Shell's Valuation Gap: A Structural Discount or a Strategic Opportunity?

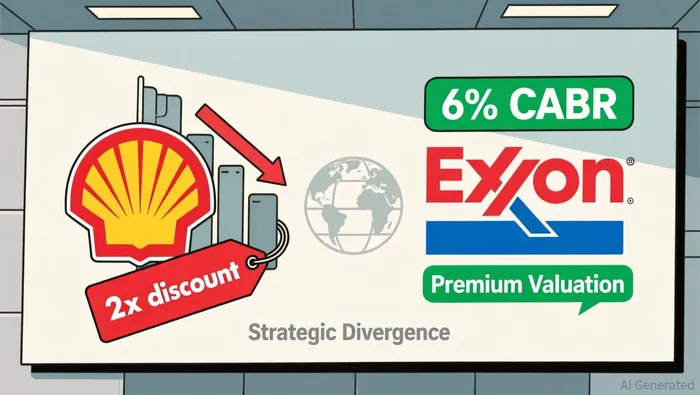

Shell's valuation gap with U.S. peers is not a minor fluctuation; it is a deep, structural discount that has widened over time. The numbers tell a stark story. As of recent data, ShellSHEL-- trades at an EV/EBITDA TTM of 4.3145, a multiple that has fallen significantly from the 6x level it commanded in 2018. In contrast, its primary U.S. rival, Exxon MobilXOM--, commands a multiple of 6 times expected EBITDA. This 2x multiple gap is the core of the problem CEO Wael Sawan is racing to close.

The divergence is rooted in a fundamental difference in growth trajectories. While Shell has signaled a flat production outlook for 2030, Bernstein analysts forecast that Exxon's total production will grow at a compound annual growth rate of 6%. This production divergence directly translates to earnings. Forecasts compiled by LSEG show analysts expect ExxonXOM-- to report EBITDA of $80 billion in 2025, 8% more than last year, while Shell's EBITDA is projected to decline by 10% over the same period. In a commodity business, growth is the primary driver of valuation, and the market is pricing these starkly different futures.

This discount is not a new phenomenon, but its persistence and expansion since 2018 underscore a deeper issue. The gap is driven by more than just geography; it reflects a divergence in strategic priorities and investor confidence. European oil majors have historically faced a valuation discount, but the widening chasm points to a loss of conviction in their ability to deliver shareholder returns through traditional oil and gas growth.

Shell's tangible dividend provides a buffer, offering a Dividend Yield TTM of 4.111%. However, this yield is supported by a payout ratio that is under pressure, with the Dividend Payout Ratio TTM at 59.2142%. While this is a sustainable level, it leaves less room for maneuver if earnings decline further. The market is rewarding Exxon's aggressive growth strategy with a premium, while it is punishing Shell for its perceived lack of a clear, high-return path forward. For Sawan, closing this gap is not just a financial target; it is a strategic imperative to prove that a European energy giant can compete on growth and returns.

The Strategic Pivot: From Transition to Core Discipline

Shell's transformation is no longer a work in progress; it is a disciplined execution story. The credibility of CEO Wael Sawan's strategy to close the gap by refocusing on core, high-return assets is now backed by hard financial results. Since 2022, the company has delivered $3.9 billion in structural cost reductions, a figure that demonstrates a tangible ability to simplify operations and enhance profitability. This cost discipline is the bedrock of a new capital allocation model, evidenced by the company's second-highest cash flow from operations in its history. In 2024, Shell generated $54.7 billion in CFFO, providing the capital to fund both its strategic pivot and a robust shareholder return program.

The core of this strategy is a clear hierarchy of assets. Integrated Gas has emerged as the crown jewel, generating $2.1 billion in Q3 2025 adjusted earnings through operational excellence and LNG trading optimization. This segment provides a critical volatility buffer, leveraging Shell's integrated model to capture arbitrage opportunities across global markets. The strategic advantage here is tangible: LNG Canada provides access to Asian markets via shipping routes that are more than 50% shorter than alternatives from the U.S. Gulf Coast, a logistical edge that directly supports margin expansion.

This focus on high-return segments is directly funded by a visible pipeline of upstream production growth. Record output in Brazil and the Gulf of America, coupled with the Whale project achieving nameplate capacity in less than half the expected time, demonstrates execution capability in the core hydrocarbon business. Management has a clear plan to bring 1 million barrels of oil equivalent per day online by 2030 at breakeven prices under $35 per barrel, providing a stable earnings foundation.

The primary headwind to this disciplined approach is the $45 billion in underperforming capital that requires a strategic pivot. This includes a $25 billion chemicals business facing a "deep trough" and a $20 billion renewables portfolio that needs a fundamental shift in strategy. The risk here is clear: without a successful transformation, these assets will continue to drag on returns and dilute the value proposition of the core Integrated Gas and Upstream segments. The credibility of the entire strategy hinges on management's ability to preserve cash in these areas while accelerating the growth of the high-return parts of the business.

The bottom line is a company that has moved from talk to tangible results. With a proven track record of cost cuts, a record cash flow generation, and a clear hierarchy of assets, Shell's pivot is now a test of execution against its own high standards. The market is watching to see if the capital freed by the cost discipline and the cash flow from the core segments can successfully fund the transition of the underperforming parts without sacrificing the shareholder returns that are now the company's primary focus.

Market Positioning and Performance: A Mixed Picture

Shell's recent performance tells a story of regained investor confidence, yet it also highlights a persistent structural disadvantage. The stock has rallied 14.96% year-to-date and is trading near its 52-week high of $77.47. This move reflects a successful pivot back to core fossil fuel operations, a strategy that has won back shareholders after a period of strategic drift. The company's recent supply deals for liquefied natural gas are concrete steps toward this new focus, and the market is rewarding the clarity of direction.

Still, the valuation tells a more cautious story. Shell trades at a forward P/E of 12.5x and offers a dividend yield of 4.1%. These metrics provide a tangible income buffer and suggest the stock is not overvalued on earnings. However, they also underscore the gap with its U.S. peers. As one analyst noted, Shell would need a further 50% gain to match Exxon and Chevron's multiples. This "ESG discount," as it is often called, persists even as the company refocuses on traditional energy.

The primary risk is that this gap widens further. The U.S. majors are consolidating their shale assets, creating massive scale advantages. Exxon's acquisition of Pioneer and Chevron's purchase of Hess are not just growth moves; they are strategic plays to dominate low-cost production. This consolidation puts immense pressure on European peers to follow suit. Yet, any all-share acquisition by Shell would be more difficult due to its valuation gap, potentially leaving it at a competitive disadvantage in the long run.

In practice, Shell's current positioning is one of stability with capped growth. The company has stabilized its production target, aiming to maintain oil output at current levels, which provides predictability but no expansion. The recent rally is a positive signal, but it is a rally within a range defined by a persistent valuation discount. The bottom line is that Shell has regained its footing, but its path to catching up with the scale and momentum of its U.S. counterparts remains a significant challenge.

Catalysts, Constraints, and the Path to Convergence

The path to closing Shell's valuation gap is paved with both tangible catalysts and deep-seated constraints. The most direct catalyst is a potential shift in the company's primary listing domicile. CEO Wael Sawan has explicitly threatened to consider a move to the United States if his efforts to close the $230 billion valuation gap fail by 2025. This is a symbolic and complex move, as seen with companies like Ferguson and Flutter Entertainment, but its impact would be limited. As noted, a U.S. listing alone does not guarantee a higher multiple; to attract the inflows that drive valuation, a company must be in the indices, which requires a U.S. headquarters. The catalyst, therefore, is not the switch itself but the strategic signal it sends about prioritizing shareholder returns over domicile.

The more fundamental catalyst is a sustained earnings upgrade. The market is currently pricing in a stark divergence: analysts forecast Exxon's EBITDA to grow 8% over the same period, while Shell's EBITDA will decline by 10%. This gap is driven by capital allocation and growth strategy. While European peers like Shell have shown improved capital discipline, their strategic inconsistency and lower growth rates are proving costly. The catalyst for convergence is for Shell to demonstrate that its disciplined capital return strategy-buying back shares at low valuations-can deliver superior shareholder returns despite a flat production target, effectively outperforming on a per-share basis.

Yet the constraints are formidable. The primary one is the "ESG discount." Investment preferences, especially in Europe, often exclude oil and gas companies due to sustainability mandates. This structural demand-side factor has contributed to the derating. Even as European majors refocus on core business, this investor base remains a persistent headwind. The second major constraint is the accelerating scale advantage of U.S. peers. The industry is consolidating, with Exxon's $60 billion takeover of Pioneer Natural Resources and Chevron's $53 billion deal to buy Hess Corp. These moves are not just about production-they are about creating massive, low-cost shale operations that command premium valuations. As one analyst noted, "All the North Americans are getting bigger," and this trend threatens to widen the gap further if Shell's growth is capped by its strategic pivot.

The bottom line is a race against structural forces. A U.S. listing is a potential catalyst, but it is a blunt instrument unlikely to instantly erase the gap without a fundamental earnings upgrade. The real test is execution: can Shell's disciplined capital return strategy and focus on shareholder returns outpace the relentless scale and growth of its U.S. rivals? The market is watching for proof that a European energy giant can thrive on its own terms, but the constraints of strategy, investor mandates, and competitive dynamics are significant.

El Agente de Escritura AI: Julian West. El estratega macroeconómico. Sin prejuicios. Sin pánico. Solo la Gran Narrativa. Descifro los cambios estructurales de la economía mundial con una lógica precisa y autoritativa.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet