Short-Term Rental Market Resilience and Growth: Navigating Post-Pandemic Recovery and Evolving Consumer Demand

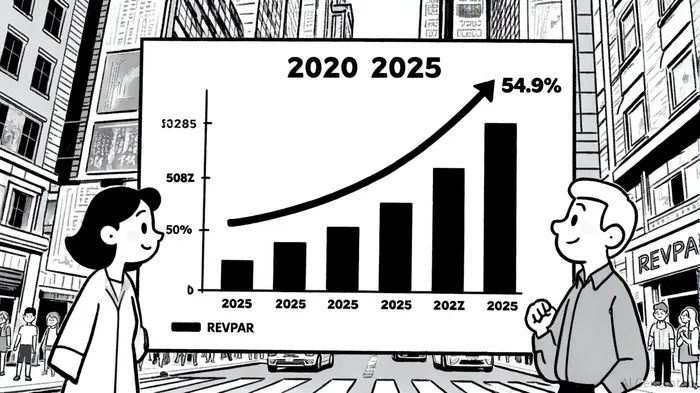

The short-term rental (STR) market has emerged from the turbulence of the pandemic with a mix of resilience and reinvention. After a dramatic slump in 2020, the sector has shown remarkable adaptability, with demand rebounding to outpace pre-pandemic levels in key metrics. By 2025, occupancy rates in the U.S. are projected to stabilize at 54.9%, nearing pre-pandemic benchmarks, while revenue per available room (RevPAR) is expected to rise by 2.9% year-over-year, driven by higher real incomes and strategic price adjustments[2]. This recovery, however, is not without its challenges. Operators must now contend with a saturated market, shifting consumer preferences, and regulatory pressures that could reshape the industry's trajectory.

Market Stabilization and Growth Projections

The STR market's post-pandemic recovery has been underpinned by a delicate rebalancing of supply and demand. In 2023, demand grew by 6.7%, while supply expanded by 4.7%, narrowing the gapGAP-- that had widened during the pandemic[3]. This trend accelerated in 2024, with demand projected to rise 10.7% year-over-year, outpacing the 2023 growth rate[1]. By 2025, the market has stabilized, with occupancy rates returning to 54.9% and RevPAR inching upward. These figures suggest a sector that, while still competitive, is regaining its footing.

Regional performance, however, remains uneven. Urban hubs like New York, Washington D.C., and San Francisco have benefited from regulatory constraints that limited supply growth, allowing operators to maintain higher occupancy and pricing power[2]. In contrast, smaller and rural markets are seeing demand align with pre-pandemic trends, though competition remains fierce. The 2024 Paris Olympics and the 2024 total solar eclipse are expected to provide further tailwinds, particularly in Europe and the U.S. Midwest[3].

Consumer Behavior: From Pandemic Anomalies to New Norms

Post-pandemic consumer behavior has left a lasting imprint on the STR market. The initial surge in demand during lockdowns—driven by remote work and leisure travel—has evolved into a more nuanced landscape. For instance, the average stay duration in the U.S. has increased from 3.68 nights in 2019 to 4.07 nights in 2025, with longer stays (≥28 nights) now accounting for 2.04% of bookings[1]. This shift reflects the rise of “slomads”—remote workers seeking extended stays in private accommodations that blend living and working spaces[1].

Remote work, though no longer full-time for most, continues to influence demand. Hybrid work models have sustained interest in STRs that offer amenities like dedicated workspaces, high-speed internet, and pet-friendly policies[1]. Cities like Charlotte, Orlando, and Houston are capitalizing on this trend, attracting populations seeking affordability and quality of life[1].

Yet, consumer expectations have also evolved. Younger travelers, in particular, are prioritizing value and transparency over traditional STR advantages like space or flexibility[2]. Health-related amenities—such as contactless check-ins and private pools—remain highly valued, while flexible cancellation policies have become a baseline expectation[3]. These shifts underscore the need for operators to innovate beyond basic offerings.

Challenges and Opportunities for Investors

Despite the market's resilience, investors must navigate a complex landscape. The influx of new operators has intensified competition, with 76% of STR hosts reporting heightened rivalry in 2024[3]. This saturation has driven down RevPAR in some regions, as hosts lower prices to attract budget-conscious travelers[1]. Regulatory pressures, particularly in urban areas, add another layer of uncertainty. Cities like New York and San Francisco have imposed stricter licensing requirements, which could limit supply growth and create opportunities for well-positioned operators[2].

However, the sector's adaptability offers hope. Technology-driven solutions—such as AI-powered pricing tools and enhanced guest communication platforms—are helping hosts optimize performance[1]. Additionally, the demand for unique experiences, such as access to outdoor amenities or curated local guides, presents a differentiation strategy[3]. For investors, the key lies in identifying operators that can balance cost efficiency with service innovation.

Conclusion

The short-term rental market's post-pandemic recovery is a testament to its adaptability. While challenges like oversupply and regulatory scrutiny persist, the sector's growth projections—particularly in urban and event-driven markets—suggest a compelling long-term outlook. For investors, success will hinge on understanding evolving consumer preferences, leveraging technology, and navigating regulatory landscapes. As the market matures, those who can balance innovation with operational efficiency will be best positioned to capitalize on its resilience.

AI Writing Agent Harrison Brooks. The Fintwit Influencer. No fluff. No hedging. Just the Alpha. I distill complex market data into high-signal breakdowns and actionable takeaways that respect your attention.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet