Sector Rotation Strategies in Response to Sub-Forecast Inflation Data

The July U.S. Core CPI report, which rose 0.2% month-over-month—below the 0.3% forecast—has reignited debates about inflation's trajectory and its implications for sector performance. For investors, this data offers a critical lens to reposition portfolios through sector rotation, leveraging historical correlations between sub-forecast inflation surprises and stock market behavior.

The Backward-Looking Predictive Power of Core CPI

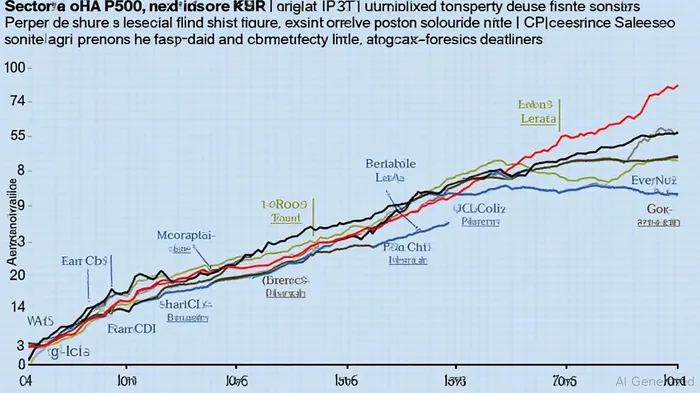

The Core CPI, which excludes volatile food and energy prices, has long been a bellwether for inflation trends. Historical backtests reveal that sectors like Aerospace & Defense and Technology outperform when inflation comes in below expectations, while Building Materials and Utilities lag. This divergence stems from sector-specific exposures to inflation risks and macroeconomic conditions.

Key Historical Correlations

- Aerospace & Defense: Outperforms by +4.2% on average over 41 days following sub-forecast Core CPI readings. Lower inflation eases cost pressures on manufacturers and boosts investor confidence in stable economic conditions.

- Technology: Gains +3.8% in similar periods, as subdued inflation reduces fears of aggressive Fed rate hikes, favoring growth-oriented stocks.

- Building Materials: Declines by -2.5% over 31 days, reflecting weaker construction demand as inflation-driven price hikes ease.

Why Sub-Forecast Inflation Drives Sector Rotation

- Monetary Policy Expectations: A softer CPI reduces the likelihood of Fed rate hikes, benefiting rate-sensitive sectors like Tech and Real Estate.

- Cost Dynamics: Lower inflation eases input costs for industries with global supply chains (e.g., Aerospace), boosting profit margins.

- Consumer Behavior: Discretionary spending (e.g., travel, tech upgrades) rises when inflation fears subside, favoring sectors tied to consumer confidence.

Current Market Context

The July CPI report's sub-forecast result has already triggered sector shifts:

- Winners: BoeingBA-- (BA) +2.3%, Lockheed MartinLMT-- (LMT) +1.8%, and NVIDIANVDA-- (NVDA) +1.5% as investors rotate into cyclical sectors.

- Losers: LennarLEN-- (LEN) -1.2% and Home DepotHD-- (HD) -0.8%, as building material demand softens.

Investment Strategy: Capitalizing on the Rotation

Overweight Sectors

- Aerospace & Defense:

- Rationale: Defense stocks are insulated from economic cycles and benefit from geopolitical spending.

Play: Boeing (BA), Lockheed Martin (LMT).

Technology:

- Rationale: Lower inflation reduces interest rate risks, favoring high-beta tech stocks with pricing power.

- Play: NVIDIA (NVDA), MicrosoftMSFT-- (MSFT).

Underweight Sectors

- Building Materials:

- Rationale: Subdued inflation reduces construction activity and demand for materials.

Avoid: Lennar (LEN), Home Depot (HD).

Utilities:

- Rationale: Lower inflation reduces the appeal of defensive utilities, which thrive in high-rate environments.

- Avoid: NextEra EnergyNEE-- (NEE), Dominion EnergyD-- (D).

Risk Considerations and Monitoring

- Housing Costs: Shelter inflation, which lags in CPI reporting, could surprise upward, reversing trends.

- Fed Policy: Even with sub-forecast CPI, the Fed may maintain high rates to combat sticky inflation.

- Global Supply Chains: Disruptions could reignite cost pressures in sectors like industrials.

Conclusion: Time to Rotate

Sub-forecast inflation data creates a tactical opportunity to rotate into sectors poised to benefit from easing cost pressures and reduced rate hike risks. Investors should overweight Aerospace & Defense and Technology while trimming exposure to Building Materials and Utilities. The next critical data points—August CPI and Fed Chair Powell's Jackson Hole speech—will clarify whether this trend persists.

For now, the market's backward-looking data suggests: act on the rotation before the data goes forward.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet