Will Ross Stores' Store Expansions and Other Initiatives Aid?

Ross Stores, Inc. ROST has been making smart moves to enrich shoppers’ experience and bolster growth. The company’s strategic initiatives, including its ongoing store openings and expansions, have boosted comparable store sales (comps) by attracting more customers and increasing average spending. It continues to gain from positive customer response for its merchandise across banners.

In fourth-quarter fiscal 2025, comps improved 9%. Categories such as shoes and cosmetics were among the strongest performers, while the Ladies business continued to show strong momentum following merchandising and vendor assortment improvements. Management also noted that every region delivered positive comparable sales growth, with the Midwest and Mountain regions leading performance. Such positives led to a sales increase of 12% year over year, with earnings per share (EPS) rising 21% in the reported quarter. For fiscal 2026, ROSTROST-- expects comps growth of 3-4%, with total sales anticipated to increase 5-7%.

The company continues its disciplined expansion strategy. Its store-expansion efforts are focused on continually increasing penetration in the existing as well as new markets. In fiscal 2025, ROST’s store expansion program marked another year of disciplined growth as it entered new markets and strengthened its presence in the existing ones. In fiscal 2025, the company opened 80 Ross Dress for Less stores and 10 dd’s DISCOUNTS locations.

Building on this momentum, the company expects to expand its store base by 5% in fiscal 2026. The company plans to open 110 locations in fiscal 2026, including 85 Ross storesROST-- and 25 dd’s DISCOUNTS. This expansion reflects a reacceleration of dd’s DISCOUNTS. In the long term, it has the potential to expand the Ross chain to 2,900 locations and dd’s DISCOUNTS to 700 stores, further broadening its reach over time.

Additionally, Ross Stores’ marketing efforts emphasize its off-price model and consistent value through digital channels, traditional advertising and store expansion to reinforce its position as a leading off-price retailer. The company aims to attract and retain a diverse customer base seeking high-quality merchandise at affordable prices. In a nutshell, Ross Stores appears well-poised for long-term growth, supported by steady store openings, solid execution and financial resilience.

ROST’s Price Performance, Valuation and Estimates

Shares of Ross Stores have gained 44.2% in the past six months compared with the industry’s growth of 11.8%.

Image Source: Zacks Investment Research

From a valuation standpoint, ROST trades at a forward price-to-earnings ratio of 28.34X compared with the industry’s average of 32.64X.

Image Source: Zacks Investment Research

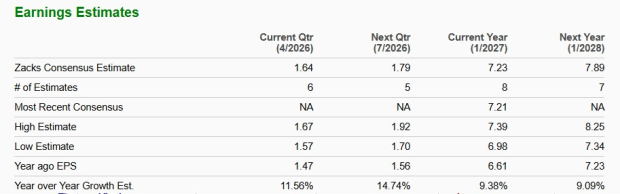

The Zacks Consensus Estimate for ROST’s current-year and next-year earnings per share (EPS) implies year-over-year growth of 9.4% and 9.1%, respectively. The estimates for the aforesaid years have moved north in the past 30 days.

Image Source: Zacks Investment Research

Ross Stores stock currently carries a Zacks Rank #2 (Buy).

More Key Retail Stock Picks

Deckers Outdoors Corporation DECK, together with its subsidiaries, designs, markets, and distributes footwear, apparel and accessories for casual lifestyle use and high-performance activities in the United States and internationally. At present, Deckers sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for DECK’s current fiscal-year sales and earnings indicates growth of 8.9% and 8.5%, respectively, from the year-ago figures. DECK delivered a trailing four-quarter earnings surprise of 36.9%, on average.

American Eagle Outfitters, Inc. AEO operates as a specialty retailer of casual apparel, accessories and footwear for men and women. At present, AEO sports a Zacks Rank of 1.

The Zacks Consensus Estimate for AEO’s current fiscal-year sales and earnings indicates growth of 4.11% and 16%, respectively, from the year-ago figures. American Eagle delivered a trailing four-quarter earnings surprise of 37.6%, on average.

Five Below, Inc. FIVE operates as a specialty value retailer in the United States. At present, FIVE sports a Zacks Rank of 1.

The consensus estimate for FIVE’s current fiscal-year sales and earnings implies growth of 22.1% and 25%, respectively, from the year-ago figures. FIVE has delivered a trailing four-quarter earnings surprise of 62.1 %, on average.

Free Report: Profiting from the 2nd Wave of AI Explosion

The next phase of the AI explosion is poised to create significant wealth for investors, especially those who get in early. It will add literally trillion of dollars to the economy and revolutionize nearly every part of our lives.

Investors who bought shares like Nvidia at the right time have had a shot at huge gains.

But the rocket ride in the "first wave" of AI stocks may soon come to an end. The sharp upward trajectory of these stocks will begin to level off, leaving exponential growth to a new wave of cutting-edge companies.

Zacks' AI Boom 2.0: The Second Wave report reveals 4 under-the-radar companies that may soon be shining stars of AI’s next leap forward.

Access AI Boom 2.0 now, absolutely free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

American Eagle Outfitters, Inc. (AEO): Free Stock Analysis Report

Deckers Outdoor Corporation (DECK): Free Stock Analysis Report

Ross Stores, Inc. (ROST): Free Stock Analysis Report

Five Below, Inc. (FIVE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet