Salesforce Slides as Weak Guidance Overshadows Solid Q2 Beat and AI Momentum

Salesforce delivered a mixed second-quarter report that beat expectations on both revenue and earnings but fell short on guidance, sending its shares down about 7% in pre-market trading. The company posted adjusted earnings of $2.91 per share, ahead of analyst expectations of $2.78, on revenue of $10.2 billion, which topped consensus of $10.14 billion. Net income climbed to $1.89 billion from $1.43 billion a year ago. Yet despite the beat, management’s outlook for the October quarter disappointed investors, particularly on revenue growth and backlog metrics, while the updated full-year guidance suggested a more tempered pace. Salesforce’s decision to expand its share repurchase authorization by another $20 billion underscored its commitment to shareholder returns, but the cautious revenue outlook overshadowed the positives, especially given the stock’s struggles this year.

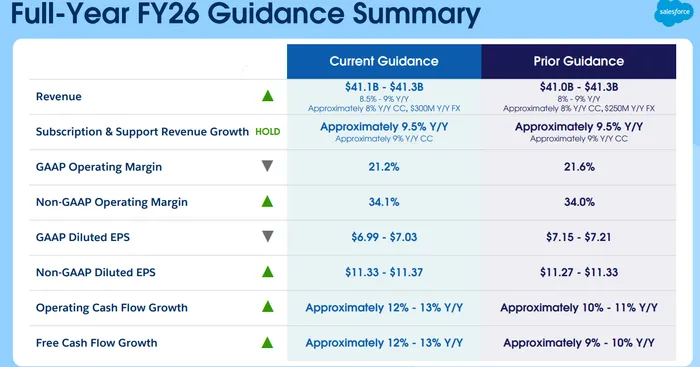

Breaking down the results, Salesforce’s 10% revenue growth was steady, fueled by strong performance in its core clouds and momentum in Data Cloud and AI, where annual recurring revenue climbed 120% year-over-year to $1.2 billion. Notably, the company closed 60 deals worth more than $1 million that included both Data Cloud and AI products, signaling traction in its efforts to monetize artificial intelligence. Current remaining performance obligations (CRPO), a closely watched backlog metric, grew 11% to $29.4 billion, slightly above estimates, offering some reassurance on future demand. Operating margins were also a bright spot, with adjusted operating margin at 34.3%, up 60 basis points, while GAAP margin rose to 22.8%, reflecting ongoing efficiency initiatives. However, while management lifted the low end of its full-year revenue outlook to $41.1 billion, the top end held steady at $41.3 billion, representing growth of about 8%—below the 8.7% the Street had hoped for. This cautious guidance sent a clear signal that near-term top-line acceleration remains elusive.

For investors, the concerns are clear. SalesforceCRM-- has struggled to regain the growth spark that once made it a high-flying SaaS name, with revenue stuck in the single-digit range since mid-2024. Analysts and investors remain unconvinced that its AI initiatives, particularly Agentforce, will generate the kind of explosive growth seen in peers like Microsoft or Nvidia. CFO Robin Washington acknowledged ongoing challenges in marketing and commerce products, as well as slower growth in some geographies, which could weigh on future performance. CEO Marc Benioff struck a confident tone on the call, arguing that demand for AI-driven SaaS is strong, but Wall Street’s skepticism is evident in the stock’s performance.

From a technical perspective, Salesforce’s stock has taken a turn for the worse. Heading into earnings, the stock was testing resistance at its 50-day moving average, but the post-earnings drop has pushed it decisively below both the 50- and 20-day moving averages. This breakdown raises the risk of further downside, with the August low near $226 now in focus as a critical support level. Compounding the technical weakness is the stock’s Accumulation/Distribution, suggesting institutions have been net sellers over the past 13 weeks. That pattern hints that large investors may be pulling back, reducing confidence in the sustainability of any near-term bounce. A test of $226 could serve as a litmus for whether institutional buyers step back in or whether the selling pressure deepens.

Yet despite these concerns, valuation could provide a backstop. Analysts note that Salesforce’s enterprise value to free cash flow multiple has fallen to a decade low, reflecting investor worries about disruption from AI-native competitors. This cheaper profile could make the stock attractive to long-term buyers willing to look past near-term sluggishness, especially with free cash flow guidance raised for the year and $25 billion still available under the expanded buyback program. In addition, the stock’s heavy underperformance versus large-cap tech peers leaves room for mean reversion if sentiment improves, particularly around AI adoption or the October Dreamforce conference, where management is expected to showcase new product capabilities.

In summary, Salesforce’s Q2 results were better than feared on paper, with solid beats on revenue, EPS, and backlog metrics, but the guidance reinforced the narrative of slowing growth and left investors disappointed. Technical breakdowns and evidence of institutional distribution suggest pressure may continue in the near term, with $226 a key level to watch. Longer term, however, the combination of improving margins, AI momentum, and an unusually cheap valuation could rekindle institutional interest, particularly if Dreamforce delivers positive surprises. For now, Salesforce remains caught between cautious near-term fundamentals and the possibility of longer-term re-rating if its AI initiatives start to meaningfully contribute to growth. The path forward may be choppy, but traders and investors alike will be watching whether CRMCRM-- stabilizes at support or whether this latest disappointment signals further pain ahead.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet