Salesforce's Cost Cuts Boost Margins: Will Expansion Continue Further?

Salesforce, Inc. CRM has delivered strong margin expansion over the past year, driven by disciplined cost controls and a shift toward profitable growth. The company’s operating efficiency has improved steadily, as reflected by margin expansion in each of the trailing four quarters.

In the first, second, third and fourth quarters of fiscal 2026, Salesforce’s non-GAAP operating margin expanded 20 basis points (bps), 60 bps, 240 bps and 110 bps, respectively, on a year-over-year basis. In fiscal 2026, the company’s overall non-GAAP operating margin improved 110 bps year over year to 34.1%.

Salesforce’s disciplined cost management through workforce optimization and reduction in discretionary spending has supported margin expansion. Consistent progress in the operating margin highlights Salesforce’s ability to scale profitability even as revenue growth remained moderate. The company’s revenue growth rate has slowed down from a double-digit percentage range to a single-digit percentage over the past two fiscal years. This scenario indicates that Salesforce’s cost discipline has clearly boosted margins.

Salesforce's operating margin expansion over the past year has also been driven by the rapid adoption of its artificial intelligence (AI)-powered "Agentforce" and Data Cloud products, which significantly increased high-margin recurring revenues. Agentforce and Data Cloud combined brought in $2.9 billion in recurring revenues in the fourth quarter of fiscal 2026, representing a 200% year-over-year increase. Agentforce alone generated $800 million in recurring revenues, reflecting a 169% year-over-year surge.

Nonetheless, sustaining margin expansion may be harder going forward. SalesforceCRM-- is increasing investments in AI and is focusing on funding the growth of Agentforce and Data Cloud, which could pressure costs in the near term. The company is prioritizing market share in AI over immediate maximum profitability, reinvesting savings from operational efficiencies into research and development to accelerate its AI roadmap. Management’s non-GAAP operating margin of 34.3% for fiscal 2027 indicates a modest 20 bps expansion from fiscal 2026.

How Competitors Fare Against Salesforce

Microsoft Corporation MSFT and Oracle Corporation ORCL are two main rivals of Salesforce in the enterprise software market.

Microsoft is witnessing strong revenue and earnings growth, driven by robust demand for cloud and AI offerings. Microsoft Cloud revenues increased 26% year over year to $51.5 billion in the second quarter of fiscal 2026. Microsoft Cloud business stands out with a strong gross margin of 67% in the second quarter.

Oracle’s revenues have been growing robustly in recent quarters, driven by growing AI workload demands, multi-cloud partnerships and the adoption of its specialized database services. However, the company continues to invest heavily in cloud infrastructure and AI capabilities, which is hurting its profitability. In the third quarter of fiscal 2026, Oracle’s non-GAAP operating margin contracted 100 bps to 43%.

Salesforce’s Price Performance, Valuation and Estimates

Shares of Salesforce have plunged 34.5% over the past year compared with the Zacks Internet – Software industry’s decline of 10.4%.

Salesforce One-Year Price Return Performance

Image Source: Zacks Investment Research

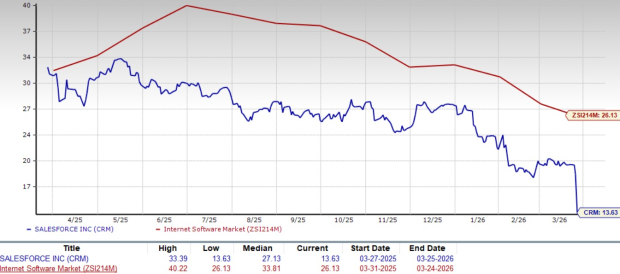

From a valuation standpoint, CRMCRM-- trades at a forward price-to-earnings ratio of 13.63, significantly below the industry’s average of 26.13.

Salesforce Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Salesforce’s fiscal 2026 and 2027 earnings implies a year-over-year increase of approximately 4.8% and 11.9%, respectively. Estimates for fiscal 2026 and 2027 have been revised upward in the past 30 days.

Image Source: Zacks Investment Research

Salesforce currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Salesforce, Inc. (CRM): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet