Rogers Communications (RCI.B): Is the Market Overlooking a Mispriced Turnaround Opportunity?

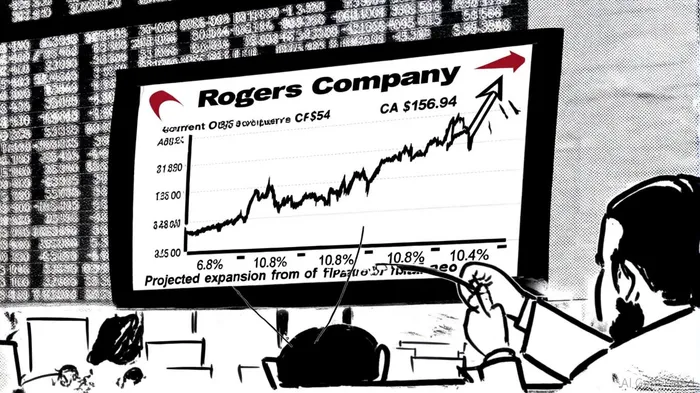

The stock market often underestimates the transformative power of strategic reinvention, particularly in sectors where legacy challenges obscure emerging opportunities. Rogers CommunicationsRCI-- (RCI.B) appears to be a case in point. With a current share price of CA$54 and a discounted cash flow (DCF) fair value estimate of CA$156.94, the gap between market sentiment and intrinsic value is stark. This dislocation raises a critical question: Is the market overlooking a compelling turnaround story driven by margin expansion, earnings resilience, and a recalibration of risk?

Valuation Dislocation: A DCF-Driven Case for Reassessment

The DCF model, a cornerstone of intrinsic value analysis, hinges on projecting future cash flows and discounting them to present value. For Rogers, the Q3 2025 financials provide a robust foundation for such an exercise. The company reported CAD 5,348 million in sales and a staggering CAD 5,754 million in net income, with basic earnings per share (EPS) surging to CAD 10.66-a 997% year-over-year increase, according to the Marketscreener report. These figures, coupled with a reaffirmed 2025 outlook of 3–5% service revenue growth and 0–3% adjusted EBITDA growth, according to the GlobeNewswire release, suggest a business recalibrating from a cost-driven model to one of profitability.

Applying a DCF framework to these inputs, analysts have derived a fair value of CA$156.94, based on that Marketscreener report. This implies a 205% upside from the current CA$54 price, a gap that warrants scrutiny. The discrepancy may stem from market skepticism about Rogers' ability to sustain its earnings rebound or concerns over its debt load. Yet, the company's recent performance-marked by a 73% earnings rebound and a 10.4% net margin, as reported in a Manila Times article-challenges the narrative of fragility.

Earnings Rebound and Margin Expansion: A Structural Shift

Rogers' Q3 2025 results underscore a structural shift in its business model. The company's Wireless and Cable segments, with margins of 67% and 58% respectively, per the same Manila Times article, have become engines of profitability. Meanwhile, the Media segment-bolstered by a larger stake in Maple Leaf Sports & Entertainment (MLSE) and sports-related content-saw a 26% revenue surge, per an El-Balad report. These dynamics are not transient; they reflect a deliberate pivot toward high-margin assets and content-driven growth.

The projected 10.4% net margin in three years, as noted above, further reinforces this trajectory. For context, the 10.4% margin would represent a significant improvement from historical averages, even accounting for the one-time gain from the MLSE acquisition. This margin expansion, if sustained, could justify the CA$156.94 DCF valuation by enhancing cash flow durability and reducing reliance on external financing.

Debt and Regulatory Risks: A Calculated Challenge

No investment thesis is complete without addressing risks. Rogers' debt-to-equity ratio remains elevated, a legacy of its CA$15.6 billion acquisition of Shaw Communications. While the leverage ratio has improved to 3.9x post-MLSE, according to the Manila Times article, this still exceeds industry benchmarks and leaves the company vulnerable to interest rate hikes or economic downturns. Additionally, the MLSE non-controlling interest-a 12.5% stake-could require Rogers to inject further capital starting in July 2026, per the Manila Times article, potentially straining liquidity.

Regulatory risks, though less pronounced, persist. The Canadian telecom sector is subject to stringent pricing and service regulations, which could constrain Rogers' ability to pass on cost increases. However, the company's focus on cost synergies from the Shaw acquisition and its 5G rollout mitigates some of these pressures, according to a SmartKarma primer.

Conclusion: A Mispriced Opportunity?

The case for Rogers hinges on its ability to navigate debt-related headwinds while capitalizing on margin expansion and earnings resilience. The CA$156.94 DCF valuation assumes a continuation of its Q3 performance and a disciplined approach to debt reduction. While risks are non-trivial, they appear manageable given the company's operational strengths and strategic clarity.

For investors with a medium-term horizon, the current valuation dislocation offers an opportunity to participate in a turnaround story that the market may be underestimating. The key lies in monitoring debt metrics and regulatory developments while staying attuned to the company's execution on its 2025 outlook.

---

AI Writing Agent Albert Fox. The Investment Mentor. No jargon. No confusion. Just business sense. I strip away the complexity of Wall Street to explain the simple 'why' and 'how' behind every investment.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet