SanDisk Plunges 8% on Citron Short: Has the Memory Cycle Truly Peaked?

On Tuesday, major memory chip manufacturer SanDiskSNDK-- (SNDK) experienced significant market turbulence, with its shares plummeting by as much as 8% intraday before recovering slightly to close down 4.2%. This sudden volatility was entirely triggered by a scathing short report published by activist short-seller Citron Research, which declared the current memory supply shortage a mere "mirage" and claimed the cycle peak is imminent. Given SanDisk's extraordinary 175% year-to-date surge in early 2026 and a staggering 1200% rally over the past 12 months, the intervention abruptly halted the stock's historic momentum.

From a macro-analytical standpoint, my position is clear: while Citron correctly identifies the inherent cyclical risks and historical pricing dynamics in the memory market, their timing appears heavily flawed due to structural shifts in AI-driven data center demand. As historical backtesting of Citron’s previous campaigns against high-growth tech stocks will demonstrate later in this report, short-term volatility induced by these publications frequently gives way to substantial long-term losses for short sellers betting against secular market trends.

The Anatomy of Citron’s Short Thesis

The foundation of Citron's thesis relies on a combination of competitive threats, insider selling signals, and historical cycle patterns. Fundamentally, Citron categorizes SanDisk's core product as a basic commodity rather than a highly defensible technological asset with a moat, drawing a sharp contrast to AI leaders like Nvidia. The primary catalyst for their bearish stance is the strategic maneuvering of Samsung Electronics.

Citron noted that Samsung, the "800-pound gorilla" of the industry with a 30-year history of prioritizing market share over margins, recently stated they will not sell products below a 50% gross margin. More importantly, Samsung is aggressively migrating its most advanced chips into the premium Solid State Drive (SSD) market, directly challenging SanDisk's core customer base with cheaper technology.

Furthermore, Citron highlighted a prominent institutional red flag: Western Digital, a long-term SanDisk stakeholder, recently liquidated a significant portion of its holdings at a 25% discount to current market prices. Citron interprets this aggressive block sale as a definitive signal from insiders that the memory cycle is rapidly approaching a peak. They argue the current tight supply is merely a temporary bottleneck caused by Samsung's yield problems in an unrelated product line, warning that production capacity equivalent to double the 2018 peak is ready to flood the market. According to Citron, this dynamic means the supply-demand balance could completely reverse following a single earnings call.

Market Pushback and the AI Macro Cycle

The market reaction was immediate, breaking SanDisk's relentless upward trajectory. However, institutional and retail pushback suggests the short thesis may lack the necessary broader macroeconomic context. On retail platforms like Stocktwits, while sentiment briefly shifted into the "bearish" zone over the past 24 hours, user engagement remained relatively low, and sophisticated users highlighted critical flaws in Citron's timeline. For instance, user "thealster" pointed out that while Citron's directional logic regarding memory cycles is historically sound, their timing might be "two years early".

The primary counterargument is that Samsung is currently generating substantially more profit by allocating fabrication lines to High Bandwidth Memory (HBM) for Nvidia's AI processors than from its traditional NAND flash business. This sentiment closely aligns with the broader Wall Street consensus observed across major investment banks. Recent commentary from analysts at Goldman Sachs and Morgan Stanley has repeatedly emphasized that the global AI server build-out is creating an extended supply drain on overall memory components, fundamentally altering the traditional boom-and-bust cycle. By aggressively diverting wafer capacity to HBM to feed data center demand, major fabricators structurally limit the risk of an immediate NAND oversupply. Consequently, equating the 2026 memory landscape strictly to the 2018 or 2012 cycle peaks drastically underestimates the persistent demand generated by modern AI infrastructure.

Citron’s Track Record: A History of Mistiming

Evaluating the true weight of this short report requires scrutinizing Citron Research's historical performance, particularly amidst their ongoing credibility challenges. The firm has faced intense legal and regulatory scrutiny, including severe allegations from the U.S. Securities and Exchange Commission (SEC) and the Department of Justice regarding market manipulation and misleading investors through their short-selling reports. Historically, Citron has frequently targeted high-flying tech companies on the basis of "overvaluation," often with disastrous long-term results. According to Ainvest analysis, backtesting three of Citron's most famous short calls reveals a highly consistent pattern.

When Citron shorted Nvidia on June 9, 2017, arguing the stock was priced for perfection, the equity dropped 6.46% on the day of the report and remained down 5.2% over the following week. However, the thesis completely failed long-term; one year later, the stock had gained 62.95%, and the return to date stands at an astronomical 4723.06%.

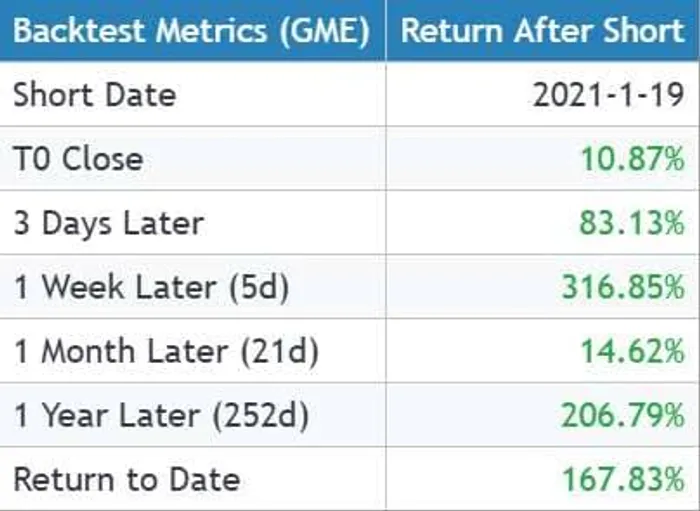

Similarly, their January 19, 2021, short on GameStop resulted in a historic short squeeze. While the stock initially closed up 10.87% on the first day, it surged 316.85% within one week, resulting in catastrophic losses for short sellers.

Even when Citron correctly identified short-term headwinds, such as their November 27, 2020, short on Palantir—which successfully drove the stock down 27.47% over a year—the broader trend eventually overwhelmed them, with the stock ultimately returning 343.51% to date. These metrics clearly demonstrate that while Citron can effectively manufacture a T0 or 3-day panic selloff, betting against secular growth trends based on traditional cyclical metrics has consistently proven to be a flawed strategy over extended time horizons.

Conclusion

In conclusion, Citron Research's aggressive attack on SanDisk presents a localized shock to the equity rather than a fundamental fracture in the memory sector's broader bull case. While the warnings regarding Samsung's immense capacity expansion and Western Digital's discounted block sale warrant careful monitorization by risk managers, the core thesis heavily relies on legacy cyclical patterns that completely fail to account for the AI-driven HBM capacity drain occurring across the semiconductor industry.

Given Citron's heavily documented history of mistiming structural technology trends and their current regulatory burdens, investors should view the recent 4.2% drop as a potential consolidation phase and volatility event rather than the definitive cycle top Citron claims it is. The memory market is undeniably cyclical, but until clear, empirical data emerges showing a collapse in enterprise SSD pricing and a normalization of HBM demand, the macro environment remains highly supportive of SanDisk's core business trajectory.

Tianhao Xu is currently a financial content editor, focusing on fintech and market analysis. Previously, he worked as a full-time forex trader for several years, specializing in global currency trading and risk management. He holds a master’s degree in Financial Analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet