Semiconductor Sector Momentum: Diverging Institutional Sentiment Between Nvidia and AMD in Q3 2025

The semiconductor sector remains a cornerstone of global technological advancement, with artificial intelligence (AI) and high-performance computing (HPC) driving unprecedented demand. However, within this high-growth landscape, institutional investors are increasingly diverging in their outlooks for two industry titans: NVIDIA (NVDA) and Advanced Micro Devices (AMD). Q3 2025 data reveals a stark contrast in institutional ownership patterns and sentiment trends, reflecting broader debates over valuation, innovation, and market positioning.

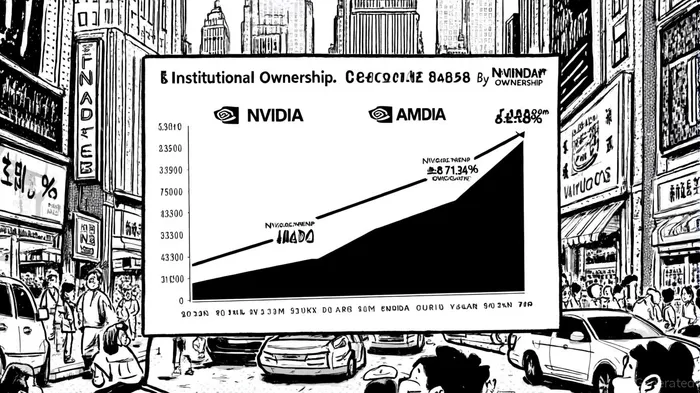

Institutional Ownership: Stability vs. Momentum

NVIDIA continues to attract heavy institutional backing, with Vanguard Group Inc. holding 8.88% of its shares (2.18 billion shares, valued at $292.67 billion) and BlackRock Inc. maintaining a 7.47% stake (1.84 billion shares), according to Tickergate ownership data. These positions underscore confidence in NVIDIA's dominance in AI software ecosystems and GPU leadership. Meanwhile, AMDAMD-- has seen a surge in institutional interest, with State Street Corp increasing its holdings by 2.3% since November 2024, netting a $11.5 billion position (4.3% ownership), according to an Investing.com analysis. As of July 2025, institutional ownership of AMD stands at 71.34%, with Vanguard, State Street, and Geode Capital collectively holding significant stakes, per MarketBeat institutional ownership.

Notably, AMD's institutional buying over the past two years has outpaced selling by $4.37 billion in value (205.5 million shares purchased vs. 176 million sold), according to MarketBeat. This contrasts with NVIDIA's more stable ownership structure, where recent additions like Munro Partners (4.07% stake) and GHE LLC (804,517 shares) reflect incremental confidence rather than a paradigm shift, as highlighted in the Investing.com analysis.

Sentiment Shifts: Valuation Arbitrage and Earnings Potential

The diverging institutional perspectives are amplified by valuation dynamics. AMD's forward P/E ratio of 17.66X and price-to-book (P/B) ratio of 3.9X position it as a compelling value play compared to NVIDIA's 22.57X P/E and 51.4X P/B, according to a TalkMarkets analysis. Analysts at Citigroup have capitalized on this gap, assigning AMD a "Buy" rating with a $200 price target-implying a 59% upside from its current price-while citing its competitive AI hardware and open-source ROCm platform as catalysts, as noted in the Investing.com analysis.

NVIDIA, meanwhile, retains a premium valuation despite recent volatility. Forty-six analysts cover its stock, with consensus projecting a 55% revenue increase for Q3 2025, according to the TalkMarkets piece. Recent analyst activity has focused on raising price targets, reflecting optimism about its proprietary software stack and data center dominance. However, AMD's projected 48.3% EPS growth over the next 12 months-outpacing NVIDIA's 41.3%-has drawn comparisons to its rival's slower momentum, as discussed in the Investing.com analysis.

Market Dynamics: Trade Tensions and Competitive Positioning

Both companies face headwinds from U.S.-China trade tensions, which have dampened demand for semiconductors in critical markets. Yet, AMD's lower valuation and expanding data center revenue (driven by its EPYC processors and Instinct MI300 AI accelerators) have made it a favored alternative for cost-conscious investors, per MarketBeat. NVIDIA's reliance on its closed-ecosystem software (e.g., CUDA) remains a double-edged sword: while it solidifies its AI leadership, it also limits flexibility for clients seeking open-source alternatives, according to MarketBeat.

Investment Implications

For institutional investors, the choice between NVIDIANVDA-- and AMD hinges on risk tolerance and growth expectations. NVIDIA's premium valuation reflects its entrenched leadership in AI and HPC, but its high P/E and P/B ratios leave less room for error. AMD, conversely, offers a lower-cost entry point with strong fundamentals and analyst support, though its ability to sustain growth amid intense competition remains untested.

As the semiconductor sector navigates macroeconomic uncertainties, the institutional shift toward AMD signals a growing appetite for value-driven bets in a market historically dominated by premium plays. However, NVIDIA's ecosystem advantages and recurring revenue streams ensure it remains a cornerstone of long-term AI infrastructure.

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet