Service Sector Drives Inflation as Fed Tightens — What Sectors Survive?

The U.S. service sector has emerged as a pivotal driver of inflation in 2025, with shelter costs, medical care, and transportation services contributing to persistent price pressures. As the Federal Reserve tightens monetary policy to curb inflation, investors must recalibrate their portfolios to navigate the shifting economic landscape. Historical sector rotation strategies offer a roadmap for capital preservation and growth in this environment.

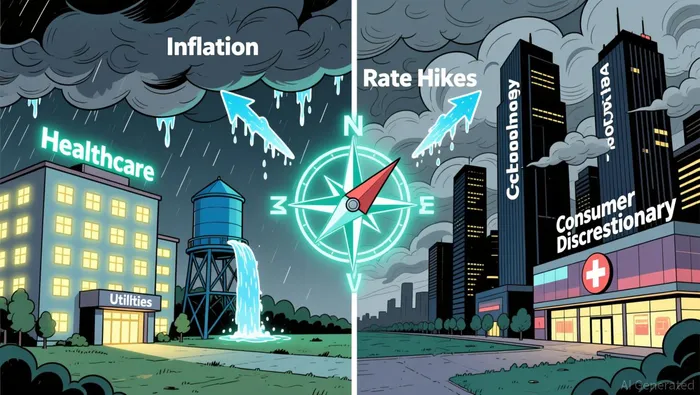

The Inflationary Landscape: Key Drivers and Risks

The December 2025 CPI report reveals a mixed picture: shelter costs rose 3.2% year-over-year, while medical care services climbed 3.5%. Airline fares surged 5.2% in a single month—the largest increase since 1993—highlighting the sector's vulnerability to supply-side shocks. Meanwhile, communication and used vehicle prices declined, offering pockets of relief. However, the core CPI for services less food and energy stands at 2.6%, signaling entrenched inflationary pressures.

The Federal Reserve's response—likely further rate hikes—poses risks for sectors sensitive to borrowing costs. Historically, tightening cycles have disproportionately impacted high-growth and discretionary sectors, while defensive and interest-sensitive sectors have outperformed.

Sector Rotation: Lessons from the Past

During the 2007–2009 financial crisis, investors who rotated into defensive sectors like Healthcare and Utilities outperformed those clinging to cyclical plays. Similarly, in 2025, the following strategies could prove effective:

- Defensive Sectors as Safe Havens

- Healthcare and Utilities: These sectors thrive in high-inflation environments due to their stable cash flows and essential services. For example, the Healthcare sector's 3.5% annual price increase underscores its resilience. Utilities, with their predictable demand and dividend yields, also benefit from rising interest rates.

Consumer Staples: Non-essential spending declines during tightening cycles, but staples like groceries and household goods remain resilient. The 1.5% drop in used car prices, however, suggests caution in overexposure to discretionary retail.

Cyclical Sectors: Timing the Rebound

- Energy and Materials: These sectors often outperform during inflationary peaks due to commodity demand. The 5.2% spike in airline fares and 3.6% rise in shelter costs indicate ongoing industrial activity, making Energy and Materials attractive for short-term gains.

Financials: Banks and insurers benefit from higher interest margins. The 67.5 Prices Index in July 2025, the highest since 2022, signals rising operational costs, which financial institutions may pass on to consumers.

Avoiding Vulnerable Sectors

- Technology and Consumer Discretionary: These sectors are highly sensitive to rate hikes and consumer confidence. The 1.9% decline in communication services and the 2.9% drop in hotel prices highlight their fragility.

Strategic Recommendations for 2025

- Rebalance Toward Defensive Plays: Allocate 40–50% of portfolios to Healthcare, Utilities, and Consumer Staples. These sectors have historically outperformed during tightening cycles, offering stability amid volatility.

- Hedge with Cyclical Exposure: Maintain 20–30% in Energy and Materials to capitalize on inflationary tailwinds. Monitor commodity prices and geopolitical risks for timing.

- Limit Exposure to High-Beta Sectors: Reduce holdings in Technology and Consumer Discretionary, which are prone to sharp corrections during rate hikes.

- Leverage Financials for Yield: Banks and insurers can provide income in a higher-rate environment, but assess their ability to absorb rising input costs.

Risks and Considerations

- Data Uncertainty: The government shutdown in October–November 2025 may distort inflation readings, creating noise in sector rotation signals.

- Global Supply Chains: Tariffs and trade tensions could prolong service-sector inflation, favoring sectors with pricing power.

- Labor Market Dynamics: A weakening labor market, as seen in the July 2025 ISM report, may delay the Fed's rate-cutting timeline, extending the duration of high-rate environments.

Conclusion

Rising service-sector inflation and tightening monetary policy demand a disciplined approach to sector rotation. By aligning portfolios with defensive sectors, hedging with cyclical plays, and avoiding overexposed areas, investors can navigate the storm while positioning for long-term growth. As the Fed's policy trajectory remains uncertain, continuous monitoring of inflation indicators and sector-specific fundamentals will be critical.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet