Sanctions Jolt Oil—But Do They Have Legs?

Oil prices are rising once more as investors absorb the Trump administration’s new sanctions on Russia’s two biggest oil producers, Lukoil and Rosneft an action that injects fresh geopolitical tension into an already volatile energy market.

The sanctions, announced October 22, mark a major escalation in Washington’s campaign to pressure Moscow for its “lack of serious commitment” to ending the war in Ukraine. President Donald Trump called the measures “tremendous” in scope, while Treasury Secretary Scott Bessent confirmed that the U.S. “is prepared to take further action if necessary,” signaling that the administration may strengthen restrictions in the weeks ahead.

Oil Funds Rebound On Sanctions Shock

Energy markets responded swiftly. The United States Oil Fund LP (USO) surged 3.4% on Wednesday and another 4% Thursday morning, while the United States Brent Oil Fund LP (BNO) climbed 3.3% and then 3%, extending the early week rebound.

But flows aren’t buying it. Despite the pop, money hasn’t meaningfully chased crude exposure. BNO shows roughly –$18M YTD and –$1.5M over the past month in net flows (as of Oct. 23). USO sits at –$73M YTD. That’s not the posture of investors bracing for a lasting supply shock.

Macro gravity still points down. The sanctions could tighten Brent at the margin if export frictions stick—but the bigger forces remain OPEC+ supply growth and uneven demand (China’s slower industrial pulse still looms). Goldman Sachs this week reiterated a bearish glide path, projecting Brent at ~$52 by late 2026 amid persistent surplus risk. Reuters

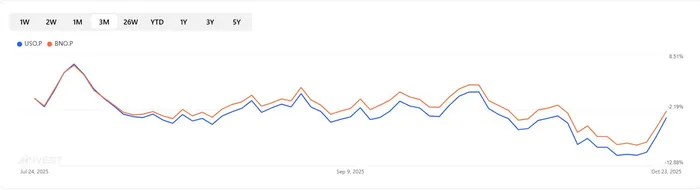

Market watchers say the sanctions rally may be more of a geopolitical reaction than a structural shift in investor sentiment. Both USO and BNOBNO-- remain negative for the year, down roughly 3% and 1%, respectively, amid OPEC+ production increases led by Saudi Arabia and Russia.

Demand Weakness Weighs On Outlook

Even as sanctions tighten supply expectations, global demand concerns continue to restrain prices. President Trump’s renewed tariff threats and ongoing trade tensions have clouded world growth prospects, while China’s slowing economy—still grappling with a real estate downturn and accelerating its transition to cleaner energy—has cut back on crude imports.

The Road Ahead For Oil ETFs

Analysts view the road ahead for oil ETFs as balanced between geopolitically driven price support and supply-side resistance. Should U.S. sanctions meaningfully constrain Russian exports, Brent-linked instruments like BNO may benefit from near-term tailwinds.

Yet any sustained rally will likely be capped by rising OPEC+ output and weak demand from China. Without clear evidence of renewed global consumption growth, oil may struggle to build on its recent bounce.

For now, fund flows tell the story: investors remain reluctant to commit fresh capital, wary that the latest surge is fueled more by politics than fundamentals. Unless stronger demand signals emerge from major economies, oil ETF performance is likely to remain uneven—driven less by data and more by headlines out of Washington and Moscow.

Quickly compare USO, BNO with our ETF Compare Tool

Market Radar delivers concise, daily trading ideas by tracking everything from options activity and market sentiment to high-profile political trades.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet