"Sell on the Rumors" While Fundamentals Remain Intact as Q4 Earnings Reveal the Next Opportunities

More than half of S&P 500 companies have reported fourth-quarter earnings so far, with the Mag 7 excluding Nvidia already delivering results. Together, they offer a broad snapshot of the economic outlook and industry-specific trajectories. Earnings season is always a major stress test, especially with equity markets sitting near historical highs and investors becoming increasingly selective. When fundamentals remain solid, the focus naturally shifts toward alpha generation. The recent turbulence across banks, slowing AI monetization despite aggressive capital spending, and the sharp software sell-off all reflect that process. The question now is where patient investors should position for longer-term opportunities.

Banking Sector

The banking sector saw an initial pullback even though most institutions delivered better-than-expected fourth-quarter earnings. Management teams struck a cautious tone due to potential impacts from President Trump's proposed 10% credit card interest rate cap. Investors also leaned into a familiar "sell the ruomor" reaction following earnings, amplifying near-term downside but simultaneously creating selective buy-the-dip opportunities. What JPMorganJPM-- and Bank of AmericaBAC-- results already showed is that the financial environment remains healthy, with borrowers staying resilient and delinquency rates low. Morgan StanleyMS-- and Goldman SachsGS-- continued to benefit from strong wealth management activity and should maintain momentum as an IPO revival gains traction, particularly with more AI-related companies expected to list this year. Overall conditions remain favorable heading into the new year, and near-term volatility should not overshadow that backdrop. While many banking CEOs voiced concerns over a potential rate cap, past experience suggests the system tends to adapt, and the ultimate impact is often far less severe than initially feared.

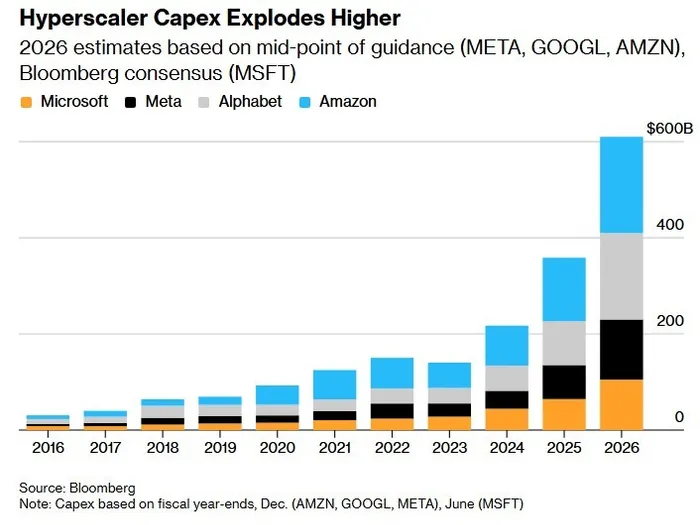

The Mag 7

The Magnificent Seven, excluding Nvidia, largely delivered earnings beats, yet the key issue lies elsewhere. AI monetization continues to lag behind the pace of capital spending on data centers, raising questions about the eventual payback period. Google, one of the biggest beneficiaries of the AI boom so far, saw its cloud revenue surge 48% year over year, driven by Gemini. However, the company also committed to roughly $180 billion in capital expenditure for 2026, more than double the prior year. Microsoft reported Azure growth of 39% year over year, slightly slower than before, while quarterly capital spending jumped 66% to $38 billion. Amazon's AWS posted 24% growth alongside plans for $200 billion in capital expenditure this year, up 53% annually. Meta also indicated its capital spending could double to $120 billion by 2026. Investors have remained patient because the long-term AI narrative is intact, but the scale of spending and rising depreciation risk could pressure margins, especially without a clear timeline for returns. Valuations are not particularly stretched, as many of these stocks have lagged the broader index, yet caution remains warranted given the absence of any visible slowdown in cash burn.

Semiconductors

On the other hand, massive capital commitments from major technology companies signal sustained demand for advanced chips. This dynamic continues to favor companies with clear competitive advantages such as Nvidia, Broadcom, TSMC, and Micron. These names have experienced similar sell-offs recently alongside the broader market, despite their structural positioning. AMD faced heavier pressure following weak guidance, but its GPU presence remains small relative to Nvidia, and recent order shifts involving major customers like OpenAI and Oracle highlight how competitive dynamics are still evolving. Even so, the fundamental outlook for semiconductor stocks remains intact as long as long-term AI investment continues. Consensus expectations for ongoing heavy spending suggest more participants will enter the race as competition accelerates.

Software

Advanced AI models have raised concerns about disruption to existing software ecosystems, triggering sharp sell-offs despite many companies having already embraced AI integration. We remain cautiously optimistic on the sector, as regulated and enterprise-grade software platforms are best positioned to deploy AI with efficiency and safety at scale. Palantir stands out as an example, combining data science with AI to drive faster business growth, positioning AI as a growth engine rather than a replacement threat. Panic around Claude's "Cowork" AI agent resembles another DeepSeek-style moment for Nvidia, yet history suggests such fears often fade. Software firms will need to innovate more aggressively to stay competitive, but the sector's adaptability should not be underestimated.

Crypto

Cryptocurrencies experienced panic selling after breaking the $80,000 and $70,000 psychological levels in succession, with negative sentiment spilling over into broader markets. At this stage, attempting to buy the dip appears premature, as confidence has deteriorated sharply amid a lack of concrete action from Trump. Compared with crypto, the AI thesis remains far more compelling, and selectively buying into software weakness offers a clearer risk-reward profile. In this environment, capital is better allocated toward areas where fundamentals, visibility, and long-term conviction remain stronger.

In the end, this earnings season reinforces a familiar but often misunderstood reality. Short-term volatility driven by headlines, policy noise, and valuation anxiety does not invalidate long-term structural trends. Banks remain fundamentally sound despite regulatory uncertainty, AI leaders continue to invest aggressively even as near-term returns lag, and semiconductors stand at the center of an expanding arms race that shows no sign of cooling. Software's sell-off reflects fear rather than obsolescence, while crypto's weakness underscores how quickly conviction can evaporate without tangible progress. For investors, the opportunity is not in chasing momentum or reacting to panic, but in selectively accumulating quality assets where fundamentals remain intact and long-term visibility is improving. This is a market that rewards patience, discipline, and a clear distinction between noise and signal.

Independent investment research powered by a team of market strategists with 20+ years of Wall Street and global macro experience. We uncover high-conviction opportunities across equities, metals, and options through disciplined, data-driven analysis.

Latest Articles

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Unlock Market-Moving Insights.

Subscribe to PRO Articles.

Already have an account? Sign in

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO