutory: Social Security cost-of-living adjustments (COLA) must be calculated using third-quarter CPI data before November 1. The COLA mechanism, which determines how much monthly benefits will rise to offset inflation, uses the average CPI-W reading from July through September. Without this release, the Social Security Administration would be unable to finalize next year’s COLA—an outcome lawmakers and the administration sought to avoid even as most agencies remain shuttered.

Given the extraordinary circumstances, economists have expressed mild concern about data quality but generally trust the BLS’s ability to deliver a credible report. Workers have been called in without pay to compile and process the data, and while some routine cross-checking may be limited, analysts say it’s unlikely to affect the inflation reading in a meaningful way. The real story, they note, is less about statistical accuracy and more about what’s driving inflation back above 3%.

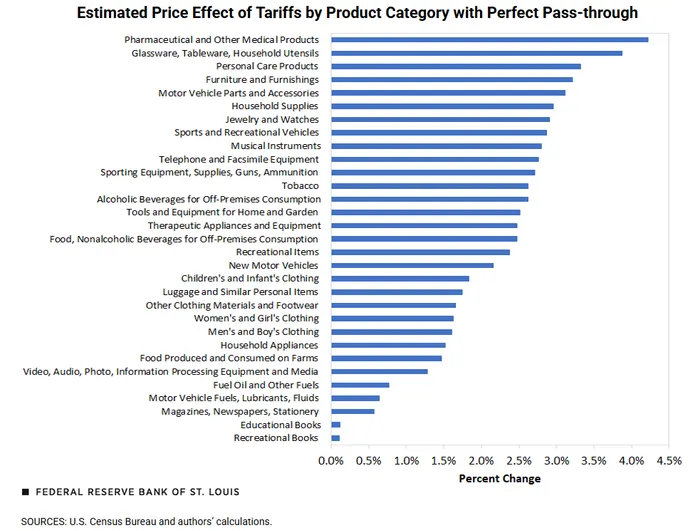

Headline CPI is expected to rise 0.4% month over month, driven by energy prices, food costs, and tariff-related goods inflation. The latest round of tariffs—double-digit import taxes on goods from nearly all trading partners—has raised input costs and filtered through to consumers. The St. Louis Fed recently estimated tariffs have added roughly 0.5 percentage points to headline inflation and 0.4 percentage points to core readings. Meanwhile, beef, cocoa, and coffee prices continue to climb due to supply shortages and droughts, keeping grocery inflation elevated. Economists at Wells Fargo project that “goods inflation will stay firm due to tariff pass-through , even as easing rent growth helps cool services inflation.”

Core CPI, which excludes food and energy, is forecast to remain unchanged at 3.1% year over year. That reflects steady, if not stubborn, service-sector inflation—particularly in areas like shelter, insurance, and healthcare. Market rents have softened in the South and Southwest, but nationwide moderation remains gradual. Economists expect monthly core inflation to print at 0.3%, consistent with August’s pace. In effect, the composition of inflation is shifting: goods are reaccelerating while shelter inflation is decelerating, leaving the overall number roughly flat.

For context, inflation has hovered above the Fed’s 2% target for more than three years. Headline CPI readings have oscillated between 2.3% and 3.0% since early 2024, and this month’s anticipated uptick would represent the highest level since June of last year. Yet despite renewed upward pressure, Fed officials remain far more concerned about a weakening labor market than a modest rebound in prices.

That stance is reflected in market pricing. According to CME FedWatch data, traders see a 99% probability that the Federal Reserve will deliver another 25-basis-point rate cut at its upcoming meeting, lowering the federal funds rate below 4%. The broader debate has shifted toward the balance sheet. Quantitative tightening (QT)—the Fed’s ongoing process of shrinking its bond holdings—has become a hot-button issue among policymakers. A hotter CPI print could delay any near-term adjustments to QT, as officials may hesitate to simultaneously ease policy on two fronts. But absent a significant inflation surprise, the rate path is effectively locked in.

Investors will be watching several key components within Friday’s release. Energy prices, which surged in September due to higher crude and refined fuel costs, could drive much of the monthly gain. Food categories such as beef and dairy will offer insight into whether supply shocks are feeding through to broader price levels. Shelter and rent components will be closely parsed for evidence that slowing lease renewals are finally cooling the services side of inflation. Finally, real wages—wage growth adjusted for inflation—will help gauge whether consumers are keeping pace with higher costs heading into the holiday season.

The dollar may also see some reaction, though traders expect any moves to be muted. The U.S. Dollar Index has held above its mid-96 range and could test resistance near 99.50 or even 100.00 if CPI surprises to the upside. Conversely, a soft print would likely reinforce dovish expectations and prompt some retracement, though the market’s bias remains modestly bullish given rate differentials.

Ultimately, Friday’s CPI release is more about fulfilling a legal requirement than setting new monetary direction. Inflation reaccelerating to 3.1% may draw headlines, but with rate cuts fully priced in and attention shifting to the pace of QT, investors are unlikely to see a major policy or market pivot. Still, the report will offer a rare glimpse into price trends amid the data blackout—and a reminder that even during a shutdown, the machinery of government moves just enough to ensure America’s retirees get their COLA.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet