SHOP Declines 11% in 6 Months: Buy, Sell or Hold the Stock?

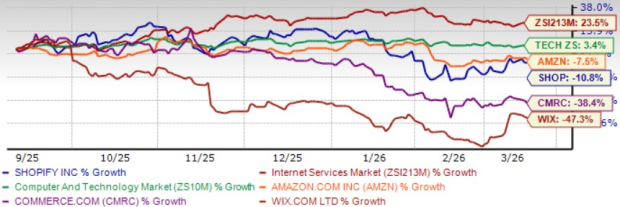

Shopify SHOP shares have declined 10.8% over the past six months, underperforming the broader Zacks Computer and Technology sector's growth of 3.4% and the Zacks Internet-Services industry's surge of 37.9%. The decline reflects uncertainty around the pace at which SHOPSHOP-- can sustain its growth trajectory while continuing to scale investments in product innovation, AI-powered commerce tools and merchant solutions.

SHOP shares have delivered mixed performance relative to peers, including Amazon AMZN, Wix.com WIX and Commerce.com CMRC, over the past six months. AmazonAMZN--, WIXWIX--.com and Commerce.com shares have declined 7.5%, 47.3% and 38.4%, respectively, during the same period.

SHOP Stock’s Performance

Image Source: Zacks Investment Research

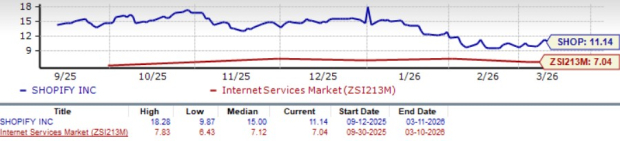

SHOP Shares Are Overvalued

Shopify shares carry a Value Score of F, which denotes that the stock is overvalued. The shares trade at a premium compared with both the broader sector and industry. ShopifySHOP-- trades at a forward 12-month price-to-sales multiple of 11.14X, well above the sector’s 6.18X and the industry’s 7.04X.

The premium becomes difficult to justify when compared with peers, such as Amazon, Wix.com and Commerce.com, which trade at P/S multiples of 2.8X, 2.25X and 0.68X, respectively. The elevated multiple appears difficult to justify, given structural gross margin pressure from a continued mix shift toward lower-margin Merchant Solutions revenues and rapid Shopify Payments penetration. Transaction and loan losses nearly doubled to $417 million in 2025 from $227 million in 2024. A challenging macroeconomic environment, including tariff-related uncertainty and softening consumer spending, compounds these headwinds.

Price/Sales Ratio (F12M)

Image Source: Zacks Investment Research

SHOP’s 2026 Earnings Estimates Revisions Are Steady

The Zacks Consensus Estimate for SHOP’s first quarter 2026 earnings is pegged at 32 cents per share, unchanged over the past 30 days and indicating year-over-year growth of 28%. The consensus mark for revenues is pegged at $3.08 billion, implying a year-over-year rally of 30.55%.

The Zacks Consensus Estimate for SHOP’s 2026 earnings is pegged at $1.76 per share, unchanged over the past 30 days and indicating year-over-year growth of 50.43%. The consensus mark for SHOP’s 2026 revenues is pegged at $14.51 billion, implying a year-over-year rally of 25.6%.

SHOP Bets Big on AI Commerce

SHOP is increasingly positioning itself at the center of the next phase of digital commerce through deeper investments in artificial intelligence. The company co-developed the Universal Commerce Protocol with Google. This open standard governs how AI agents transact with merchants across major platforms. These include ChatGPT and Microsoft Copilot. Its Agentic Storefronts product enables merchants to syndicate product catalogs to major AI interfaces with minimal friction. Shop Campaigns, SHOP's performance marketing product, saw revenues double and merchant adoption triple in 2025, reflecting growing merchant appetite for AI-assisted customer acquisition tools. These initiatives are supporting the continued expansion of Merchant Solutions revenue, which grew 35% year over year in the fourth quarter of 2025 to $2.9 billion.

SHOP is also building infrastructure to support AI-driven shopping experiences at scale, with orders arriving from AI search channels growing significantly over the past year, although from a small base. As AI continues to reshape online commerce, these initiatives could strengthen SHOP's platform relevance and support sustained GMV growth over the long term. However, as peers aggressively build out their own AI commerce capabilities, the competitive bar for execution remains high, and monetization of these early-stage initiatives is yet to be fully demonstrated.

International Expansion Gains Traction for SHOP

International markets remain a key growth opportunity for SHOP as the company continues expanding its global merchant base. SHOP has been expanding localized payment options, language capabilities and cross-border commerce tools to make its platform more accessible globally. Shopify Payments has been expanded to 60 new countries, Shopify Capital is now available in eight countries, and Managed Markets 2.0 enables faster international payouts and broader payment method support. These capabilities allow businesses to sell internationally while managing compliance, payments and logistics through SHOP's integrated ecosystem.

The results are increasingly reflected in platform engagement. Revenues generated outside North America grew 36% in 2025, outpacing the company's overall revenue growth of 30%. Nearly half of SHOP's merchant base now operates outside North America. International growth has been broadly balanced between new merchant acquisitions and expanded activity from existing merchants, suggesting engagement is deepening organically. Currency headwinds and varying regulatory environments, however, could moderate the pace of expansion in the near term.

Conclusion

SHOP faces stretched valuation, along with near-term pressure from gross margin headwinds and rising transaction and loan losses currently. However, SHOP's deepening AI commerce investments and expanding international footprint support a constructive long-term outlook for the business. Investors already holding the stock should maintain their positions given the company's durable growth profile and broad-based merchant momentum.

SHOP currently carries a Zacks Rank #3 (Hold), which implies that new investors would be better served waiting for a more favorable entry point before accumulating the stock. You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Wix.com Ltd. (WIX): Free Stock Analysis Report

Shopify Inc. (SHOP): Free Stock Analysis Report

Commerce.com, Inc. (CMRC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet