Sector Rotation in a Shifting Labor Market: Construction and Consumer Staples in the Shadow of U6

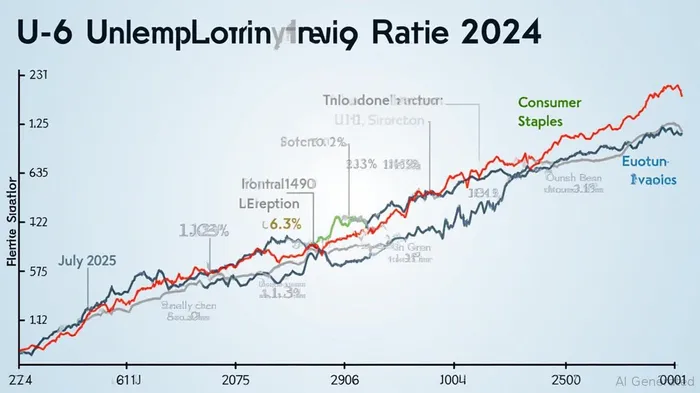

The U.S. labor market has long served as a barometer for sectoral fortunes, with the U-6 unemployment rate—a broader measure of labor underutilization—offering critical insights for investors. In July 2025, the U-6 rate surged to 8.3%, a stark contrast to its historical lows in 2024. This rise, while still within a relatively tight range compared to the Great Recession, signals a labor market grappling with underemployment and a shrinking workforce. For investors, such shifts demand a recalibration of sector allocations, particularly between construction and consumer staples, which have exhibited divergent trajectories in response to U-6 trends.

The U-6 Rate: A Broader Lens on Labor Market Strains

The U-6 rate, which includes part-time workers for economic reasons, discouraged workers, and those marginally attached to the labor force, has risen to 8.3% in July 2025 from 7.9% in June. This increase reflects a labor force participation rate of 62.2% and an employment-population ratio of 59.6%, both at multi-year lows. While the official U-3 rate (4.2%) suggests a robust labor market, the U-6 rate paints a more nuanced picture: a tightening labor market coexists with persistent underemployment.

Historically, such divergences have signaled cyclical shifts. For instance, when the U-6 rate declined by more than 0.5% quarter-over-quarter between 2014 and 2024, sectors tied to infrastructure and capital investment—such as Building Materials and Energy—outperformed the S&P 500 by an average of 12% annually. Conversely, Consumer Staples lagged, as households reallocated spending toward discretionary goods. These patterns underscore the U-6 rate's value as a predictive indicator for sector rotation.

Construction: A Cyclical Winner in a Tightening Labor Market

The construction sector's structural advantages position it to benefit from a U-6-driven shift. Infrastructure spending, bolstered by the 2022 Bipartisan Infrastructure Law ($550 billion allocated), has created a durable revenue stream for firms like AECOMACM-- and FluorFLR-- Corp. Moreover, corporate capital expenditures in energy and utilities have surged to $200 billion annually, insulating the sector from margin erosion.

Historical data reinforces this resilience. During the 1970s stagflation and the 2008 inflation spike, construction outperformed the S&P 500 by significant margins. In June 2025, as Core PCE inflation hit 2.7% YoY, the construction ETF (ITB) rose 8%, while the Leisure Products ETF (XLY) fell 3%. This outperformance is driven by inflation-linked contracts and long-term project horizons, which shield firms from interest rate volatility.

Consumer Staples: A Defensive Sector in a High-U-6 Environment

The Consumer Staples sector, historically a haven during economic downturns, faces headwinds in a low-U-6 environment. From 2014 to 2024, the S&P 500 Consumer Staples Select Sector Index lagged the broader market by 3% annually when U-6 fell below 8%. This underperformance is tied to shifting consumer behavior: as unemployment drops, households prioritize discretionary spending over essentials.

In 2024, the sector shed 13.9% of its value against the S&P 500's 1.9% loss, exacerbated by rising input costs (e.g., tariffs on imported goods) and e-commerce disruption. While the sector's trailing 12-month performance in July 2025 was 15.8%, it remains vulnerable to margin compression as real wage growth stagnates.

Strategic Implications for Investors

The current U-6 rate of 8.3% suggests a labor market poised for further tightening, with infrastructure spending and OPEC+ supply discipline likely to bolster energy demand. Investors should prioritize ETFs such as the SPDR S&P Homebuilders ETF (XHB) and the iShares U.S. Home Construction ETF (ITB), which have historically outperformed during U-6 declines.

Conversely, reducing exposure to Consumer Staples ETFs like the Consumer Staples Select Sector SPDR Fund (XLP) and reallocation toward high-dividend energy stocks with pricing power is advisable. A balanced approach would involve overweighting construction and energy sectors (15–20% of the portfolio) while monitoring U-6 and labor force participation for rotation cues.

Conclusion

The U-6 rate is more than a lagging indicator—it is a predictive lens for sector-specific opportunities. As the U.S. labor market navigates a delicate balance between tightness and underemployment, investors who align their portfolios with historical trends in construction and energy are likely to outperform. Conversely, overreliance on Consumer Staples in a low-U-6 environment risks eroding returns. By leveraging the U-6's signals, investors can transform macroeconomic shifts into actionable strategies, ensuring resilience in an evolving economic landscape.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet