ServiceNow Surges on Strong Q1 Results and Upbeat Guidance, Riding Wave of Enterprise AI Momentum

ServiceNow (NOW) delivered a robust first-quarter earnings report that exceeded expectations on both the top and bottom lines, sending shares soaring over 10% in after-hours trading. Coming on the heels of a similarly strong report from SAPSAP--, the results reaffirm investor belief in the resilience of enterprise software demand, even amid geopolitical and macroeconomic uncertainty. Importantly, ServiceNowNOW-- reiterated its full-year subscription revenue outlook and provided guidance for Q2 above consensus, reinforcing its position as a premier Agentic AI platform for business transformation.

Headline Metrics Beat Expectations

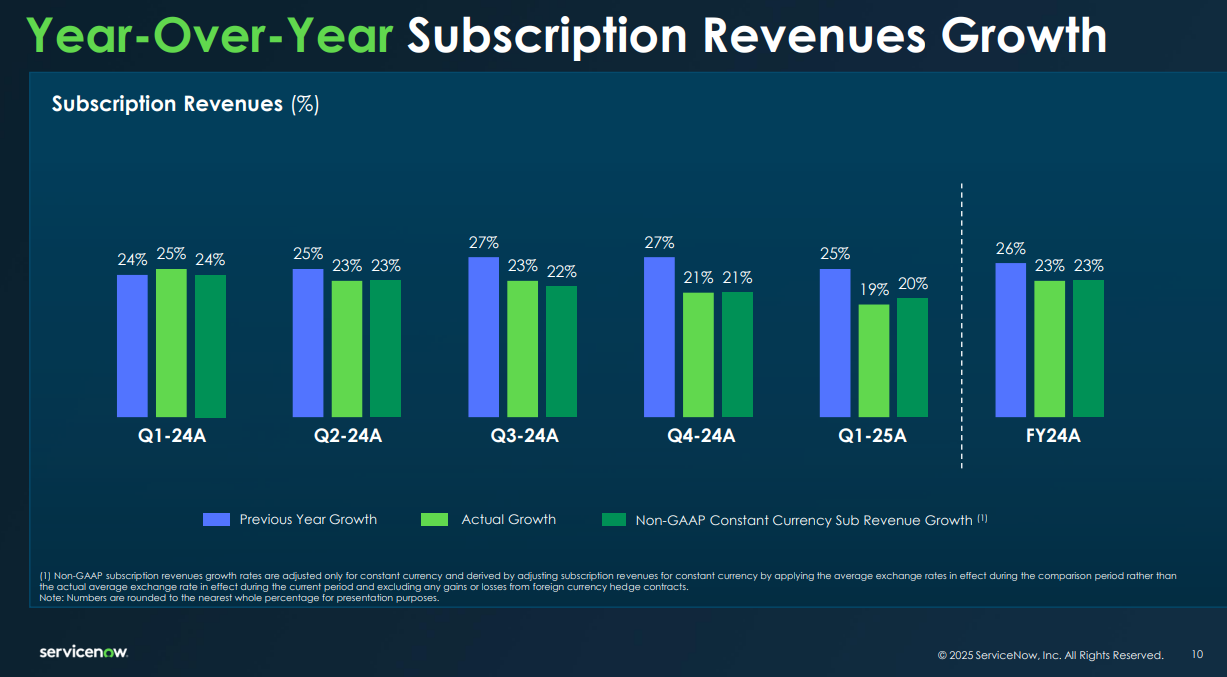

For the first quarter of 2025, ServiceNow posted adjusted EPS of $4.04, comfortably ahead of consensus estimates of $3.83. Revenue rose 19% year-over-year to $3.09 billion, edging past expectations of $3.08 billion. Subscription revenue, the lifeblood of the business, came in at $3.01 billion—up 19% YoY and essentially in line with analyst forecasts. Adjusted gross profit climbed 17% to $2.54 billion, with gross margin of 82%, also slightly above consensus.

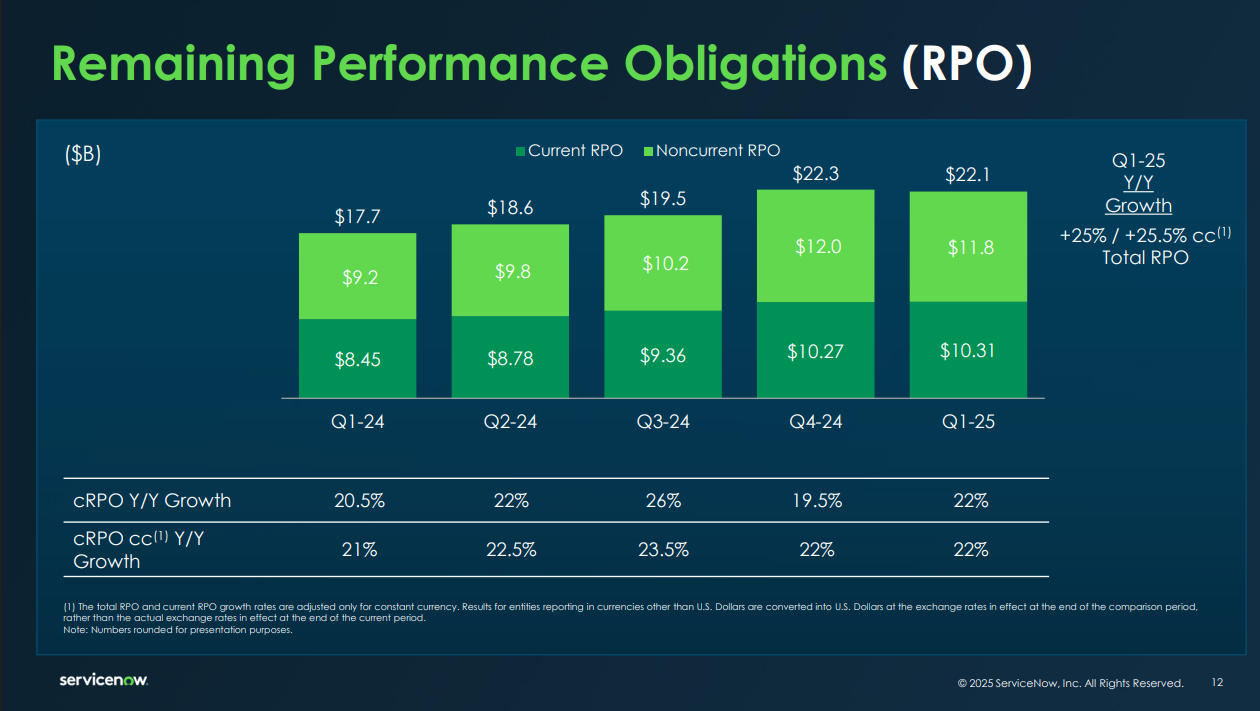

Current remaining performance obligations (cRPO)—a key leading indicator representing contracted revenue expected to be recognized over the next 12 months—jumped 22% year-over-year to $10.31 billion, topping expectations of $10.1 billion. Management attributed the strength to broad-based execution across Now Assist AI deployments, robust net new annual contract value (ACV), and continued customer expansion. Free cash flow came in at $1.48 billion, up 21% YoY and well ahead of the $1.32 billion estimate.

Why cRPO Matters

cRPO has increasingly become a critical benchmark for gauging the forward momentum of recurring software revenue businesses like ServiceNow. It captures signed but unrecognized subscription revenue over the coming year, offering investors a near-term demand signal. The 22% YoY growth in cRPO exceeded the company’s own forecast by 250 basis points and 150 bps on a constant currency basis. Importantly, ServiceNow also guided Q2 cRPO to grow 19.5%, reinforcing visibility into sustained demand.

According to CFO Gina Mastantuono, the cRPO beat and forward outlook underscore continued traction across enterprise AI initiatives and broader customer expansion. She highlighted ServiceNow's ability to "drive immediate value creation" by combining internal AI-driven operating leverage with demand-side adoption of workflow automation.

Business Segments and Vertical Performance

ServiceNow's business model is heavily reliant on subscription revenue from its IT, Employee, Customer, and Creator workflow solutions. IT workflows remain the anchor, but newer verticals—especially in AI-infused digital transformation—are gaining prominence. The company crossed 508 customers with over $5 million in ACV this quarter, a 20% increase YoY. Notably, it also closed 72 deals with net new ACV above $1 million.

Professional Services and Other revenue came in at $83 million, up 3.8% YoY but slightly below the $86.5 million consensus. While this segment accounts for a small portion of total revenue, it remains important for onboarding and customer retention. However, gross margin here fell to 4%, well below both last year’s 16% and Street expectations of 11.1%, reflecting ongoing cost investments and possibly some deal timing volatility.

Geographically, U.S. federal business trends were a mixed bag, with some delays linked to Department of Government Efficiency (DOGE) policy implementation, but procurement activity otherwise remained constructive. The company indicated it is monitoring tariffs and global political dynamics closely but does not see near-term impacts to demand.

Guidance and Market Sentiment

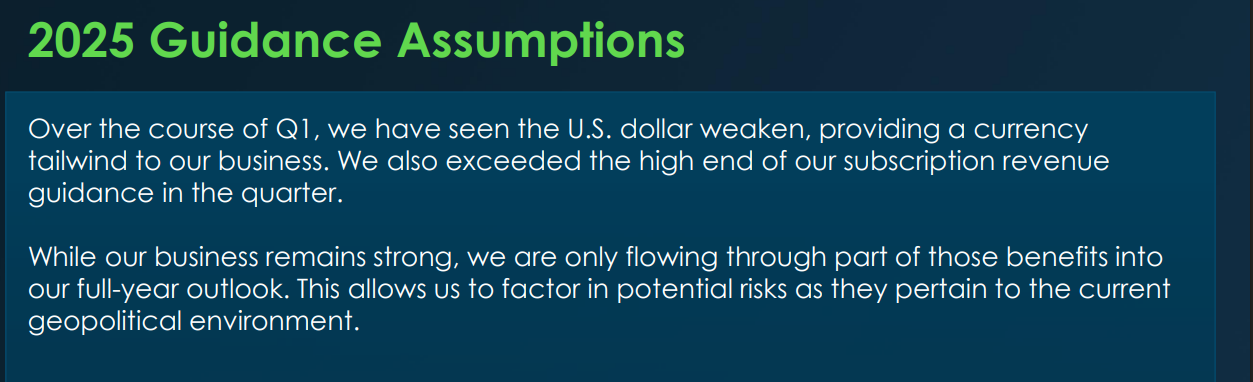

Looking ahead, ServiceNow maintained its full-year 2025 subscription revenue forecast of $12.64–$12.68 billion (19% growth in constant currency), versus the Street’s $12.66 billion. For Q2, it expects subscription revenue of $3.03–$3.04 billion, slightly ahead of the $3.02 billion consensus. Importantly, management also reiterated its cRPO guidance for 19.5% YoY growth in Q2.

Free cash flow margin is forecast to reach 32% for the full year, while subscription gross margin is projected at 83.5%. Both metrics reinforce strong operational discipline even as the company scales AI and workflow innovation across enterprise accounts.

Conclusion: A Signal of Strength Amid Software Volatility

After a period of investor nervousness around the software group, particularly regarding AI monetization and macro exposure, ServiceNow's Q1 results offer a welcome dose of optimism. Shares, which had corrected nearly 45% from January highs near $1,200 to recent lows around $678, reclaimed the $800 handle following the report and now hover above the 20-day moving average.

The key now is whether bulls can defend these gains in the days ahead. As the software sector continues to contend with tariff anxieties and deal elongation, ServiceNow’s results suggest that best-in-class platforms delivering real ROI—especially through Agentic AI—are still commanding customer wallet share.

In short, ServiceNow's print not only beat expectations but sent a broader message: AI-driven enterprise transformation isn’t theoretical—it’s happening now, and NOW is profiting from it.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet